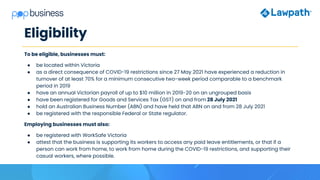

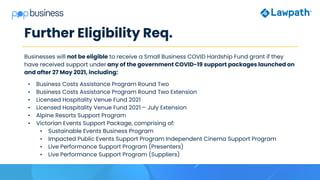

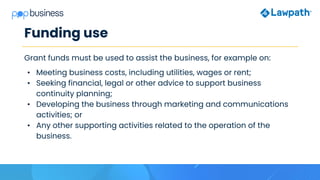

The Victorian Business Support Package, announced in August 2021, allocates an additional $400 million to assist businesses affected by COVID-19, including grants for small businesses with significant revenue declines and funds for hospitality venues. Key offerings include the $180 million Small Business COVID Hardship Fund, the Business Continuity Fund providing $5,000 grants, and specific funding for commercial tenants. Eligibility criteria vary across programs, and applications must be submitted online by specified deadlines.