2-2

After studying Chapter4,

you should be able to:

Define “capital budgeting” and identify the steps involved in the

capital budgeting process.

Justify why cash, not income, flows are the most relevant to

capital budgeting decisions.

Summarize in a “checklist” the major concerns to keep in mind

as one prepares to determine relevant capital budgeting cash

flows.

Define the terms “sunk cost” and “opportunity cost” and explain

why sunk costs must be ignored, while opportunity costs must

be included, in capital budgeting analysis.

Explain how tax considerations, as well as depreciation for tax

purposes, affects capital budgeting cash flows.

Determine initial, operating, and terminal period “after-tax,

incremental, cash flows” associated with a capital investment

project.

Apply the various techniques of evaluating projects

3.

2-3

What is

Capital Budgeting?

Theprocess of identifying,

analyzing, and selecting

investment projects whose

returns (cash flows) are

expected to extend beyond

one year.

4.

2-4

The Capital BudgetingProcess

Generate investment proposals

consistent with the firm’s strategic

objectives.

Estimate after-tax incremental cash

flows for the investment projects.

Estimate the cost of capital relevant for

the project

Evaluate project incremental cash flows.

5.

2-5

Classification of Investment

ProjectProposals

1. New products or expansion of

existing products

2. Replacement of existing equipment or

buildings

3. Research and development

4. Exploration

5. Other (e.g., safety or pollution related)

2-7

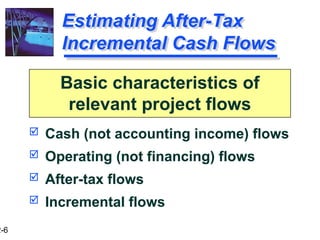

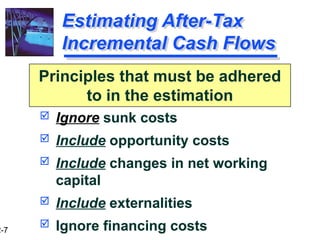

Estimating After-Tax

Incremental CashFlows

Ignore sunk costs

Include opportunity costs

Include changes in net working

capital

Include externalities

Ignore financing costs

Principles that must be adhered

to in the estimation

8.

2-8

Sunk Costs

SunkCosts—A cost that has

already been incurred and cannot

be recovered irrespective of the

decision to accept or reject the

project.

R&D, Market Research,

Consultant’s Fees

It is irrelevant

9.

2-9

Opportunity Costs

OpportunityCosts--The cash flow foregone by

using your resources in a particular way.

Resources have multiple uses

You can use them in one way to the exclusion

of other uses and this gives rise to opportunity

costs

By using your own building for your business,

you forego the rent that you could have earned

by renting it to some one else.

It is relevant to decision making.

10.

2-10

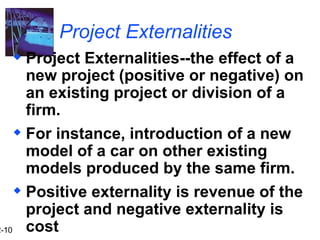

Project Externalities

ProjectExternalities--the effect of a

new project (positive or negative) on

an existing project or division of a

firm.

For instance, introduction of a new

model of a car on other existing

models produced by the same firm.

Positive externality is revenue of the

project and negative externality is

cost

11.

2-11

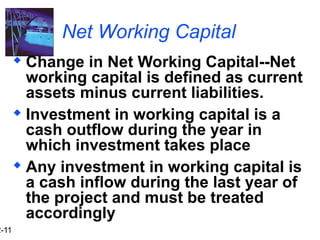

Net Working Capital

Change in Net Working Capital--Net

working capital is defined as current

assets minus current liabilities.

Investment in working capital is a

cash outflow during the year in

which investment takes place

Any investment in working capital is

a cash inflow during the last year of

the project and must be treated

accordingly

12.

2-12

Financing costs

Financingcosts are considered in

the discounting rate (the cost of

capital).

They are not considered in

determining the cash flows of the

project. Otherwise it would be

double counting.

13.

2-13

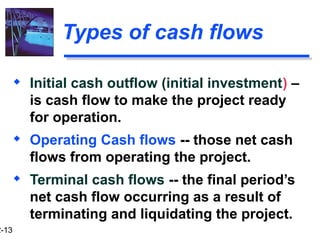

Types of cashflows

Initial cash outflow (initial investment) –

is cash flow to make the project ready

for operation.

