A look at child support laws and legal information in Ontario.

Want to reach us? We can be found at:

1120 Finch Ave W, North York, ON M3J 3H7

(416) 650-1300

http://www.torontodivorcelaw.com

“Kiddie Tax” is the term used for the tax on certain unearned

income of children taxed at the parent’s rate instead

of the child’s rate. Children typically are in a lower

tax bracket than their parents and the Kiddie Tax was developed

to prevent parents from lowering their tax liability

by shifting investment income assets to their children.

Webinar for Accountants - Get an easy-to-understand overview of all things child support. What are assessments? Can they be reviewed? What options for agreements are there?

Note: prices shown in the video might not be reflective of our current prices. Please, refer to the website for updated information. Thank you.

“Kiddie Tax” is the term used for the tax on certain unearned

income of children taxed at the parent’s rate instead

of the child’s rate. Children typically are in a lower

tax bracket than their parents and the Kiddie Tax was developed

to prevent parents from lowering their tax liability

by shifting investment income assets to their children.

Webinar for Accountants - Get an easy-to-understand overview of all things child support. What are assessments? Can they be reviewed? What options for agreements are there?

Note: prices shown in the video might not be reflective of our current prices. Please, refer to the website for updated information. Thank you.

Effective February 1, 2017, New Jersey child support automatically terminates at age 19, unless certain circumstances exist. Find out how your child support may change, and get answers to your child support questions.

Wayne Lippman presents Tax Filing Status GuideWayne Lippman

Who should file their tax? Wayne Lippman explains.

Determine the most advantageous (and allowable) filing status for the taxpayer.

Overview of all 5 filing statii:

Married Filing Jointly (not legally separated)

Qualifying Widow(er) with Dependent Child

Head of Household

Single

Married Filing Separately (Taxpayer either Itemizes or claims 0 standard deductions, if spouse itemized deductions)

*Confirm marital status on the last day of the tax year

How to plan for your personal and financial affairs now, so that YOU (not the state of Michigan) determine what happens to your children and assets when you become incapacitated or die.

The role of judiciary & the legal procedure in an adoption case by dr alka mu...alka mukherjee

Central Adoption Resource Authority (CARA) is the nodal agency to monitor and regulate in-country and intra-country adoption and is a part of Ministry of Women and child care.

Following are the certain essential conditions in order to be eligible to adopt a child:

• The procedure for adoption is different in case of Indian citizen, NRI or a foreign citizen and a child can be adopted by any of the three.

• Irrespective of their gender or marital status, any person is eligible to adopt.

• Provided that a couple is adopting a child, they should have completed two years of stable marriage and both should agree for the adoption.

• 25 years should be the minimum age difference between the child and the adoptive parents.

WHEN CAN A CHILD BE ELIGIBLE TO BE ADOPTED?

• Any orphan, surrendered or abandoned child is legally declared free for adoption by the child welfare committee as per the guidelines of the Central Government of India.

• A child without a legal parent or a guardian or the parents are not capable of taking care of the child anymore is said to be an orphan.

• When a child is deserted or unaccompanied by parents or a guardian and the child welfare committee has declared the child to be abandoned, a child is considered to be abandoned.

• Renounce on account of physical, social and emotional factors that are beyond the control of parents or the guardian is called a surrendered child as declared by the child welfare committee.

• In case of adoption, a child requires to be “legally free”. A child is considered to be legally free if even after trying their level best the police fails to find the true parent or guardian of the child.

WHAT ARE THE NORMAL CONDITIONS TO BE FULFILLED BY PARENTS?

• The adoptive parents need to be mentally, physically and emotionally stable.

• The adoptive parents should be financially stable.

• The adoptive parents should not be suffering from any life- threatening diseases.

• Apart from cases of special needs children, couples with three or more kids are not allowed for adoption.

• A single female is allowed to adopt a child of any gender but a single male is not allowed to adopt a girl child.

• The maximum age limit of a single parents should be 55 years.

The mutual rights and obligations of parents and children in Estonia. Estonian Family Law Act. Parent's right of custody. Representation of child. Equirement for surrender of child and determining access to child. Separation of child from family. Termination of joint right of custody. Right of access. Estonia’s Supreme Court’s position.

