LEARNING OBJECTIVES

Understand natureof a limited company

Advantages and disdavantages of a limited company

Income statement of a limited company

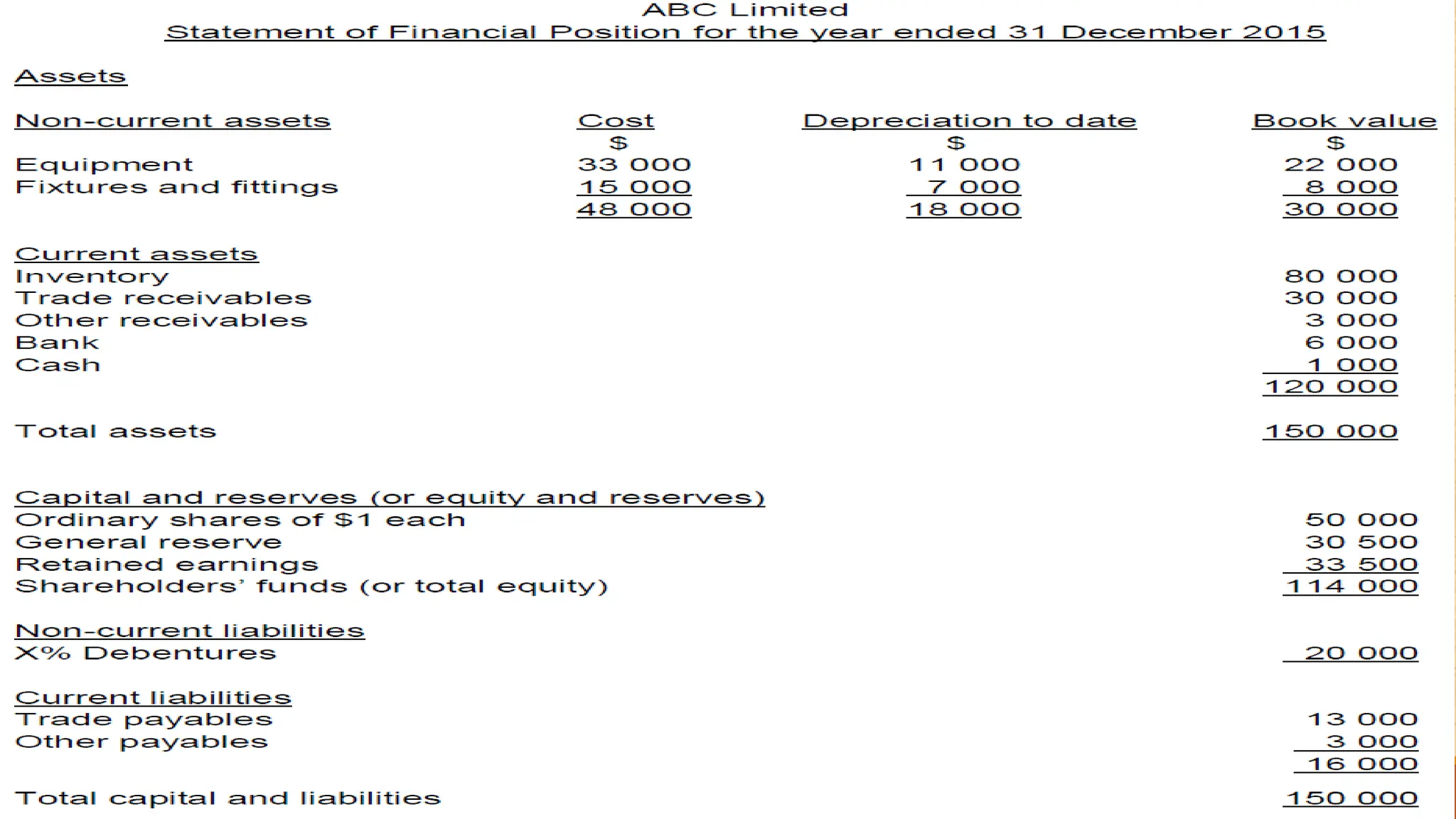

Statement of Financial Position of a limited company