Operating Cash flows -- those net cash

flows from operating the project.

Terminal cash flows -- the final period’s

net cash flow occurring as a result of

terminating and liquidating the project.

14.

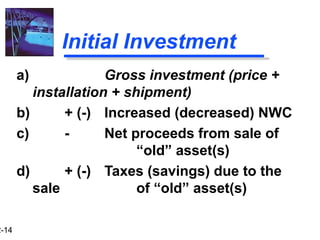

2-14

Initial Investment

a) Grossinvestment (price +

installation + shipment)

b) + (-) Increased (decreased) NWC

c) - Net proceeds from sale of

“old” asset(s)

d) + (-) Taxes (savings) due to the

sale of “old” asset(s)

15.

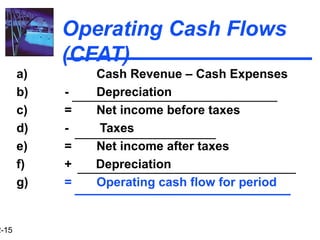

2-15

Operating Cash Flows

(CFAT)

a)Cash Revenue – Cash Expenses

b) - Depreciation

c) = Net income before taxes

d) - Taxes

e) = Net income after taxes

f) + Depreciation

g) = Operating cash flow for period

16.

2-16

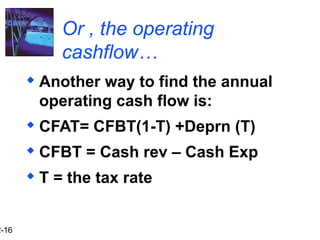

Or , theoperating

cashflow…

Another way to find the annual

operating cash flow is:

CFAT= CFBT(1-T) +Deprn (T)

CFBT = Cash rev – Cash Exp

T = the tax rate

17.

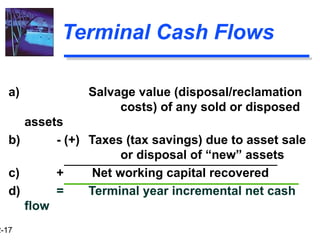

2-17

Terminal Cash Flows

a)Salvage value (disposal/reclamation

costs) of any sold or disposed

assets

b) - (+) Taxes (tax savings) due to asset sale

or disposal of “new” assets

c) + Net working capital recovered

d) = Terminal year incremental net cash

flow

18.

2-18

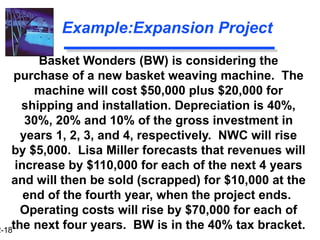

Example:Expansion Project

Basket Wonders(BW) is considering the

purchase of a new basket weaving machine. The

machine will cost $50,000 plus $20,000 for

shipping and installation. Depreciation is 40%,

30%, 20% and 10% of the gross investment in

years 1, 2, 3, and 4, respectively. NWC will rise

by $5,000. Lisa Miller forecasts that revenues will

increase by $110,000 for each of the next 4 years

and will then be sold (scrapped) for $10,000 at the

end of the fourth year, when the project ends.

Operating costs will rise by $70,000 for each of

the next four years. BW is in the 40% tax bracket.

19.

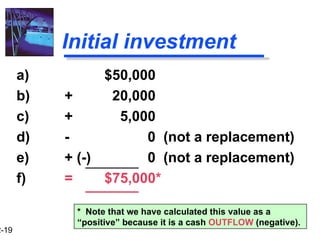

2-19

Initial investment

a) $50,000

b)+ 20,000

c) + 5,000

d) - 0 (not a replacement)

e) + (-) 0 (not a replacement)

f) = $75,000*

* Note that we have calculated this value as a

“positive” because it is a cash OUTFLOW (negative).

20.

2-20

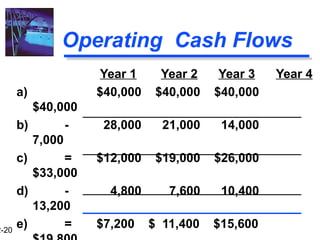

Operating Cash Flows

Year1 Year 2 Year 3 Year 4

a) $40,000 $40,000 $40,000

$40,000

b) - 28,000 21,000 14,000

7,000

c) = $12,000 $19,000 $26,000

$33,000

d) - 4,800 7,600 10,400

13,200

e) = $7,200 $ 11,400 $15,600

21.