CDF Texas Public Benefits Training 2011100% Campaign

Training for Title I, School Nurses, CIS workers, Counselors, Social Workers, Benefit Coordinators and other staff working with families and employees in Texas school districts. The training covers: Children’s Medicaid, the Children’s Health Insurance Program (CHIP), and the Earned Income Tax Credit/Child Tax Credit (EITC/CTC).

Effective February 1, 2017, New Jersey child support automatically terminates at age 19, unless certain circumstances exist. Find out how your child support may change, and get answers to your child support questions.

Wayne Lippman presents Tax Filing Status GuideWayne Lippman

Who should file their tax? Wayne Lippman explains.

Determine the most advantageous (and allowable) filing status for the taxpayer.

Overview of all 5 filing statii:

Married Filing Jointly (not legally separated)

Qualifying Widow(er) with Dependent Child

Head of Household

Single

Married Filing Separately (Taxpayer either Itemizes or claims 0 standard deductions, if spouse itemized deductions)

*Confirm marital status on the last day of the tax year

How to plan for your personal and financial affairs now, so that YOU (not the state of Michigan) determine what happens to your children and assets when you become incapacitated or die.

The role of judiciary & the legal procedure in an adoption case by dr alka mu...alka mukherjee

Central Adoption Resource Authority (CARA) is the nodal agency to monitor and regulate in-country and intra-country adoption and is a part of Ministry of Women and child care.

Following are the certain essential conditions in order to be eligible to adopt a child:

• The procedure for adoption is different in case of Indian citizen, NRI or a foreign citizen and a child can be adopted by any of the three.

• Irrespective of their gender or marital status, any person is eligible to adopt.

• Provided that a couple is adopting a child, they should have completed two years of stable marriage and both should agree for the adoption.

• 25 years should be the minimum age difference between the child and the adoptive parents.

WHEN CAN A CHILD BE ELIGIBLE TO BE ADOPTED?

• Any orphan, surrendered or abandoned child is legally declared free for adoption by the child welfare committee as per the guidelines of the Central Government of India.

• A child without a legal parent or a guardian or the parents are not capable of taking care of the child anymore is said to be an orphan.

• When a child is deserted or unaccompanied by parents or a guardian and the child welfare committee has declared the child to be abandoned, a child is considered to be abandoned.

• Renounce on account of physical, social and emotional factors that are beyond the control of parents or the guardian is called a surrendered child as declared by the child welfare committee.

• In case of adoption, a child requires to be “legally free”. A child is considered to be legally free if even after trying their level best the police fails to find the true parent or guardian of the child.

WHAT ARE THE NORMAL CONDITIONS TO BE FULFILLED BY PARENTS?

• The adoptive parents need to be mentally, physically and emotionally stable.

• The adoptive parents should be financially stable.

• The adoptive parents should not be suffering from any life- threatening diseases.

• Apart from cases of special needs children, couples with three or more kids are not allowed for adoption.

• A single female is allowed to adopt a child of any gender but a single male is not allowed to adopt a girl child.

• The maximum age limit of a single parents should be 55 years.

The mutual rights and obligations of parents and children in Estonia. Estonian Family Law Act. Parent's right of custody. Representation of child. Equirement for surrender of child and determining access to child. Separation of child from family. Termination of joint right of custody. Right of access. Estonia’s Supreme Court’s position.

CDF Texas Public Benefits Training 2011100% Campaign

Training for Title I, School Nurses, CIS workers, Counselors, Social Workers, Benefit Coordinators and other staff working with families and employees in Texas school districts. The training covers: Children’s Medicaid, the Children’s Health Insurance Program (CHIP), and the Earned Income Tax Credit/Child Tax Credit (EITC/CTC).

I found various examples of rehearsal techniques that will be useful for my A2 Drama and Theatre Studies exam, and wrote them as part of a slideshow so that it's easy to access.

91% of online consumers check their email daily.

Email marketing is the engine room of your inbound marketing strategy. It can help accelerate people through your funnel and create new leads for your company.

Join us for this live webinar to discuss how you can set up an effective email marketing program to generate and nurture leads for your company.

