Downloaded 113 times

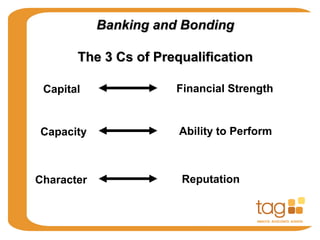

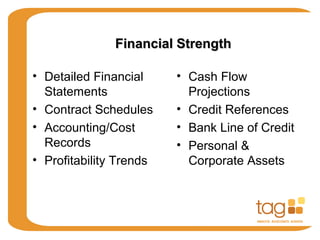

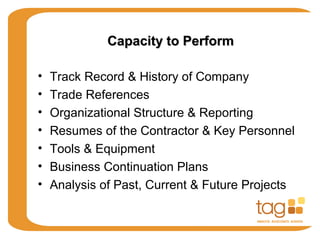

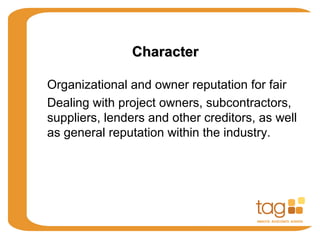

The document outlines the features, roles, and responsibilities of construction financial management, emphasizing the importance of having effective accounting processes and software to support construction businesses. It details key financial statements, job costing principles, cash management practices, and the significance of proper billing and accounts payable processing. Furthermore, it discusses the prequalification criteria for banking and bonding, alongside considerations for choosing appropriate construction accounting software.

![CV-RSS[2]](https://cdn.slidesharecdn.com/ss_thumbnails/e04c1b10-e225-40e5-aba3-491274eb0339-150828133826-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)