2-21

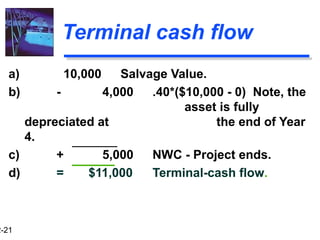

Terminal cash flow

a)10,000 Salvage Value.

b) - 4,000 .40*($10,000 - 0) Note, the

asset is fully

depreciated at the end of Year

4.

c) + 5,000 NWC - Project ends.

d) = $11,000 Terminal-cash flow.

22.

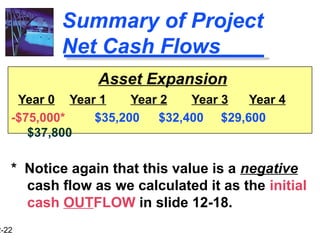

2-22

Summary of Project

NetCash Flows

Asset Expansion

Year 0 Year 1 Year 2 Year 3 Year 4

-$75,000* $35,200 $32,400 $29,600

$37,800

* Notice again that this value is a negative

cash flow as we calculated it as the initial

cash OUTFLOW in slide 12-18.

23.

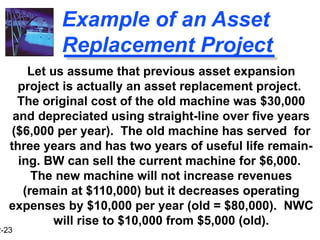

2-23

Example of anAsset

Replacement Project

Let us assume that previous asset expansion

project is actually an asset replacement project.

The original cost of the old machine was $30,000

and depreciated using straight-line over five years

($6,000 per year). The old machine has served for

three years and has two years of useful life remain-

ing. BW can sell the current machine for $6,000.

The new machine will not increase revenues

(remain at $110,000) but it decreases operating

expenses by $10,000 per year (old = $80,000). NWC

will rise to $10,000 from $5,000 (old).

24.

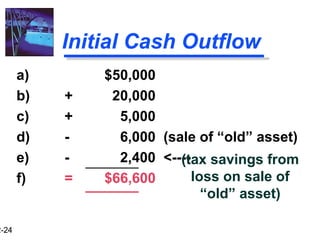

2-24

Initial Cash Outflow

a)$50,000

b) + 20,000

c) + 5,000

d) - 6,000 (sale of “old” asset)

e) - 2,400 <----

f) = $66,600

(tax savings from

loss on sale of

“old” asset)

25.

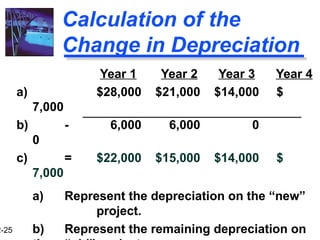

2-25

Calculation of the

Changein Depreciation

Year 1 Year 2 Year 3 Year 4

a) $28,000 $21,000 $14,000 $

7,000

b) - 6,000 6,000 0

0

c) = $22,000 $15,000 $14,000 $

7,000

a) Represent the depreciation on the “new”

project.

b) Represent the remaining depreciation on

26.

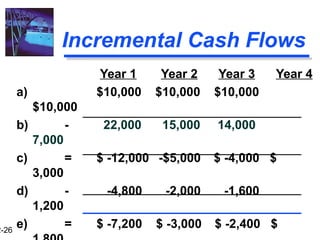

2-26

Incremental Cash Flows

Year1 Year 2 Year 3 Year 4

a) $10,000 $10,000 $10,000

$10,000

b) - 22,000 15,000 14,000

7,000

c) = $ -12,000 -$5,000 $ -4,000 $

3,000

d) - -4,800 -2,000 -1,600

1,200

e) = $ -7,200 $ -3,000 $ -2,400 $

27.

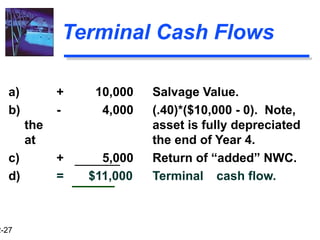

2-27

Terminal Cash Flows

a)+ 10,000 Salvage Value.

b) - 4,000 (.40)*($10,000 - 0). Note,

the asset is fully depreciated

at the end of Year 4.

c) + 5,000 Return of “added” NWC.

d) = $11,000 Terminal cash flow.