After viewing this webinar you will learn how to:

Create persona driven email marketing campaigns

Build lead nurturing to help educate your prospects from site visit to customer

Use context to drastically improve your stats

Generate new leads from email

"Child Support Consulting have extensive experience in Child Support help, having worked in the CSA for nearly a decade. This provides them with behind the scenes insights into how Child Support Agency operates, and how best to ensure you are only paying the minimum payments each year.

Help with child support required strong work ethics, a culture of helping others and a determination to ensure their clients are of the greatest importance."

"Child Support Consulting have extensive experience in Child Support help, having worked in the CSA for nearly a decade. This provides them with behind the scenes insights into how Child Support Agency operates, and how best to ensure you are only paying the minimum payments each year.

Help with child support required strong work ethics, a culture of helping others and a determination to ensure their clients are of the greatest importance."

The federal gift tax, when applicable, is levied upon giver of the gift or donor (not the recipient, referred to as the donee). Its purposed is to create a lifetime transfer tax on inter-generational gifts in order to back up the existing estate tax levied upon transfers at death.

The federal gift tax, when applicable, is levied upon the giver of the gift or donor (not the recipient, referred to as the donee). Its purpose is to create a lifetime transfer tax on inter-generational gifts in order to back up the existing estate tax levied upon transfers at death.

Surviving a Refundable Credit Due Diligence Auditgppcpa

As a tax preparer, you must be aware of the stiff penalties for failing to meet IRS due diligence requirements. Understand that both you and your clients are at risk of being assessed penalties by the IRS

Covid19 guidance for multiemployer plans and labor unions webinarWithum

COVID-19 Guidance: Multiemployer Plans and Labor Unions

In this webinar we talk about how COVID-19 is impacting Multiemployer Plans and Labor Unions, including relief programs and FAQs

A college education increases your child’s ability to think critically, advance in a career, contribute to the community and better understand the world. No wonder choosing the right college is such an important task. Your child and you must carefully consider the many aspects of a college – academic offerings, size, location, and campus life – to ensure the best possible match with his/her academic, personal and career interests. The right college choice must be affordable as well. Financial aid is available in many forms to help students meet college costs. This assistance is intended to supplement, not replace, the efforts of students and families. This guide gives parents and students the basic information needed to begin securing financial aid. It will help you find the information you need to ask the right questions and make informed decisions about managing college costs.

Source: https://ebookschoice.com/making-money-wise-college-decisions/

In 2011, the Pennsylvania legislature passed Act 112 of 2010. This legislation significantly changed the child custody law in Pennsylvania. Parents who find themselves in a fight for custody of a child should know the basics of the Pennsylvania child custody law and how the law is applied in Montgomery County, Pennsylvania.

How to Obtain Permanent Residency in the NetherlandsBridgeWest.eu

You can rely on our assistance if you are ready to apply for permanent residency. Find out more at: https://immigration-netherlands.com/obtain-a-permanent-residence-permit-in-the-netherlands/.

A "File Trademark" is a legal term referring to the registration of a unique symbol, logo, or name used to identify and distinguish products or services. This process provides legal protection, granting exclusive rights to the trademark owner, and helps prevent unauthorized use by competitors.

Visit Now: https://www.tumblr.com/trademark-quick/751620857551634432/ensure-legal-protection-file-your-trademark-with?source=share

Responsibilities of the office bearers while registering multi-state cooperat...Finlaw Consultancy Pvt Ltd

Introduction-

The process of register multi-state cooperative society in India is governed by the Multi-State Co-operative Societies Act, 2002. This process requires the office bearers to undertake several crucial responsibilities to ensure compliance with legal and regulatory frameworks. The key office bearers typically include the President, Secretary, and Treasurer, along with other elected members of the managing committee. Their responsibilities encompass administrative, legal, and financial duties essential for the successful registration and operation of the society.

WINDING UP of COMPANY, Modes of DissolutionKHURRAMWALI

Winding up, also known as liquidation, refers to the legal and financial process of dissolving a company. It involves ceasing operations, selling assets, settling debts, and ultimately removing the company from the official business registry.

Here's a breakdown of the key aspects of winding up:

Reasons for Winding Up:

Insolvency: This is the most common reason, where the company cannot pay its debts. Creditors may initiate a compulsory winding up to recover their dues.