Statement of Changes in Equity

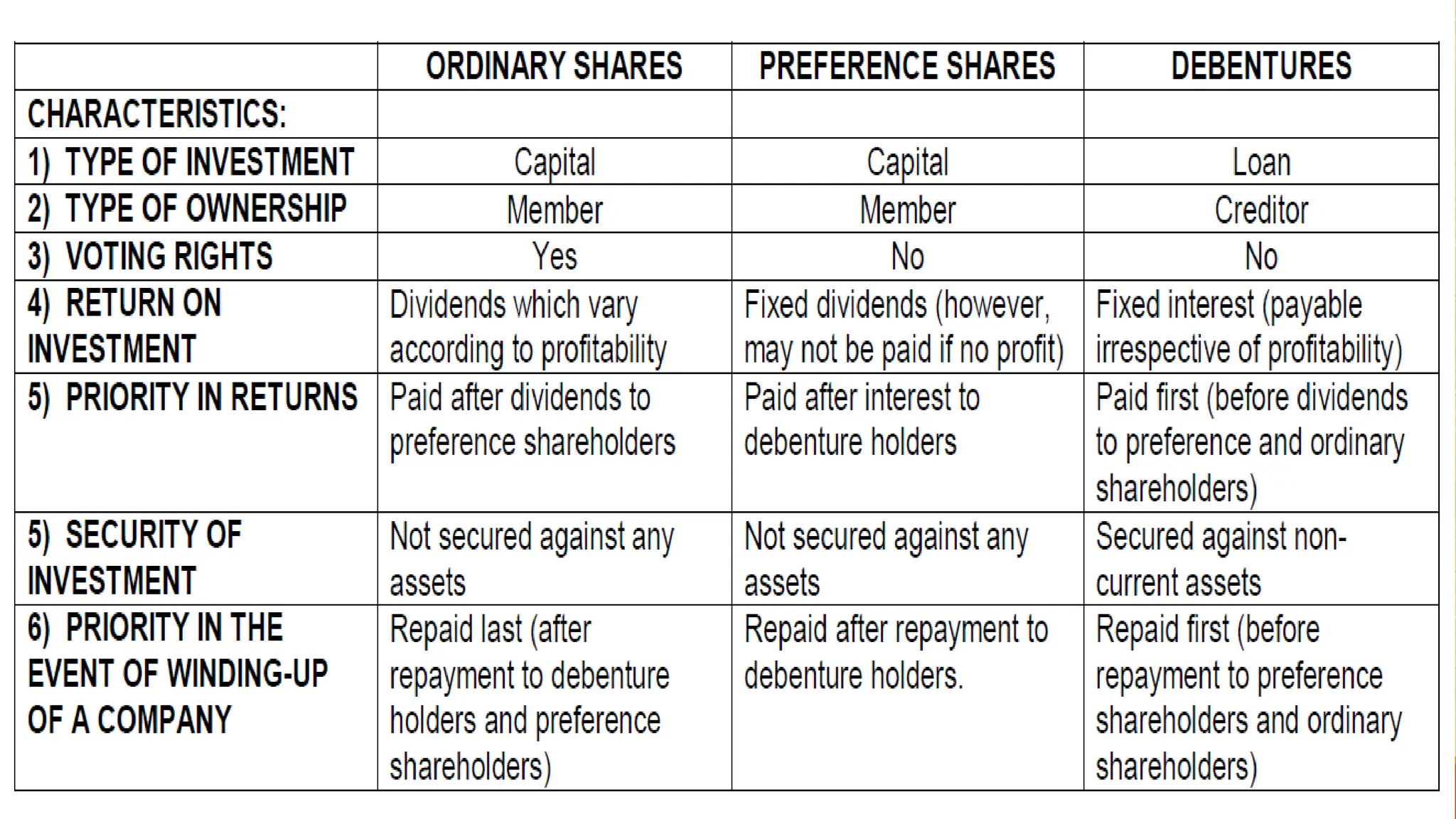

Types of shares

Dividends

General reserves

Debentures

Comparison of ordinary shares, preference shares and debentures

Capital requirements of a limited company

2

3.

