Downloaded 43 times

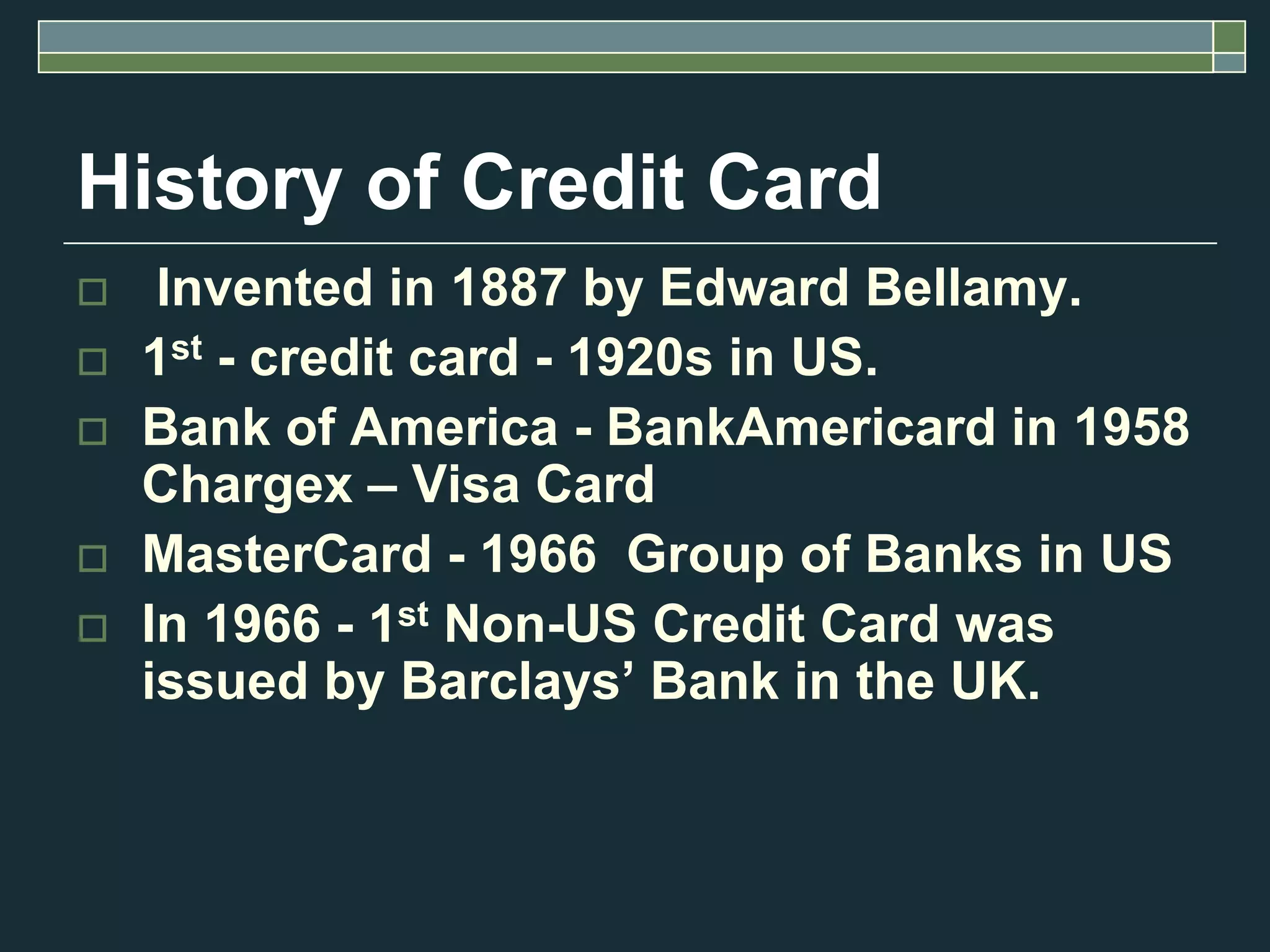

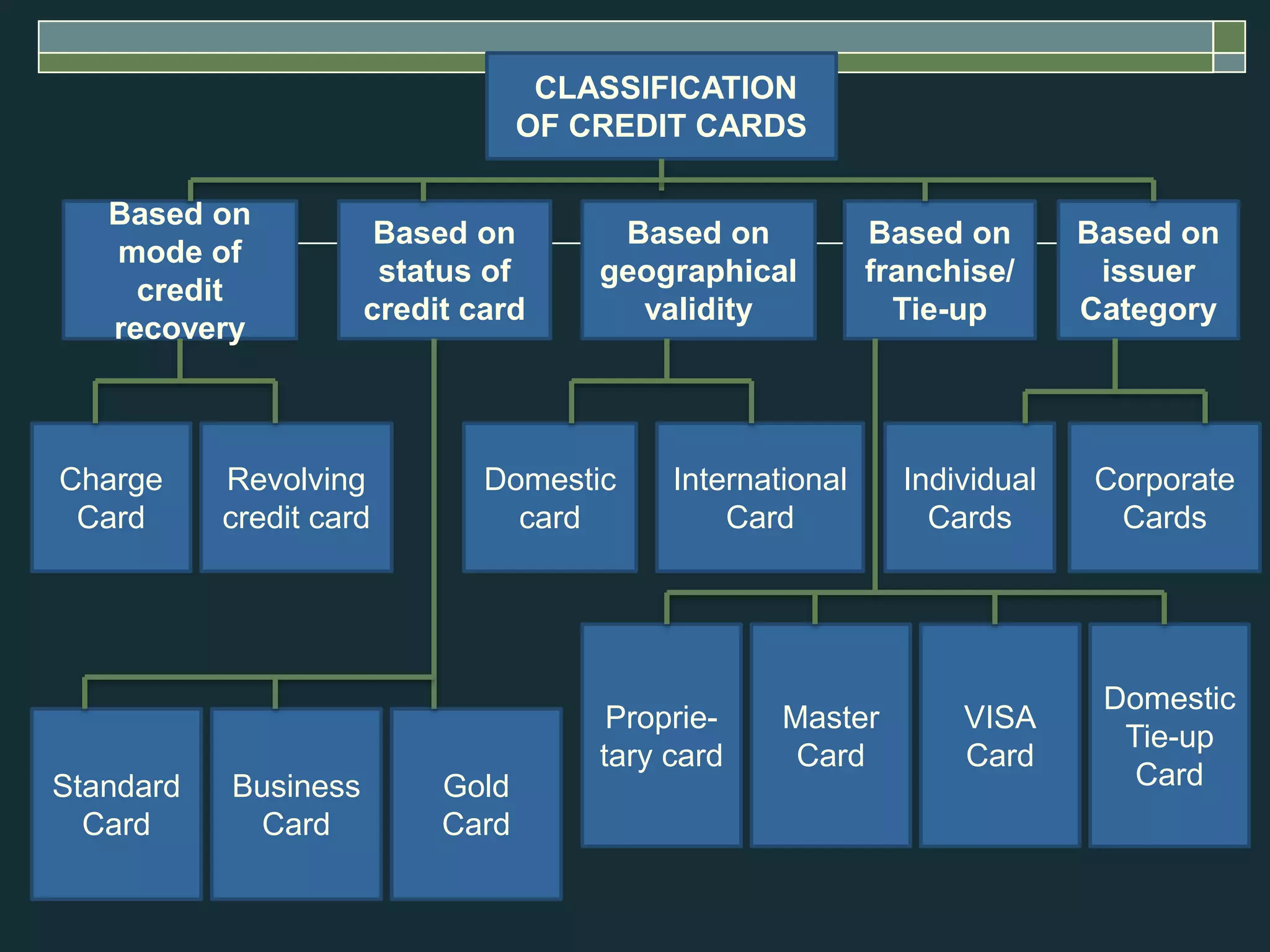

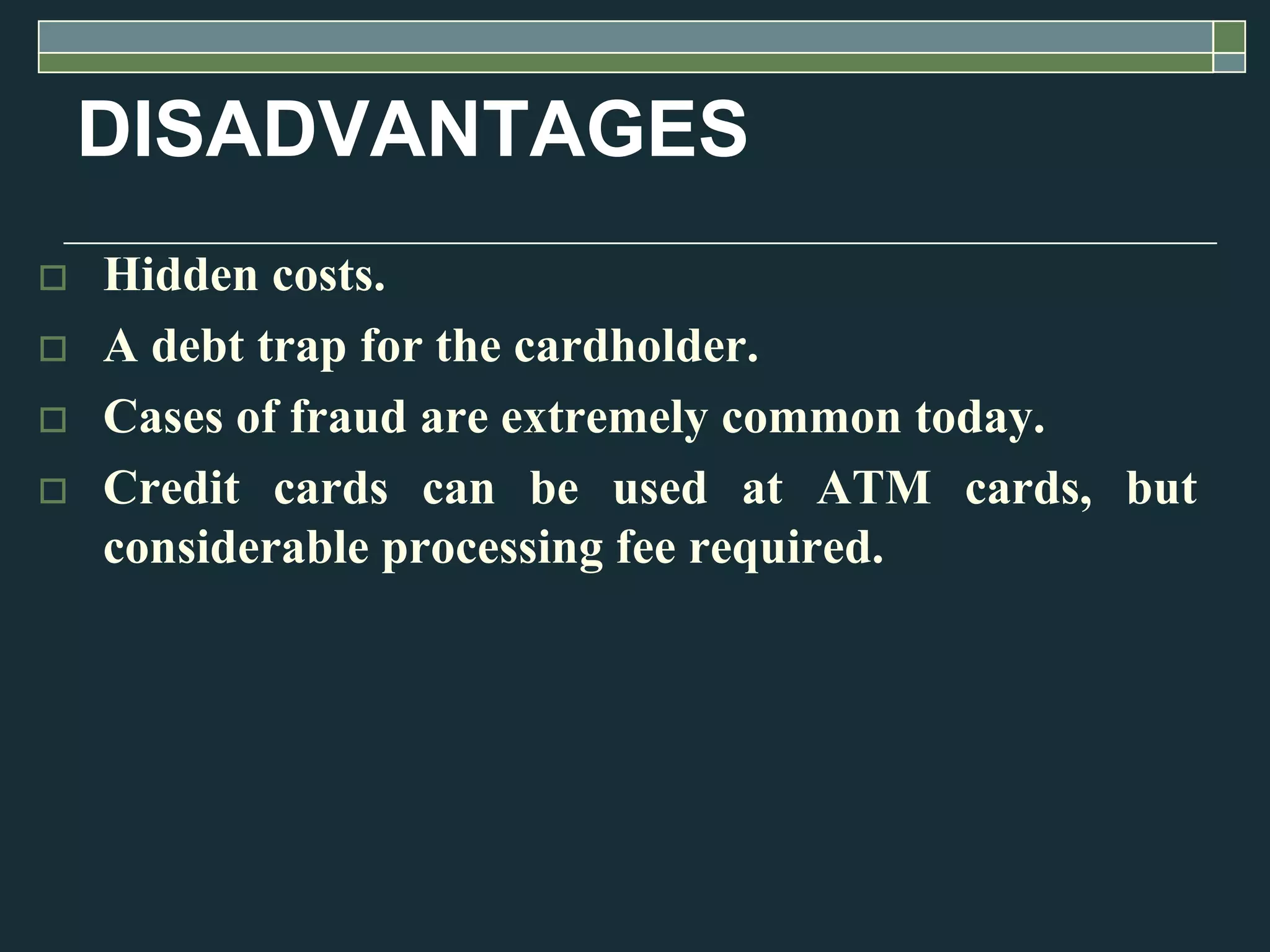

This document discusses credit cards and their history and features. It defines credit cards as plastic cards that can be used to make purchases or obtain cash using a line of credit. Credit cards are classified in different ways, including by mode of credit recovery (charge cards or revolving credit), status (standard, business, gold), geographical validity (domestic, international), franchise/tie-up (proprietary, MasterCard, Visa), and issuer (individual, corporate). The document also outlines the credit card cycle and provides advantages to both cardholders and credit card companies/banks, as well as some disadvantages.