Downloaded 266 times

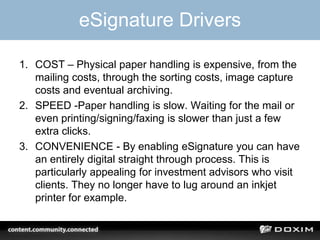

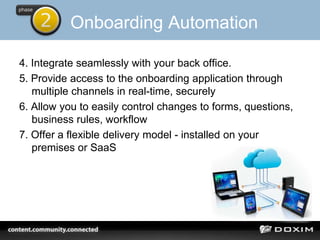

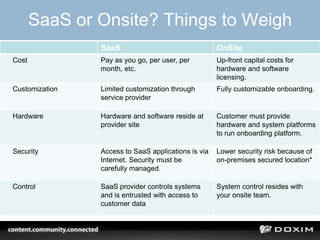

The document discusses choosing an automated client onboarding solution. It recommends buying rather than building a solution, as building in-house often costs more than expected. When choosing a solution, firms should consider whether it will be SaaS-based or on-site, how to integrate it with back-office systems, and whether it allows for configuration and incremental growth. Mobile and e-signature capabilities are also important to meet client needs and drive efficiencies. Automating high-volume account types first provides the best return on investment.