The objective ofgeneral purpose financial reporting forms the foundation of the Conceptual

Framework.

OB1 Introduction

The objective of general purpose financial reporting.

Decisions by existing and potential investors.

Considerations for investors’, lenders’, and other creditors’ expectations.

Need for information about the resources of the entity.

Necessity for general purpose financial reports and limitations.

OB2–OB11 Objective, Usefulness, and Limitations of General Purpose Financial Reporting

OB12 Economic Resources and Claims

OB13–OB14 Different types of economic resources

OB15–OB21 Distinguishing between changes in economic resources and claims

Financial Performance Reflected by Accrual Accounting

Financial Performance Reflected by Past Cash Flows

Changes in Economic Resources and Claims Not Resulting from Financial Performance

OB12–OB21 Information about a Reporting Entity’s Economic Resources, Claims, and Changes in Resources and Claims

OB1–OB21 The Objective of General Purpose Financial Reporting

5.

Considerations specific tonot- for- profit entities.

OB22 Objective for Not-for-Profit Entities

Receipts of significant amounts of resources.

Operating purposes.

Absence of defined ownership interests.

Major characteristics of not- for- profit entities.

Information for resource providers about a not- for- profit entity’s service

efforts in accomplishing its mission.

Relevance and faithfulness in providing information to resource providers.

OB23–OB28 Characteristics distinguishing not-for-profit entities from

business enterprises

OB22–OB28 Application of the Objective of General Purpose Financial Reporting to Not-for-Profit Entities