Voluntary Closure: The owners may decide to close the company due to reasons like reaching business goals, facing losses, or merging with another company.

Deadlock: If shareholders or directors cannot agree on how to run the company, a court may order a winding up.

Types of Winding Up:

Voluntary Winding Up: This is initiated by the company's shareholders through a resolution passed by a majority vote. There are two main types:

Members' Voluntary Winding Up: The company is solvent (has enough assets to pay off its debts) and shareholders will receive any remaining assets after debts are settled.

Creditors' Voluntary Winding Up: The company is insolvent and creditors will be prioritized in receiving payment from the sale of assets.

Compulsory Winding Up: This is initiated by a court order, typically at the request of creditors, government agencies, or even by the company itself if it's insolvent.

Process of Winding Up:

Appointment of Liquidator: A qualified professional is appointed to oversee the winding-up process. They are responsible for selling assets, paying off debts, and distributing any remaining funds.

Cease Trading: The company stops its regular business operations.

Notification of Creditors: Creditors are informed about the winding up and invited to submit their claims.

Sale of Assets: The company's assets are sold to generate cash to pay off creditors.

Payment of Debts: Creditors are paid according to a set order of priority, with secured creditors receiving payment before unsecured creditors.

Distribution to Shareholders: If there are any remaining funds after all debts are settled, they are distributed to shareholders according to their ownership stake.

Dissolution: Once all claims are settled and distributions made, the company is officially dissolved and removed from the business register.

Impact of Winding Up:

Employees: Employees will likely lose their jobs during the winding-up process.

Creditors: Creditors may not recover their debts in full, especially if the company is insolvent.

Shareholders: Shareholders may not receive any payout if the company's debts exceed its assets.

Winding up is a complex legal and financial process that can have significant consequences for all parties involved. It's important to seek professional legal and financial advice when considering winding up a company.

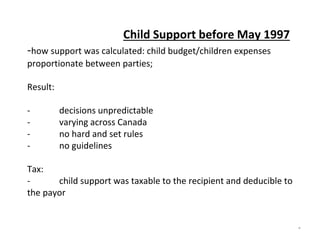

1. Child Support before May 1997

-how support was calculated: child budget/children expenses

proportionate between parties;

Result:

- decisions unpredictable

- varying across Canada

- no hard and set rules

- no guidelines

Tax:

- child support was taxable to the recipient and deducible to

the payor

*

2. Child support after May 1, 1997

• Federal Government introduced Child Support Guidelines and

amended the Divorce Act. As a result:

1. child support is not taxable or deductible;

2. any child support order made on or after May 1, 1997,

must be in accordance with the FCSG.

• However, for those recipients who are receiving child

support pursuant to an Order or Agreement dated on or

before May 1, 1997, must continue to pay tax on support and

payor can deduct support paid until the Order/ Agreement is

varied.

*

3. Purpose of FCSG

• S.1(a) of the FCSG - The objectives of the Guidelines are:

(a) “to establish a fair standard for children that ensures that they

continue to benefit from the financial means of both spouses after

separation;

(b) to reduce the conflict and tension between the spouses by making

the calculation of child support Orders more objective;

(c) to improve the efficiency of the legal process by giving courts and

spouses guidance in setting the levels of child support orders and

encouraging settlement; and,

(d) to ensure consistent treatment of spouses and children who are in

similar circumstances.

*

4. Who Can Claim Support?

• under the Divorce Act only a spouse or former spouse can

claim support

• a child has no standing to bring a claim pursuant to the

Divorce Act/ can do so under provincial legislation

*

5. Who is entitled to Support?

• under Divorce Act – s. 15 (1) – child must be a “child of the

marriage”

• Definition – “child of the marriage” – (s.2(1)) child of two

spouses (former spouses), even if one parent is not the

biological parent (but stands in loco parentis) who at the time

is:

• (a) under the age of majority (18) and has not withdrawn

from parental control;

• (b) is age of majority and over, and under parental control ,

but unable bc of illness, disability, or any other cause to

withdraw from parental charge or to obtain the necessities of

life

*

6. • under the Family Law Act – s.31 (2) - for child to be eligible,

the child must be:

• unmarried;

• a minor (under 18 yrs of age) or enrolled in a full time

program of education; and,

• if 16 yrs or older still has not withdrawn from parental control

*

7. Obligation to Pay Support

• either the child’s parents or individuals who are loco parentis

to the child

• loco parentis – spouse or former spouse who “stands in the

place of a parent” (s.2(2) of the Divorce Act (step- parent) /

assumes the role of a parent

• under the FLA – s.1(1) – a person who has demonstrated a

“settled intention to treat a child as a child of his/her family

(not foster parent).