28.

2-28

Summary of Project

NetCash Flows

Asset Expansion

Year 0 Year 1 Year 2 Year 3 Year 4

-$75,000 $35,200 $32,400 $29,600

$37,800

Asset Replacement

Year 0 Year 1 Year 2 Year 3 Year 4

-$66,600 $14,800 $12,000 $10,600

$20,000

2-31

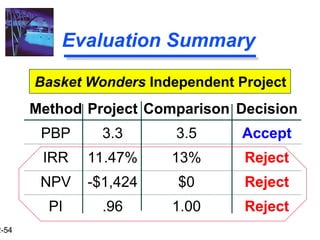

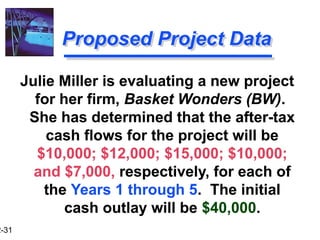

Proposed Project Data

JulieMiller is evaluating a new project

for her firm, Basket Wonders (BW).

She has determined that the after-tax

cash flows for the project will be

$10,000; $12,000; $15,000; $10,000;

and $7,000, respectively, for each of

the Years 1 through 5. The initial

cash outlay will be $40,000.

32.

2-32

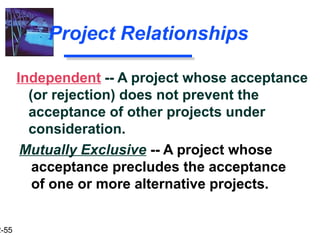

Independent Project

Independent-- A project whose

acceptance (or rejection) does not

prevent the acceptance of other

projects under consideration.

For this project, assume that it is

independent of any other potential

projects that Basket Wonders may

undertake.

33.

2-33

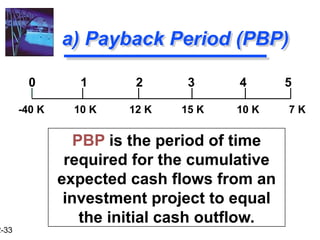

a) Payback Period(PBP)

PBP is the period of time

required for the cumulative

expected cash flows from an

investment project to equal

the initial cash outflow.

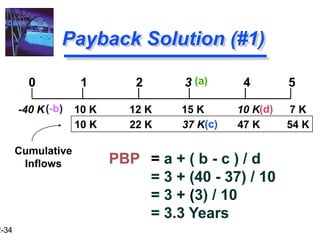

0 1 2 3 4 5

-40 K 10 K 12 K 15 K 10 K 7 K

34.

2-34

(c)

10 K 22K 37 K 47 K 54 K

Payback Solution (#1)

PBP = a + ( b - c ) / d

= 3 + (40 - 37) / 10

= 3 + (3) / 10

= 3.3 Years

0 1 2 3 4 5

-40 K 10 K 12 K 15 K 10 K 7 K

Cumulative

Inflows

(a)

(-b) (d)

35.

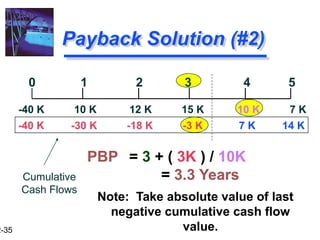

2-35

Payback Solution (#2)

PBP= 3 + ( 3K ) / 10K

= 3.3 Years

Note: Take absolute value of last

negative cumulative cash flow

value.

Cumulative

Cash Flows

-40 K 10 K 12 K 15 K 10 K 7 K

0 1 2 3 4 5

-40 K -30 K -18 K -3 K 7 K 14 K

36.

2-36

PBP Acceptance Criterion

Yes!The firm will receive back the

initial cash outlay in less than 3.5

years. [3.3 Years < 3.5 Year Max.]

The management of Basket Wonders

has set a maximum PBP of 3.5

years for projects of this type.

Should this project be accepted?

37.

2-37

PBP Strengths

and Weaknesses

Strengths:

Easy to use and

understand

Can be used as a

measure of

liquidity & risk

Weaknesses:

Does not account

for TVM

Does not consider

cash flows

beyond the PBP

Cutoff period is

38.