WHAT IS ALIMITED COMPANY ?

3

A company or business which is limited in its’ liability.

Limited liability

An owner’s or shareholder’s liability is limited to the amount of

his/her investment in the company. A shareholder will not be

liable for the company’s debts except for his/her unpaid

investment in the company.

4.

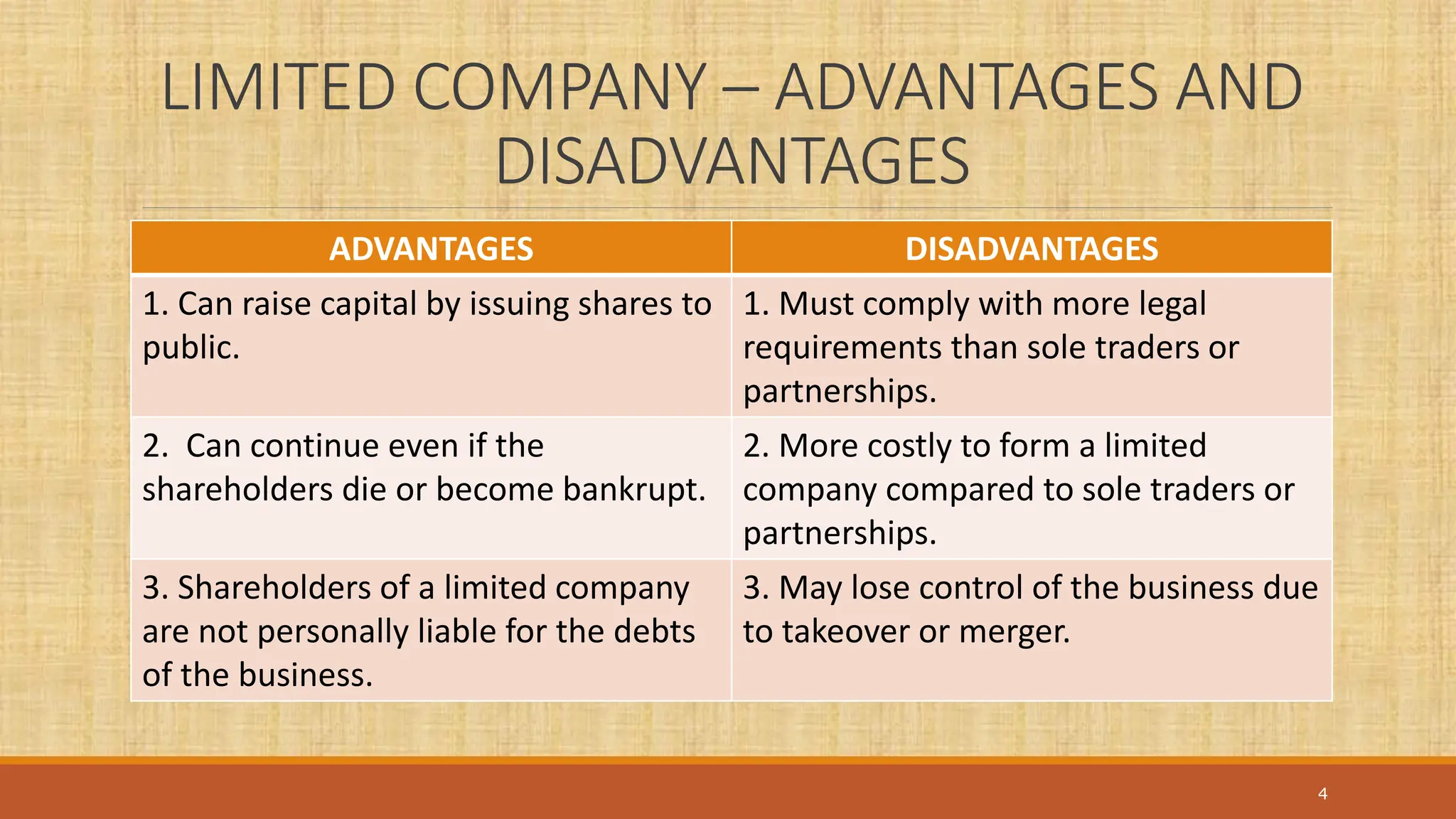

LIMITED COMPANY –ADVANTAGES AND

DISADVANTAGES

ADVANTAGES DISADVANTAGES

1. Can raise capital by issuing shares to

public.