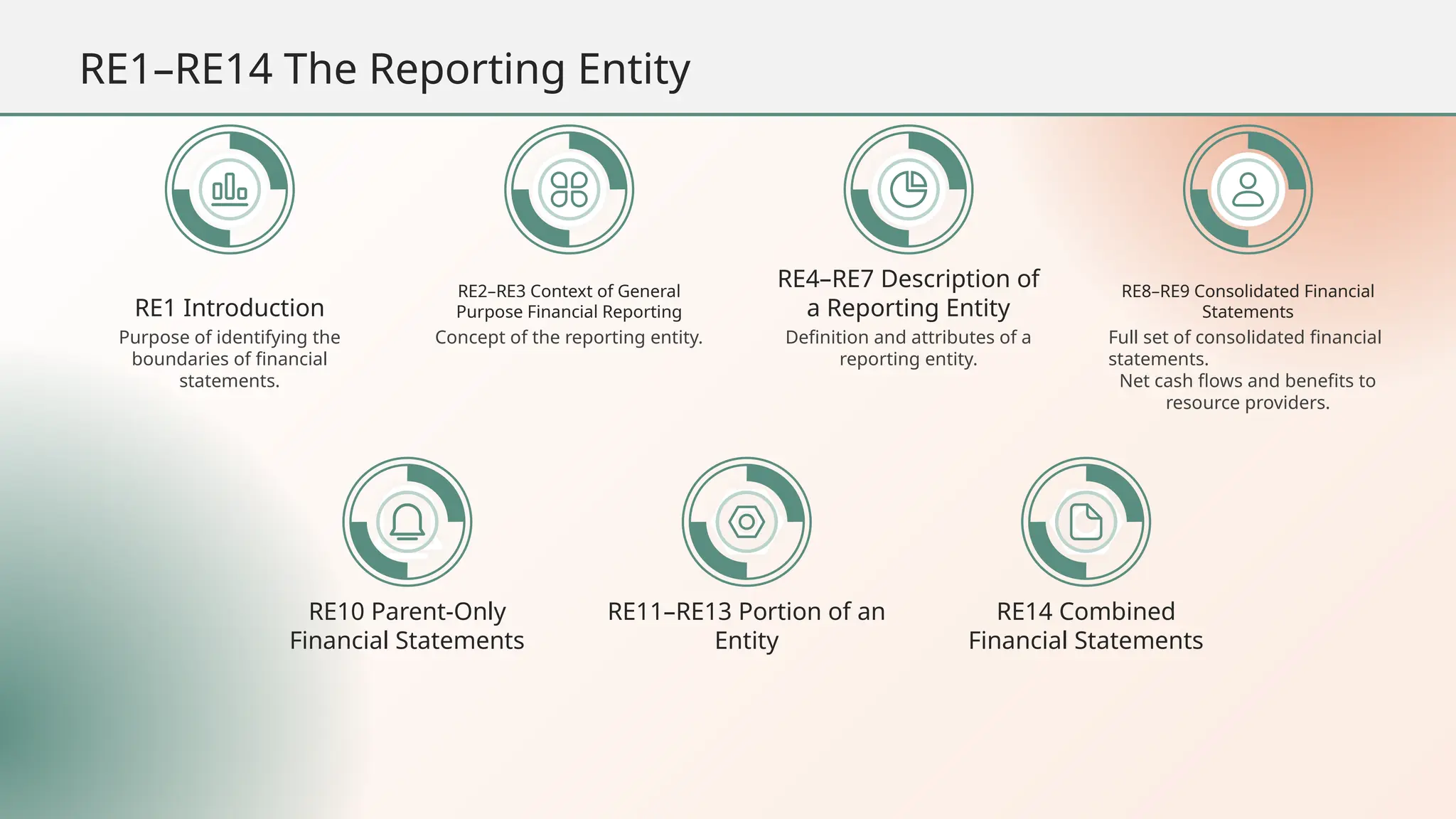

RE1 Introduction

Purpose ofidentifying the

boundaries of financial

statements.

RE2–RE3 Context of General

Purpose Financial Reporting

Concept of the reporting entity.

RE4–RE7 Description of

a Reporting Entity

Definition and attributes of a

reporting entity.

RE8–RE9 Consolidated Financial

Statements

Full set of consolidated financial

statements.

Net cash flows and benefits to

resource providers.

