15-3

What is aPartnership?

An association of two or

more persons who

are co-owners of a

business, and

share profits and losses

in an agreed-upon

manner. ABC

Company

A B

4.

15-4

What is a“Person”?

An individual

A corporation

Another partnership

Z Corp

T&D

Partnership

5.

15-5

Partnerships: Pros &Cons

Advantages

Ease of formation

Lack of formality

Single taxation (see following slide)

Disadvantages

Unlimited liability (for general partnerships)

Difficulty in disposing of partnership interests

Mutual agency

6.

15-6

Partnership Form ofOrganization: Income Tax

Reporting

Single Taxation of Partnership

Earnings

Partnerships only report their

earnings—they are not taxed at the

business entity level (as are

corporations).

Partnerships file IRS Form 1065,

which shows the allocation of profits

among partners.

Partners report their share of profits

on their individual IRS Form 1040

return.

AB

Partnership

A B

Uncle Sam

7.

15-7

Regulation

Each stateregulates the partnerships

that are formed in it.

Most states begin with a model act and

then modifies it to fit that state’s

business culture and history.

Most have now adopted the Uniform

Partnership Act of 1997 (UPA 1997) as

their model act.

8.

15-8

Regulation: The UniformPartnership Act (UPA)

The UPA 1997 covers:

Relations of partners to one another.

Relations of partners to persons dealing

with the partnership.

Dissolution and winding up of the

partnership.

9.

15-9

The Partnership Agreement

What is a partnership agreement?

A written expression of what the

partners have agreed to.

Examples of areas addressed:

Manner of sharing profits.

Limitations on withdrawals.

Rights of partners.

Settling with withdrawing partners.

Expulsion of partners.

Conflicts of interest.

10.

15-10

Practice Quiz Question#1

Which of the following is not one of

the advantages of general

partnerships?

a. Ease of formation

b. Unlimited liability

c. Lack of formality

d. Single taxation

11.

15-11

Practice Quiz Question#1 Solution

Which of the following is not one of

the advantages of general

partnerships?

a. Ease of formation

b. Unlimited liability

c. Lack of formality

d. Single taxation

15-13

Types of Partnerships

General Partnerships

All partners have unlimited liability.

Creditors can go after the personal assets of

any or all of the partners.

14.

15-14

Types of Partnerships

Limited Partnerships

Limited partners have limited liability to

partnership creditors if the partnership is unable

to pay its debts.

Limited partners’ risk is limited to their invested

capital.

Thus, personal assets are not at risk.

At least one of the partners must be a general

partner.

15.

15-15

Types of Partnerships

Limited Liability Partnerships (LLPs)

A partner’s personal assets are at risk only for

his or her own negligence and wrongdoing,

the negligence and wrongdoing of those under his or

her control, but

not debts.

Since 1993, many accounting firms have changed

from general partnerships to LLPs.

16.

15-16

Types of Partnerships

Limited Liability Limited Partnerships

(LLLPs)

Like a limited partnership, must have at least one

general partner.

General partners manage the partnership.

Big difference relates to the liability of general

partners:

No personal liability for partnership obligations (like a

limited partner)

Not liable for wrongdoing of other partners—just

personal decisions and decisions of those supervised

17.

15-17

Practice Quiz Question#2

Which of the following statements is true?

a. The partners in a general partnership

have limited liability.

b. At least two of the partners in a limited

partnership must be general partners.

c. Partners in an LLP are not responsible

for their own actions.

d. Limited liability limited partnerships

must have at least one general partner.

18.

15-18

Practice Quiz Question#2 Solution

Which of the following statements is true?

a. The partners in a general partnership

have limited liability.

b. At least two of the partners in a limited

partnership must be general partners.

c. Partners in an LLP are not responsible

for their own actions.

d. Limited liability limited partnerships

must have at least one general partner.

15-20

Partners’ Accounts

Eachpartner can have

a capital account.

a drawing account (a contra capital

account—closed out at year-end).

a loan account (loans usually earn

interest—a partnership expense).

Partnerships do NOT use a

retained earnings account. DR CR

21.

15-21

Recording Capital Contributions

Keep it FAIR!

Current Fair Market

Values should be used to

record

noncash assets contributed

to a partnership.

liabilities assumed by a

partnership. ABC

Partnership

22.

15-22

$150,000 + $175,000= $325,000

Partnership Formation Example

Brian and Spencer wish to form the B&S partnership.

Brian contributes land with a book value of $65,000

and a current value of $150,000 and a building with a

book value of $142,000 and a current value of

$175,000. Spencer will contribute cash.

If the partners plan to share profits and losses equally

after the formation of the partnership and assuming

they have agreed to equal capital contributions, how

much cash will Spencer have to contribute to form the

partnership?

23.

15-23

Comprehensive Partnership CreationProblem

The partnerships of Brad & Mike (B&M) and Austin

and Justin (A&J) began business on 1/1/X1; each

partnership owns one retail appliance store. The two

partnerships agree to combine as of 7/1/X8 to form a

new partnership, BAM-J Discount Stores.

REQUIRED

Given the information on the next two slides,

1. Prepare the journal entries to record the initial capital

contribution after considering the effect of this information.

Use separate entries for each of the combining partnerships.

2. Prepare a schedule computing the cash contributed or

withdrawn by each partner to bring the initial capital balances

into the profit and loss sharing ratio.

