Download to read offline

![View from the Middle™ | CIT Aerospace Outlook

© 2015 CIT Group Inc. CIT and the CIT logo are registered service marks of CIT Group Inc. 3

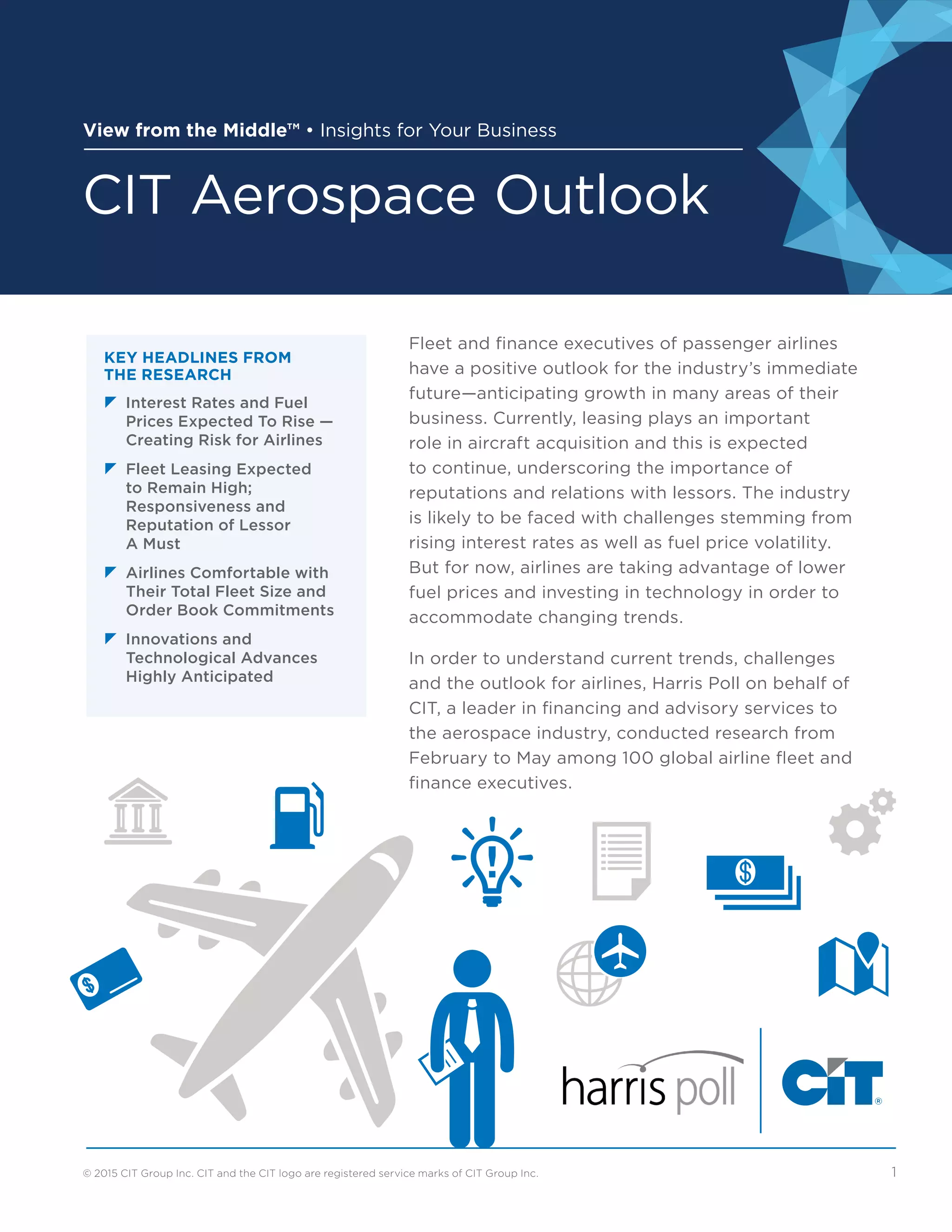

Despite the unpredictability

of fuel prices, the general outlook

is that they will RISE

And while fuel price volatility is an anticipated

challenge that airlines will face over the next two

years, executives believe fuel price volatility has

no impact or a positive impact on their airlines'

plans to acquire new technology.

z 10% of executives believe fuel price volatility

will have a very positive impact on

their airlines' plans to acquire new

technology aircraft while 28% feel the

impact will be somewhat positive

z 25% feel it has no impact at all

Among other challenges likely to be

faced in the next two years, in particular

by increases in competition, one

executive feels:

In the U.S., perhaps there has been

more focus on control of the routes,

and rights to certain cities or routes,

but for us [in Latin America], we have

to focus on the newcomers to the

market, new airlines from Europe

or the U.S. We need to find better

ways to compete against them.

- Fleet director

Despite anticipated increases in fuel

prices, the top three actions taken by fleet

and finance executives to take advantage

of current fuel prices are:

1. Hedged at current fuel prices

2. Reduced ticket prices

3. Increased utilization

of current fleet

continuedFuture Challenges

Increase in the next

18 months

Increase in

the next

3 years

Increase in

the next

5 years

50%

80%

82%](https://image.slidesharecdn.com/citaerospaceoutlookreport-151029173214-lva1-app6891/85/CIT-Aerospace-Outlook-Report-3-320.jpg)

![View from the Middle™ | CIT Aerospace Outlook

© 2015 CIT Group Inc. CIT and the CIT logo are registered service marks of CIT Group Inc. 5

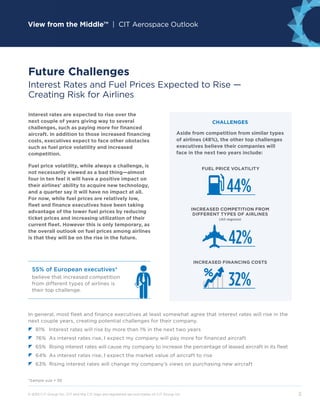

In five years, fleet and finance executives

anticipate leasing a higher percentage of

narrow body (on average 52%) than wide body

(on average 32%) aircraft.

When leasing aircraft from an operating lessor,

key areas of importance relate to lease terms

and characteristics of the lessor*.

z 62% Lease terms

z 53% Lessor’s responsiveness to my requests

z 48% Efficiency of lease negotiation process

z 44% Lessor’s reputation and experience

continued

As mentioned by one executive, the

“whole package” of a lessor and their

company is what matters most:

It is not just about [delivering] the

airplane; it is about having access

to the reserves, knowing how the

delivery is going to go, how the

re-delivery is going to go. We look

at the whole package. So it is:

do you feel comfortable with the

people you are going to be dealing

with in the company and know

that they are going to deliver

on those issues?

– C-suite executive

More than half of airline and fleet executives

expect their airline to increase the number of

routes, flights and aircraft in the next two years.

Future Plans

*Percentages may not add up to 100 because of acceptance of multiple answers from respondents answering that question.

Plans Over Next Two Years](https://image.slidesharecdn.com/citaerospaceoutlookreport-151029173214-lva1-app6891/85/CIT-Aerospace-Outlook-Report-5-320.jpg)

The CIT Aerospace Outlook report reveals a positive outlook among fleet and finance executives for the airline industry, despite anticipated challenges such as rising interest rates and fuel price volatility. Executives emphasize the importance of leasing in aircraft acquisition and expect to increase investments in technology to adapt to market changes. Key findings include an anticipated rise in leasing for narrow-body aircraft and a push towards innovations like personal device streaming for in-flight entertainment.