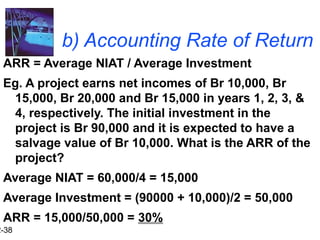

2-38

b) Accounting Rateof Return

ARR = Average NIAT / Average Investment

Eg. A project earns net incomes of Br 10,000, Br

15,000, Br 20,000 and Br 15,000 in years 1, 2, 3, &

4, respectively. The initial investment in the

project is Br 90,000 and it is expected to have a

salvage value of Br 10,000. What is the ARR of the

project?

Average NIAT = 60,000/4 = 15,000

Average Investment = (90000 + 10,000)/2 = 50,000

ARR = 15,000/50,000 = 30%

2-40

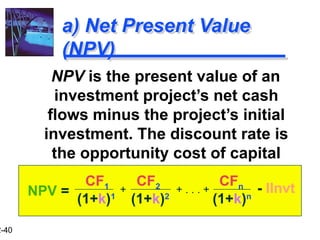

a) Net PresentValue

(NPV)

NPV is the present value of an

investment project’s net cash

flows minus the project’s initial

investment. The discount rate is

the opportunity cost of capital

CF1 CF2 CFn

(1+k)1

(1+k)2

(1+k)n

+ . . . +

+ - IInvt

NPV =

41.

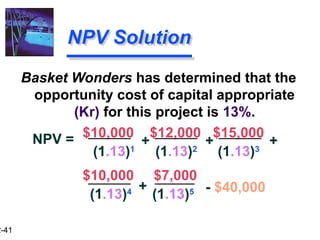

2-41

Basket Wonders hasdetermined that the

opportunity cost of capital appropriate

(Kr) for this project is 13%.

$10,000 $7,000

NPV Solution

$10,000 $12,000 $15,000

(1.13)1

(1.13)2

(1.13)3

+ +

+ - $40,000

(1.13)4

(1.13)5

NPV = +

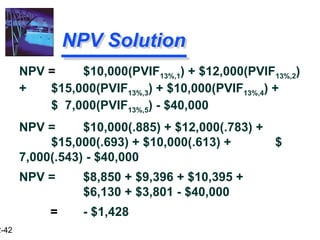

2-43

NPV Acceptance Criterion

No!The NPV is negative. This means

that the project is reducing shareholder

wealth. [Reject as NPV < 0 ]

The management of Basket Wonders

has determined that the required

rate is 13% for projects of this type.

Should this project be accepted?

44.

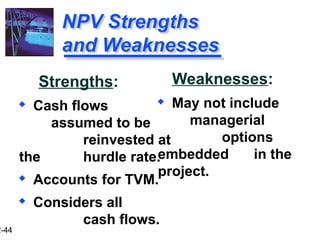

2-44

NPV Strengths

and Weaknesses

Strengths:

Cash flows

assumed to be

reinvested at

the hurdle rate.

Accounts for TVM.

Considers all

cash flows.

Weaknesses:

May not include

managerial

options

embedded in the

project.

45.

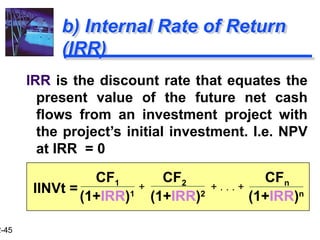

2-45

b) Internal Rateof Return

(IRR)

IRR is the discount rate that equates the

present value of the future net cash

flows from an investment project with

the project’s initial investment. I.e. NPV

at IRR = 0

CF1 CF2 CFn

(1+IRR)1

(1+IRR)2

(1+IRR)n

+ . . . +

+

IINVt =

46.

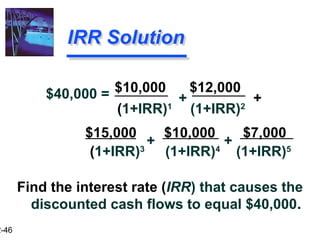

2-46

$15,000 $10,000 $7,000

IRRSolution

$10,000 $12,000

(1+IRR)1

(1+IRR)2

Find the interest rate (IRR) that causes the

discounted cash flows to equal $40,000.