RE10 Parent-Only

Financial Statements

RE11–RE13 Portion of an

Entity

RE14 Combined

Financial Statements

RE1–RE14 The Reporting Entity

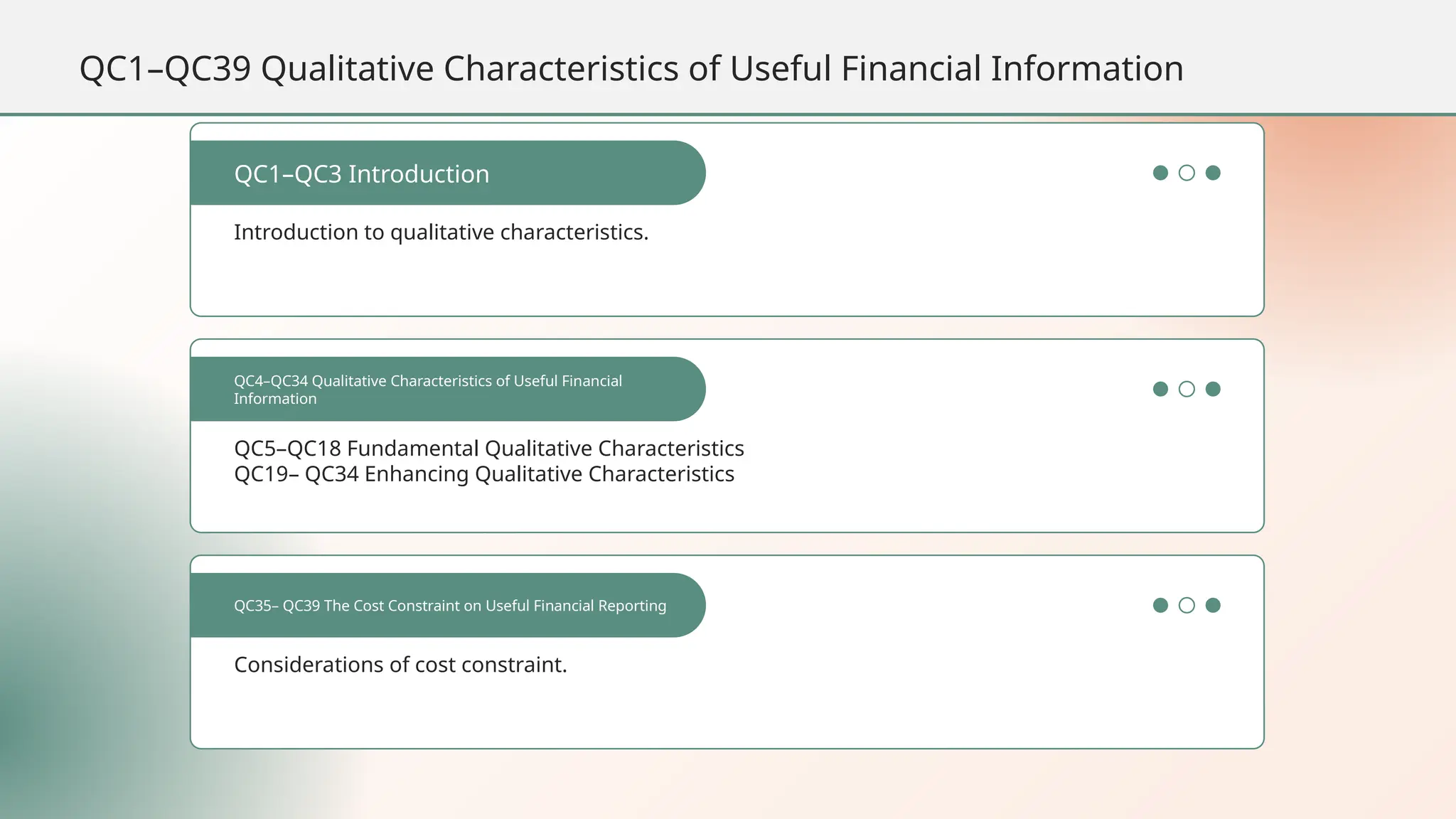

Introduction to qualitativecharacteristics.

QC1–QC3 Introduction

QC5–QC18 Fundamental Qualitative Characteristics

QC19– QC34 Enhancing Qualitative Characteristics

QC4–QC34 Qualitative Characteristics of Useful Financial

Information

Considerations of cost constraint.