*

8. • Chartier v. Chartier (1998) SCJ No. 79 (S.C.C.) – test for

settled intention – objective test – case by case:

• all factors are relevant and must be considered in

determining a child’s relationship with parent;

• court looks at financial provision / social interaction/ role in

discipline and education;

• person cannot terminate the parent relationship – right

belongs to the child;

*

9. How the Guidelines Work

• the tables and rules for the determination of child support are

set out in the Family Law Act and the Divorce Act - child

support guidelines;

• in Ontario there is the federal child support guidelines

(divorce act) and the Ontario child support guidelines (family

law act) – claim support under both acts

• depends if advance case under the divorce act or family law

act/ minor differences under the wording of the two sets of

guidelines/ amounts of child support under provincial is the

same as federal

*

10. Amount of Child Support

• tables are formulated based on mathematical formula/ based

on average spending on children in families at difference

levels of income

• when looking at the tables, only consider the payors income

(tables only show the basic s. 3 support) you must determine

the total taxable income for the year for the payor

• the total income is by reviewing line 101 of your income tax

act and making the necessary deductions and additions as per

Schedule III of the Guidelines

• usually look at line 150 income as set out in Income tax

return, but income for support purposes may be greater than

disclosed income on line 150

*

11. • Presumptive Rule – s.3(1) of the FCSG –

“Unless otherwise provided under the Guidelines, the amount

of support order for children under the age of majority is-

(a) the amount as set out in the applicable

table, according to the

number of children under the

age of majority to whom the order relates and

the income of the spouse against

whom the order is

sought; and,

(b) the amount, if any, determined under s. 7;

*

12. Income over $150,000

• s. 4 of the FCSG - for incomes over $150,000, the amount of

support is determined as follows:

• a. Amount as determined under s. 3 of the FCSG (based on

Table); OR,

• b. If the court believes this amount is inappropriate, the

amount of support as determined by the Table for the first

$150,000 and wrt the balance of the payor’s income, a

discretionary amount having regard to the condition, means,

needs and other circumstances of the children who are

entitled to support and the financial ability of each spouse to

contribute to the support of the children;

• c. the amount, if any, as determined under s. 7 of the FCSG.

*

13. • Presumption in favour of guideline amount

• Need “clear and compelling evidence” to depart from

guideline amount

• Payor must rebut presumption

• Large quantum of support by itself not a reason to depart

from guideline amount

• Consider child care budget

• Francis v. Baker (1998) SCJ no. 52 (S.C.C.) – need to balance

principles of predictability, consistency and efficiency with

fairness, flexibility and recognition of the actual condition,

needs, means and other circumstances of the children.

*

14. Income that Fluctuates

• S.16 of FCSG – Subject to s. 17-20 (ie. Pattern of income, pre-

tax corporate income, imputing income, non-resident),

annual income for support purposes is based on “total

income” in T1 General ITR and adjusted in accordance with

Schedule III (adjustments to income);

• S.17 of the FCSG - if income fluctuates, court can average over

the last three years and determine an amount that is fair and

reasonable;

• Discretionary by court ;

• Onus on payor to deviate from s.16 of the FCSG (i.e.. Line 150

etc.);

*

15. Corporate Income

• s.18 of the FCSG– a court may include all or part of the

company’s pre-tax corporate earnings (or retained earnings in

corp) if the court is of the opinion that income is available to

the payor for the purposes of paying support;

• court can also add back into income, wages paid to former or

current spouse from corp – amount that reflects the work

performed by the spouse for the corporation

*

16. Impute Income

• s.19 of FCSG – court may income if the parent is intentionally

underemployed or unemployed;