+ +

+

+

$40,000 =

(1+IRR)3

(1+IRR)4

(1+IRR)5

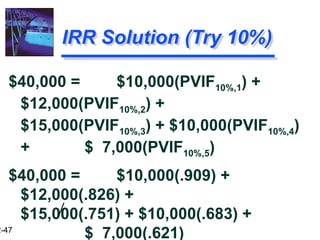

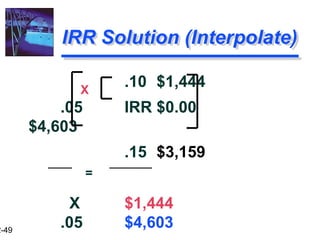

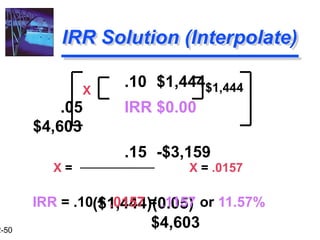

2-49

.10 $1,444

.05 IRR$0.00

$4,603

.15 $3,159

X $1,444

.05 $4,603

IRR Solution (Interpolate)

X

=

50.

2-50

.10 $1,444

.05 IRR$0.00

$4,603

.15 -$3,159

($1,444)(0.05)

$4,603

IRR Solution (Interpolate)

$1,444

X

X = X = .0157

IRR = .10 + .0157 = .1157 or 11.57%

51.

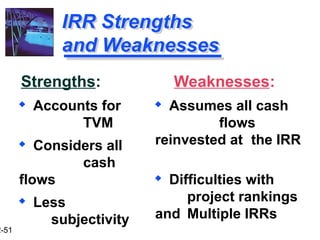

2-51

IRR Strengths

and Weaknesses

Strengths:

Accounts for

TVM

Considers all

cash

flows

Less

subjectivity

Weaknesses:

Assumes all cash

flows

reinvested at the IRR

Difficulties with

project rankings

and Multiple IRRs

52.

2-52

Profitability Index (PI)

PIis the ratio of the present value of

a project’s future net cash flows to

the project’s initial investment.

CF1 CF2 CFn

(1+k)1

(1+k)2

(1+k)n

+ . . . +

+ IInVT

PI =

PI = 1 + [ NPV / IINVT ]

<< OR >>

Method #2:

Method #1:

53.

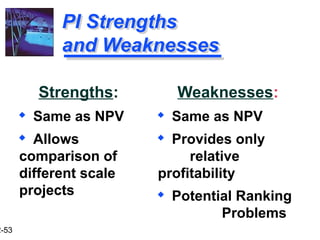

2-53

PI Strengths

and Weaknesses

Strengths:

Same as NPV

Allows

comparison of

different scale

projects

Weaknesses:

Same as NPV

Provides only

relative

profitability

Potential Ranking

Problems

2-55

Project Relationships

Mutually Exclusive-- A project whose

acceptance precludes the acceptance

of one or more alternative projects.

Independent -- A project whose acceptance

(or rejection) does not prevent the

acceptance of other projects under

consideration.

56.

2-56

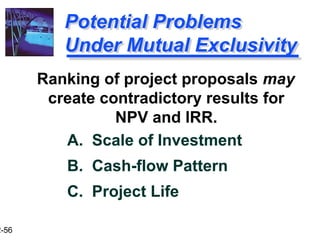

Potential Problems

Under MutualExclusivity

A. Scale of Investment

B. Cash-flow Pattern

C. Project Life

Ranking of project proposals may

create contradictory results for

NPV and IRR.

57.

2-57

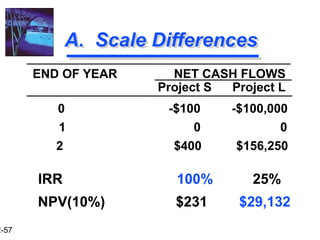

A. Scale Differences

NETCASH FLOWS

Project S Project L

END OF YEAR

0 -$100 -$100,000

1 0 0

2 $400 $156,250

IRR 100% 25%

NPV(10%) $231 $29,132

58.

2-58

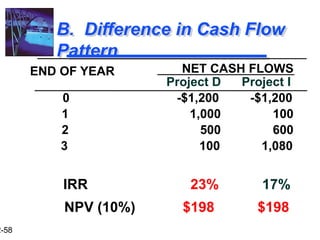

B. Difference inCash Flow

Pattern

NET CASH FLOWS

Project D Project I

END OF YEAR

0 -$1,200 -$1,200

1 1,000 100

2 500 600

3 100 1,080

IRR 23% 17%

NPV (10%) $198 $198

59.