1. Must comply with more legal

requirements than sole traders or

partnerships.

2. Can continue even if the

shareholders die or become bankrupt.

2. More costly to form a limited

company compared to sole traders or

partnerships.

3. Shareholders of a limited company

are not personally liable for the debts

of the business.

3. May lose control of the business due

to takeover or merger.

4

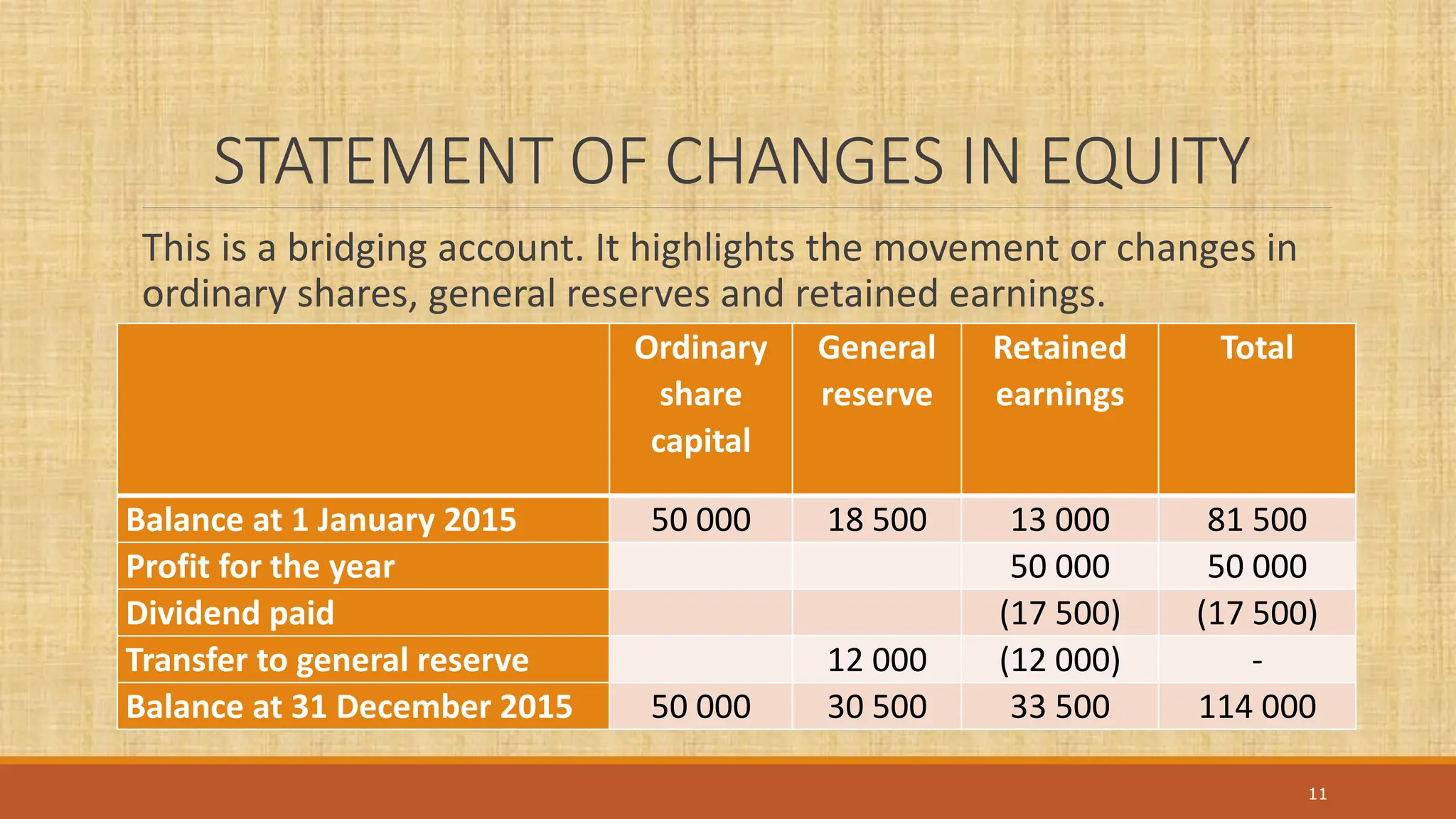

STATEMENT OF CHANGESIN EQUITY

This is a bridging account. It highlights the movement or changes in

ordinary shares, general reserves and retained earnings.

11

Ordinary

share

capital

General

reserve

Retained

earnings

Total

Balance at 1 January 2015 50 000 18 500 13 000 81 500

Profit for the year 50 000 50 000

Dividend paid (17 500) (17 500)

Transfer to general reserve 12 000 (12 000) -

Balance at 31 December 2015 50 000 30 500 33 500 114 000

12.

