Downloaded 55 times

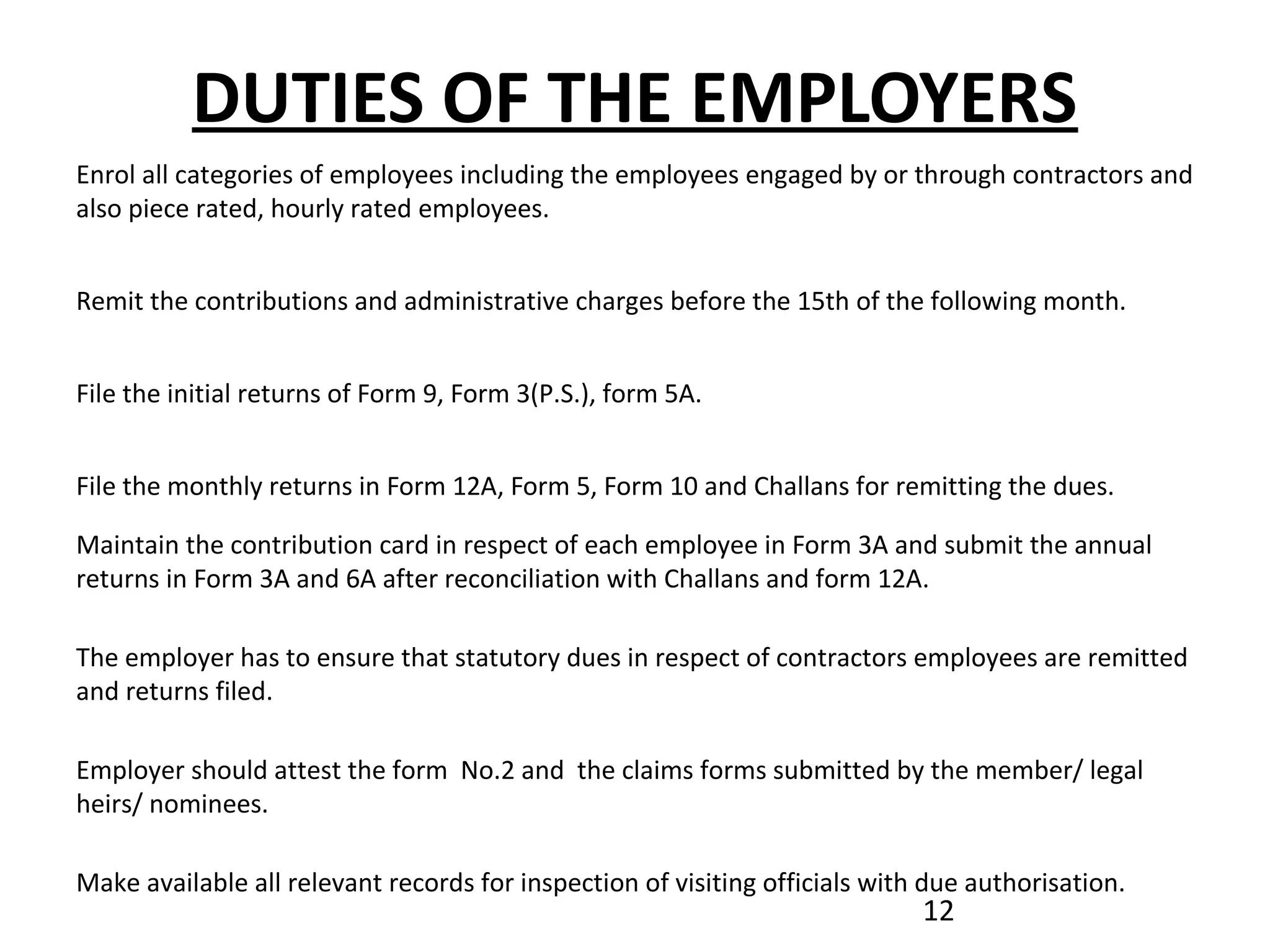

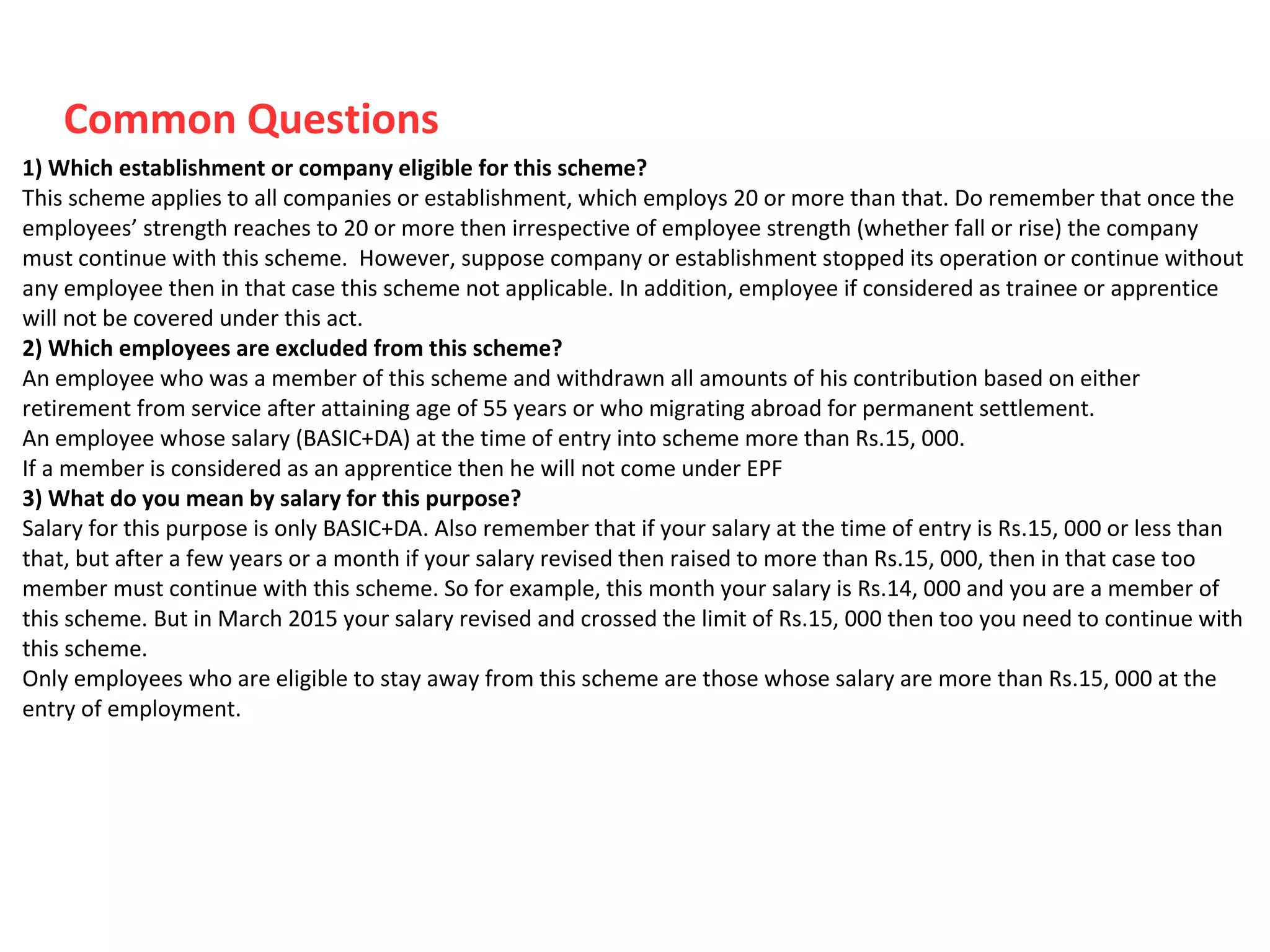

The Employees' Provident Funds & Miscellaneous Provisions Act, 1952 established a social security system for employees in India. It operates three schemes - Provident Fund, Pension Fund, and Insurance Fund. The key provisions include mandatory contributions of 12% of wages by employer and employee for provident fund. The Central Provident Fund Commissioner can assess dues, impose interest for delayed payments, recover dues, and penalize defaulters. Exemptions are provided for small establishments and those under state/central government control. Employers must enroll all eligible employees and make contributions, maintain records, and file regular returns.