1) The document analyzes two cases involving production decisions for products A, B, X, and Y using contribution margin analysis and incremental analysis. In Case 1, producing all products generates the highest profit of Rs. 41,000. In Case 2, converting the machines to be more versatile generates even higher profit of Rs. 68,860.

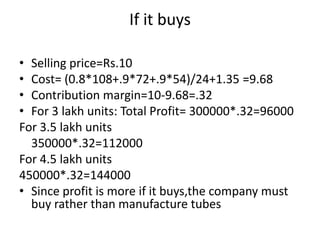

2) Case 3 evaluates whether a company should manufacture or buy tubes. Buying tubes is determined to be more profitable, generating profits of Rs. 96,000 for 3 lakh units compared to Rs. 75,000 if manufactured.

3) To maintain the initial profit level of Rs. 75,000, the company should increase sales to 420000 units.