2-59

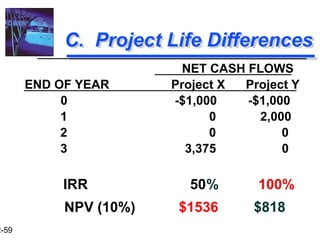

C. Project LifeDifferences

NET CASH FLOWS

Project X Project Y

END OF YEAR

0 -$1,000 -$1,000

1 0 2,000

2 0 0

3 3,375 0

IRR 50% 100%

NPV (10%) $1536 $818

60.

2-60

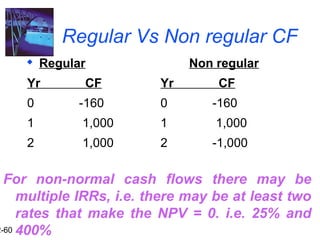

Regular Vs Nonregular CF

Regular

Yr CF

0 -160

1 1,000

2 1,000

Non regular

Yr CF

0 -160

1 1,000

2 -1,000

For non-normal cash flows there may be

multiple IRRs, i.e. there may be at least two

rates that make the NPV = 0. i.e. 25% and

400%

61.

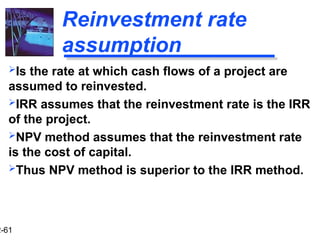

2-61

Reinvestment rate

assumption

Is therate at which cash flows of a project are

assumed to reinvested.

IRR assumes that the reinvestment rate is the IRR

of the project.

NPV method assumes that the reinvestment rate

is the cost of capital.

Thus NPV method is superior to the IRR method.

62.

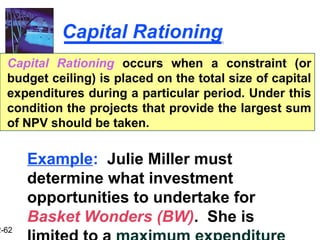

2-62

Capital Rationing

Capital Rationingoccurs when a constraint (or

budget ceiling) is placed on the total size of capital

expenditures during a particular period. Under this

condition the projects that provide the largest sum

of NPV should be taken.

Example: Julie Miller must

determine what investment

opportunities to undertake for

Basket Wonders (BW). She is

63.

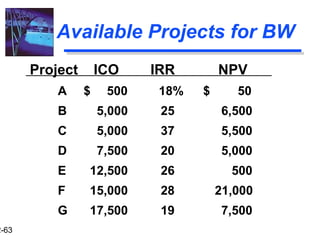

2-63

Available Projects forBW

Project ICO IRR NPV

A $ 500 18% $ 50

B 5,000 25 6,500

C 5,000 37 5,500

D 7,500 20 5,000

E 12,500 26 500

F 15,000 28 21,000

G 17,500 19 7,500

![2-36

PBP Acceptance Criterion

Yes! The firm will receive back the

initial cash outlay in less than 3.5

years. [3.3 Years < 3.5 Year Max.]

The management of Basket Wonders

has set a maximum PBP of 3.5

years for projects of this type.

Should this project be accepted?](https://image.slidesharecdn.com/ch4capitalbudgeting1-250903053140-311b3770/85/Chapter4_Introduction-to-capital_budgeting-1-pptx-36-320.jpg)

![2-43

NPV Acceptance Criterion

No! The NPV is negative. This means

that the project is reducing shareholder

wealth. [Reject as NPV < 0 ]

The management of Basket Wonders

has determined that the required

rate is 13% for projects of this type.

Should this project be accepted?](https://image.slidesharecdn.com/ch4capitalbudgeting1-250903053140-311b3770/85/Chapter4_Introduction-to-capital_budgeting-1-pptx-43-320.jpg)

![2-52

Profitability Index (PI)

PI is the ratio of the present value of

a project’s future net cash flows to

the project’s initial investment.

CF1 CF2 CFn

(1+k)1

(1+k)2

(1+k)n

+ . . . +

+ IInVT

PI =

PI = 1 + [ NPV / IINVT ]

<< OR >>

Method #2:

Method #1:](https://image.slidesharecdn.com/ch4capitalbudgeting1-250903053140-311b3770/85/Chapter4_Introduction-to-capital_budgeting-1-pptx-52-320.jpg)