QC35– QC39 The Cost Constraint on Useful Financial Reporting

QC1–QC39 Qualitative Characteristics of Useful Financial Information

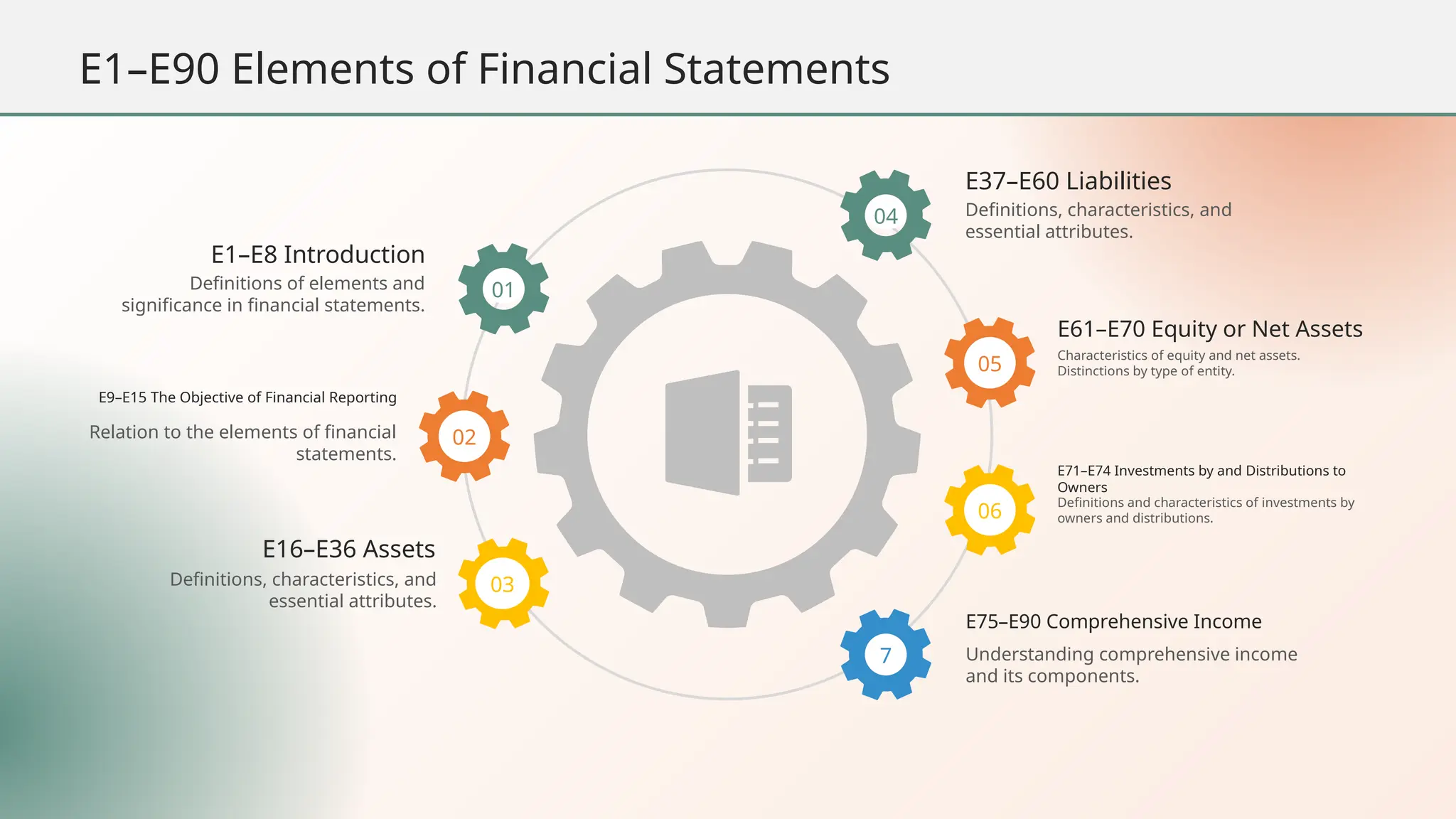

04 Definitions, characteristics,and

essential attributes.

Definitions of elements and

significance in financial statements.

01

E1–E8 Introduction

E37–E60 Liabilities

05

02

Characteristics of equity and net assets.

Distinctions by type of entity.

Relation to the elements of financial

statements.

E9–E15 The Objective of Financial Reporting

E61–E70 Equity or Net Assets

06

Definitions and characteristics of investments by

owners and distributions.

03

Definitions, characteristics, and

essential attributes.

E71–E74 Investments by and Distributions to

Owners

7 Understanding comprehensive income

and its components.

E75–E90 Comprehensive Income

E16–E36 Assets

E1–E90 Elements of Financial Statements

Requirements and relevance.

M15–M20Exit Price System

M1–M3 Introduction

M21–M23 Cash Flows as an Estimate of Exit Prices

Process and relevance in financial reporting.

M4–M6 Measurement

M24–M29 Specific Measurement Circumstances

Definition and applications of entry and exit price

systems.

M7–M9 Measurement Systems

Considerations and factors for choosing relevant

measurement systems.

M30–M42 Choosing between the Relevant Measurement

Systems

Requirements and relevance.

M10–M14 Entry Price System

M1–M49 Measurement

PR4–PR13 The Objectiveof Financial

Reporting

How presentation furthers

the objective.

PR1–PR3 Introduction

Purpose and scope of

presentation in financial

reporting.

PR14–PR34 Information Provided by

Financial Statements

PR20–PR22 Definition of Full Set of Financial

Statements

PR23–PR24 Assets, Liabilities, and Equity

PR25–PR26 Revenues, Expenses, Gains, and

Losses—Components of Comprehensive

Income

PR27–PR28 Cash Flows

PR29–PR30 Investments by and Distributions

to Owners

PR31–PR32 Comprehensive Income and Net

Income (Earnings)

PR33–PR34 Netting of Line Items

PR35–PR54 Line Items, Subtotals,

and Summary Information

Factors for determining line items and

summaries.