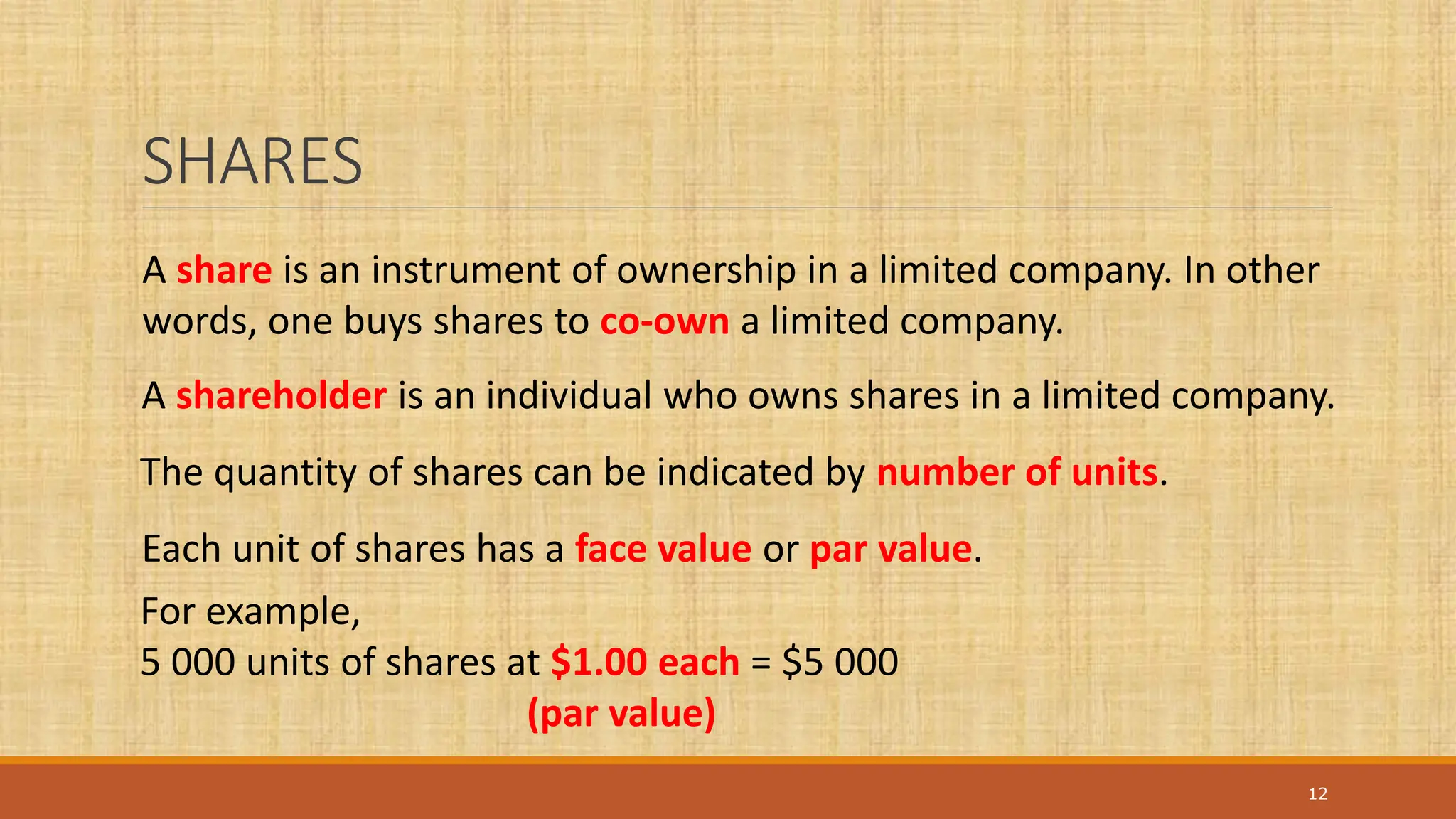

SHARES

12

A share isan instrument of ownership in a limited company. In other

words, one buys shares to co-own a limited company.

A shareholder is an individual who owns shares in a limited company.

The quantity of shares can be indicated by number of units.

Each unit of shares has a face value or par value.

For example,

5 000 units of shares at $1.00 each = $5 000

(par value)

13.

TYPES OF SHARES

13

1.Ordinary Shares

Ownership of a limited company which entitles the

shareholder to vote in the Annual General Meeting (AGM)

according to percentage of his/her shareholdings.

Example,

Marianne bought 50 000 ordinary shares of $0.50 each

= $25 000.

Total value of ordinary shares = $250 000

Therefore, Marianne’s voting right = 10%.

14.

14

2. X% PreferenceShares

Ownership of a limited company which entitles the

shareholder to receive a fixed dividend, (rate of dividend

indicated as a “%” before the term “preference shares”, for

example, 10% preference shares). This dividend is payable

first to the preference shareholders before any dividends

to the ordinary shareholders.

Example:

Albright bought 10 000 6% preference shares of $1.00 each.

Albright will receive a yearly dividend of = 10 000 x $1.00 x 6%

= $600.

15.