• impute income because both parents have an obligation to

support the children;

• parent must earn what he is capable of earning;

• don’t need to prove that the payor is intending to avoid his

support obligations;

*

17. Special or Extraordinary Expenses

• In addition to s. 3 support, payors must also pay their share of

any special or extraordinary expenses (s.7 expenses);

• s. 7 expenses are to be shared by the parties in proportion to

their incomes, after deducting from the expense, the

contribution from the child, if any, and any “ subsidies,

benefits, or income tax deductions or credits in relation to the

expense”;

• payor pays the net proportionate share of the expense

*

18. • s. 7 FCSG - Special or Extraordinary expenses:

- child care expenses (must be incurred as a result of the

parent’s employment, illness, disability or education or

training for employment);

- portion of medical and dental insurance premiums

attributed to the child;

- health related expenses that exceed insurance

reimbursement (ie. Orthodontic treatment, counseling etc.)

- extraordinary expenses for primary or secondary school;

- expenses for post-secondary education;

- extraordinary expenses for extracurricular activities

*

19. • Two part test to determine if a claimed expense is to be

included in the quantum of child support;

• The court must determine if the expense is “reasonable and

necessary” ;

• “necessary” in relation to the best interests of the child;

• “reasonable” having regard to the means of the spouses and

those of the children and the family pattern of spending

before the separation ( only for those expenses outside of the

specified expenses);

*

20. • Two categories of special expenses, the expense (not the

activity) must be “extraordinary”:

- primary and secondary school (or

educational program)

- expenses in relation to extracurricular

activities

• s. 7 (1.1) definition of “extraordinary expense”:

(a) The expense is extraordinary if it exceeds what the

recipient spouse can reasonably cover;

(b) Even if the recipient spouse can cover the expense, still

may be extraordinary, if it exceeds what the recipient

spouse can reasonably cover, the nature and number of

educational programs or extracurricular activities, special

needs and talents of child, overall cost of the program or

activity;

*

21. • if child support is a large amount, court may not order s.7

expense because not extraordinary

• extraordinary extracurricular expenses often a source of

contention – but the test is if the expenses is necessary and

reasonable;

• expense can be anticipated bf the court orders contribution;

• expense can also be retroactive if payor does not pay;

• court can order a fixed amount paid based on the activity or

the court can order a % based on future activities;

*

22. • Lewi v. Lewi (2006) OJ No. 1847 (CA)- court examined what

contribution adult child should make to post- secondary

education expenses;

• court has a broad discretion to consider the amount to be

contributed by the child;

• have to consider the means of the child and those of the

parent;

• no formula to consider the amount to be paid by the child;

*

23. • extracurricular activities – s. 3 base support includes some

allowance for usual or ordinary extracurricular activities;

• Although s. 7 does not specify that consent is required bf

enrolling a child in an extracurricular activity, the courts have

held that custodial parents cannot just enroll the children in

all kinds of expensive extracurricular activities and then

demand contribution from the payor;

• s. 7 (1) (f) is unusual extraordinary or special expenses for

extracurricular activities;

*

24. EXCEPTION TO PRESUMPTION

Exceptions to presumption that the quantum of child support

is based solely on the table amount (court has discretion to

determine the amount of support):

- Adult child

- payor income over $150,000

- loco parentis

- shared/ split custody

- Undue hardship

*

25. ADULT CHILD

• s. 3(2) of the FCSG - if the child is over the age of 18, the

amount of support is determined as follows:

• as per the FCSG as if the child was a minor;

• if the amount if inappropriate, an amount that the court says

is appropriate having regard to the means, needs and other

circumstances of the child and the ability of each spouse to

support the child;

*

26. • expectation that adult children going to school are going to

contribute something to their support;

• court can consider if s. 3 (2) guideline support is appropriate

for a adult child when considering s. 7 expenses for adult child

(i.e.. Child goes away to school). No standard set formula.