PR42–PR49 Cause, Activity, and Frequency

PR50 Expected Time until Realization or

Settlement

PR51 Expected Form of Realization or

Settlement

PR52 Response to Changes in Economic

Conditions and Other Factors

PR53 Measurement

PR54 Relationships with Other Information

PR1–PR54 Presentation

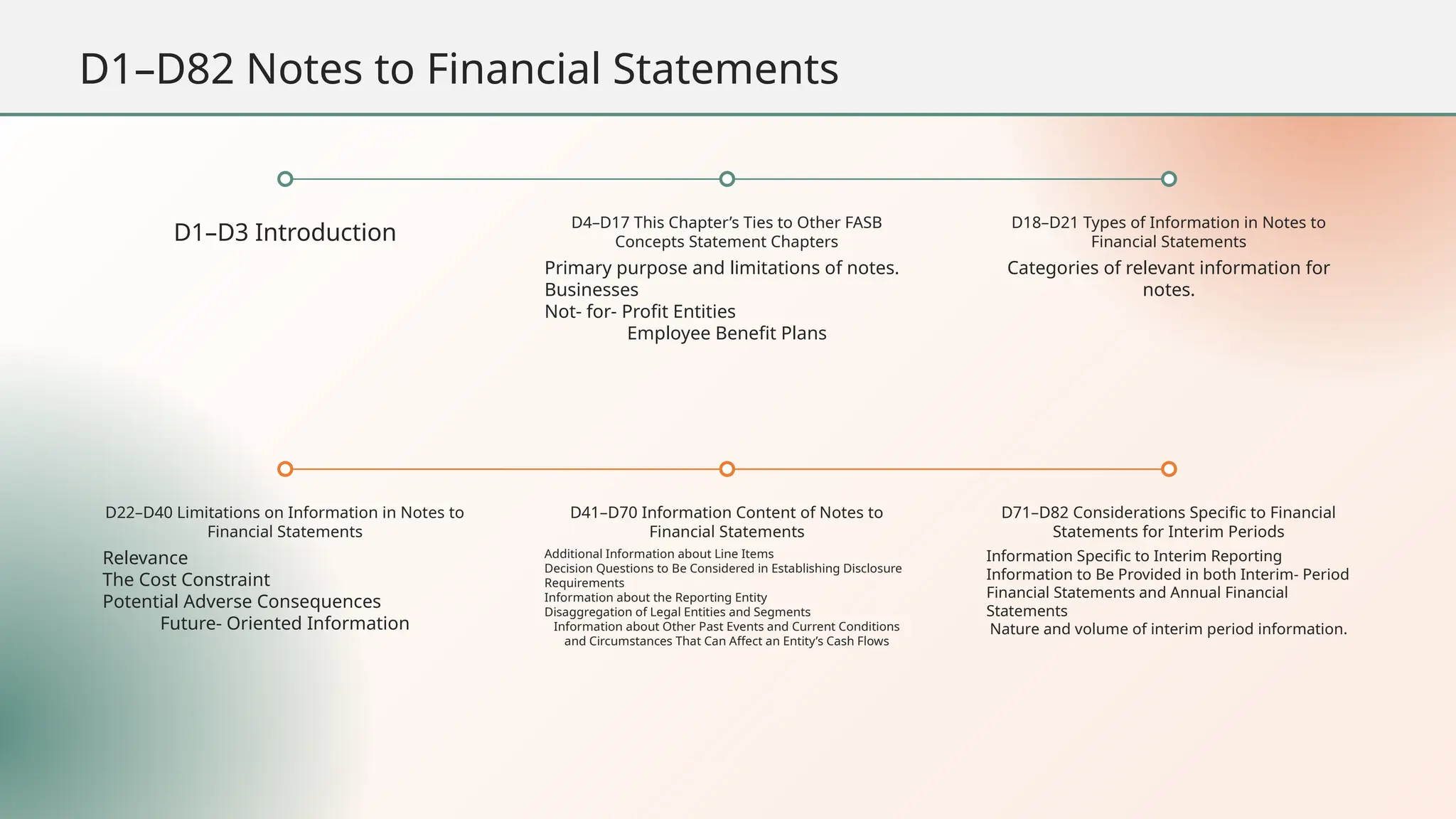

D1–D3 Introduction

D22–D40 Limitationson Information in Notes to

Financial Statements

Relevance

The Cost Constraint

Potential Adverse Consequences

Future- Oriented Information

D4–D17 This Chapter’s Ties to Other FASB

Concepts Statement Chapters

Primary purpose and limitations of notes.

Businesses

Not- for- Profit Entities

Employee Benefit Plans

D41–D70 Information Content of Notes to

Financial Statements

Additional Information about Line Items

Decision Questions to Be Considered in Establishing Disclosure

Requirements

Information about the Reporting Entity

Disaggregation of Legal Entities and Segments

Information about Other Past Events and Current Conditions

and Circumstances That Can Affect an Entity’s Cash Flows

D18–D21 Types of Information in Notes to

Financial Statements

Categories of relevant information for

notes.

D71–D82 Considerations Specific to Financial

Statements for Interim Periods

Information Specific to Interim Reporting

Information to Be Provided in both Interim- Period

Financial Statements and Annual Financial

Statements

Nature and volume of interim period information.

D1–D82 Notes to Financial Statements