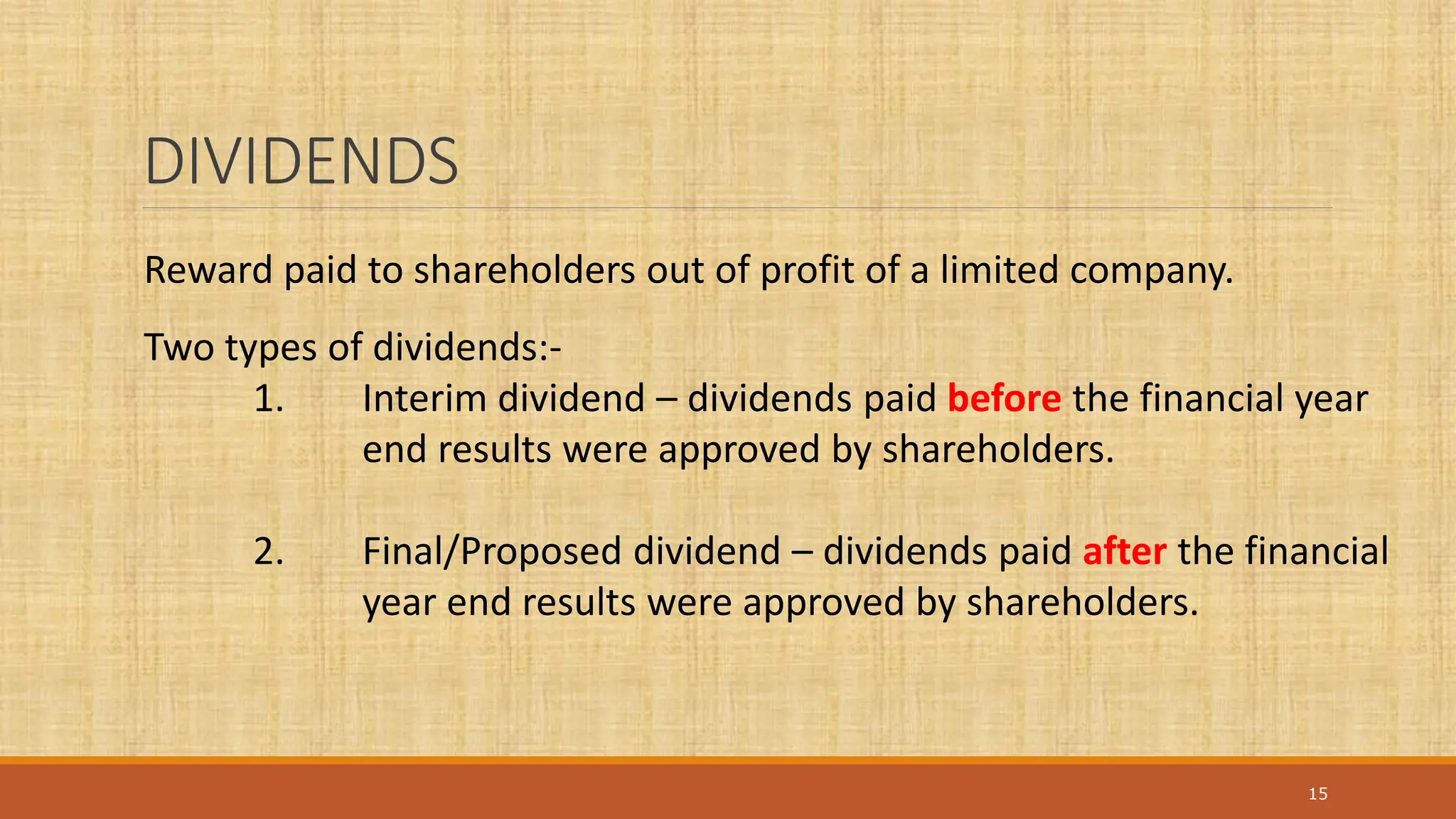

DIVIDENDS

15

Reward paid toshareholders out of profit of a limited company.

Two types of dividends:-

1. Interim dividend – dividends paid before the financial year

end results were approved by shareholders.

2. Final/Proposed dividend – dividends paid after the financial

year end results were approved by shareholders.

16.

CALCULATION OF DIVIDENDS

16

Dividendscan be calculated in the following ways:

1. As a percentage of share capital.

Example: A company has 800 000 ordinary shares of $1.00 each.

The directors have announced an ordinary share dividend of

10%.

Ordinary share dividend is 10% x 800 000 x $1.00 = $80 000.

17.

17

2. As anamount per share

Example: A company’s ordinary share capital consists of 900 000

shares at $0.50 each. The directors have announced a dividend

of $0.05 per share.

Ordinary share dividend is 900 000 x $0.05 = $45 000.

18.

GENERAL RESERVES

Part ofprofit which have not been distributed as dividends and set

aside for future uses. For example, it may be used to pay future

dividends if retained earnings are low or finance the capital

expansion of the business.

18

19.

