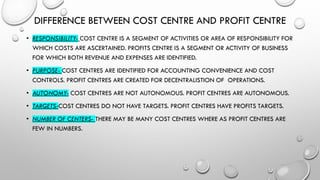

This document provides definitions and explanations of key concepts in cost accounting. It defines cost, costing, cost accounting, and cost accountancy according to the Chartered Institute of Management Accountants. It also defines and explains concepts like cost centers, cost units, profit centers, cost control, cost reduction techniques, and the differences between cost and profit centers. The document was prepared by Dr. R. Sridevi and provides an introduction to foundational cost accounting terminology and principles.