Maybe four months out of the year when the child resides at

home or partial during the yr because the recipient must

maintain the house. Court can still order full guideline

support;

• no absolute cut off age for child support

*

27. • if adult child has sufficient income or assets, even if in school

may not be entitled to support depending on his needs and

the means of the parents;

• guideline support may be inappropriate if adult child has

resources;

• if adult child rejects parent, some courts have refused to

grant adult child support. Not the case for minor kids, must

continue to pay support even if they have rejected their

parents;

*

28. s.5 - support by step parent

• obligation of biological parent and loco parentis to support

child;

• court may vary the quantum of support;

• primary obligation is biological parent with step parent also

contributing;

• No set rules as to how to calculate the support obligation

from a step parent (may get full guidelines from both/ set off/

difference etc. );

*

29. • income of recipient – irrelevant in most cases

except for the following:

- s. 7 expenses

- shared custody

- split custody

- income over $150K

- undue hardship

*

30. Split Custody

• s. 8 of the FCSG – Split Custody

• Both spouses have full custody of one or more of the children;

• amount of support is the difference paid by each spouse to

the other (eg. one spouse’s support obligation is $1000 per

month, the other spouse’s obligation is $400 per month, the

spouse with the greater income will pay $600 to the other

spouse);

*

31. shared custody – 40%

• S. 9 of the FCSG - if one spouse has the right to access or

custody of child for 40% or more of time over the year,

quantum of support based on amount set out in table,

increased cost of shared custody arrangement and condition,

means, needs and other circumstances of each spouse and of

the children;

• no single method of determining 40%– hours/ days - look at

hours, discount time at school friends etc. – start from the

assumption that the custodial parent has 100%)

*

32. • Contino v. Leonelli- Contino (2005) S.C.J. No. 65 (S.C.C.) – child

support in shared custody situation requires the exercise of

discretion and not just a set – off;

• may be a starting point and then gross up because of the

increased cost with both homes – don’t want to have a large

difference in the standard of living between both houses-

court has discretion;

• just because a payor reaches a 40% threshold does not

necessarily mean that support is reduced

*

33. The amount of support is determined as follows:

• Determine if the 40% threshold has been met;

• Determine the parties incomes for support purposes -

amount set out in Applicable Table for each spouse;

• Increased cost arrangements – examine budgets and actual

expenditures wrt children;

• Condition, means, needs of each spouse and the child of the

marriage – broad discretion;

• examine actual spending patterns wrt children/ ratio of

incomes/ net worth of parties/ standard of living for the

children in each household; *

34. Hardship

• s. 10 of the FCSG – court can order a different amount of

guideline support if the amount results in hardship;

• Circumstances that may cause a payor to suffer undue

hardship in paying support: high family debts, high cost of

access, legal obligation to pay support to another person –

high threshold to meet the test;

• s. 3, 4 (income over $150k), 5 (loco parentis), 8 (split

custody), 9 (shared custody) – may apply to vary the amount

of support if undue hardship;

*

35. • firstly, the applying spouse must have a standard of living that is

lower than the recipient ;

• hardship must be exceptional or excessive / very high threshold;

• List in s. 10(2) is not exhaustive (includes the following);

• Circumstances relate to payor not recipient at this stage;

• If hardship – court then considers the standard of living of each

household. Payor must have lower standard of living than

recipient. Must consider all income earners in household;

• If yes, then determine the amount of support to be paid. Need to

look at means and needs of the parties (income and expenses of

both households)

*

36. PRIORITY OF CHILD SUPPORT

• child support has priority over spousal support;

• The quantum of child support may impact the quantum of

spousal support;

• As a result, any future change in child support, may result in a

change in the quantum of spousal support.

*

37. ONGOING INCOME INFORMATION

• s. 25 - under the FCSG, as long as support is owing, the

recipient spouse may obtain, on request (not more than once

per year), information wrt income from the payor spouse;

• recipient spouse income – (important wrt s. 7 , split or shared

custody) also must provide information wrt her income upon

request

*

38. • Any existing Order and new Orders made after March 2010

(not apply to existing Agreements)- the payor must

automatically provide his/her income information (unless the

parties agree otherwise) within 30 days of the anniversary of

the Order (s.24.1 and s.25.1 of the FCSG);

• Recipient must also automatically provide her information (s.

7, split, shared custody) if her income was necessary to

determine support;

• Must provide Income Tax Return and Notice of Assessment

and any other document to substantiate your income as set

out in s. 21 of the FCSG;

*