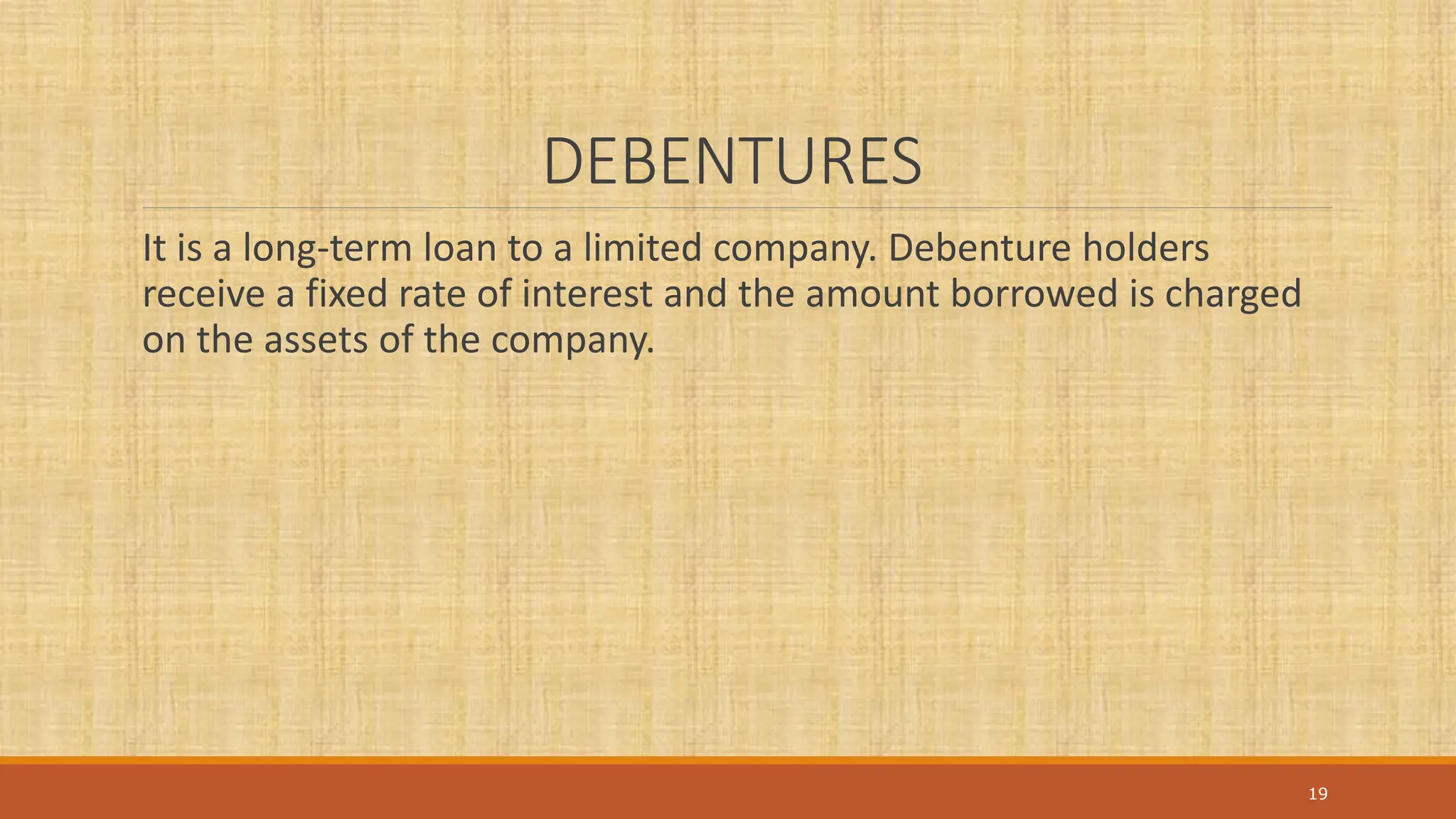

DEBENTURES

It is along-term loan to a limited company. Debenture holders

receive a fixed rate of interest and the amount borrowed is charged

on the assets of the company.

19

CAPITAL REQUIREMENT

22

The capitalrequirement of a limited company can be broken down into

different stages:-

Authorised Capital

Issued Capital

Called-up Capital

Paid-up Capital

23.

23

• Maximum numberof shares that could be issued by a

limited company.

Authorised Capital

• Number of shares issued by a limited company.

Issued Capital

• Requirement for shareholders to pay part of the

issued shared capital.

• Investors may pay in instalments, hence 1st call, 2nd

call, and final call.

Called-up Capital

• Part of called-up capital for which payment has been

received.

Paid-up Capital

24.

REFLECTION

What is thedifference between preference and ordinary shares ?

What is a debenture ?

Understand how to prepare the statement of changes in equity.

Understand the statement of financial postion of a limited company.

24