24.

15-24

Comprehensive Partnership CreationProblem

1. Profit and loss ratios. The profit and loss sharing ratios for the former partnerships were

40% to Brad and 60% to Mike, and 30% to Austin and 70% to Justin. The profit and loss

sharing ratio for the new partnership is Brad, 20%; Mike, 30%; Austin, 15%; and Justin, 35%.

2. Capital investments. The opening capital investments for the new partnership are to be in

the same ratio as the profit and loss sharing ratios for the new partnership. If necessary,

certain partners may have to contribute additional cash, and others may have to withdraw

cash to bring the capital investments into the proper ratio.

3. Accounts receivable. The partners agreed to set the new partnership’s allowance for bad

debts at 3% of the accounts receivable contributed by B&M and 12% of the accounts

receivable contributed by A&J.

4. Inventory. The new partnership’s opening inventory is to be valued by the FIFO method.

B&M used the FIFO method to value inventory (which approximates its current value), and

A&J used the LIFO method. The LIFO inventory represents 85% of its FIFO value.

5. Property and equipment. The partners agree that the building’s current value is

approximately 70% of the building’s historical cost, as recorded on each partnership’s books.

6. Unpaid liability. After each partnership’s books were closed on 6/30/X8, an unrecorded

merchandise purchase of $1,500 by A&J was discovered. The merchandise had been sold by

6/30/X8.

7. The 6/30/X8 post-closing trial balances of the partnerships follow.

25.

15-25

Comprehensive Partnership CreationProblem

Account

Brad & Mike Trial

Balance – June 30, 20X8

Austin & Justin Trial

Balance – June 30, 20X8

Cash 25,000 22,000

Accounts Receivable 100,000 150,000

Allowance for doubtful accounts 2,000 6,000

Inventory 175,000 119,000

Building & Equipment 105,000 160,000

Accumulated Depreciation 24,000 61,000

Accounts Payable 40,000 60,000

Notes Payable 100,000 120,000

Brad, Capital 95,000

Mike, Capital 144,000

Austin, Capital 65,000

Justin, Capital 139,000

Totals 405,000 405,000 451,000 451,000

1. Prepare the journal entries to record the initial capital contribution after considering the

effect of this information. Use separate entries for each of the combining partnerships.

2. Prepare a schedule computing the cash contributed or withdrawn by each partner to

bring the initial capital balances into the profit and los sharing ratio.

26.

15-26

Comprehensive Problem Solution

PART1

Summary of changes to carrying values:

Brad & Mike Austin & Justin

Increase allowance for bad debt $(1,000) $(12,000)

Increase inventory 21,000)

Increase buildings and equipment (7,500) 13,000)

Increase accounts payable (1,500)

Net increase $(8,500) $20,500)

Brad (40%) $(3,400) Austin (30%) $6,150

Mike (60%) (5,100) Justin (70%) 14,350

$(8,500) $20,500

Allocate to:

27.

15-27

Cash 25,000

Accounts Receivable100,000

Allowance for doubtful accounts 3,000

Inventory 75,000

Building & Equipment 73,500

Accounts Payable 40,000

Notes Payable 100,000

Brad, Capital 91,600

Mike, Capital 138,900

Comprehensive Problem Solution

Brad & Mike Journal Entry:

28.

15-28

Comprehensive Problem Solution

Austin& Justin Journal Entry:

Cash 22,000

Accounts Receivable 150,000

Allowance for doubtful accounts 18,000

Inventory 140,000

Building & Equipment 112,000

Accounts Payable 61,500

Notes Payable 120,000

Austin, Capital 71,150

Justin, Capital 153,350

29.

15-29

Comprehensive Problem Solution

PART2

Brad Mike Austin Justin Total

Profit sharing percentage 20% 30% 15% 35%

Capital balances 91,600 138,900 71,150 153,350 455,000

Capital balances required

using profit and loss

sharing percentages

91,000 136,500 68,250 159,250

Capital contribution or

(withdrawal)

(600) (2,400) (2,900) 5,900

15-31

Accounting for Operationsof a Partnership

Partners’ accounts

Capital accounts

Used to record the initial investment of a partner, any

subsequent capital contributions, profit or loss

distributions, and any withdrawals of capital by the

partner

Deficiencies are usually eliminated by additional

capital contributions

Capital

Investment

Contributions

% Profit

% Loss

Drawings

32.

15-32

Accounting for Operationsof a Partnership

Partners’ accounts

Drawing accounts

Used to record periodic withdrawals and is then

closed to the partner’s capital account at the end of

the period

Noncash drawings are valued at their market values

at the date of the withdrawal

Loan accounts

A loan from a partner is shown as a payable on the

partnership’s books

Unless all partners agree otherwise, the partnership

is obligated to pay interest on the loan

33.

15-33

Practice Quiz Question#3

Which of the following would result in

a reduction to a partner’s capital

account?

a. The initial investment.

b. The allocation of a profit.

c. Additional capital contributions.

d. A withdrawal.

e. A loan to a partner.

34.

15-34

Practice Quiz Question#3 Solution

Which of the following would result in

a reduction to a partner’s capital

account?

a. The initial investment.

b. The allocation of a profit.

c. Additional capital contributions.

d. A withdrawal.

e. A loan to a partner.

15-36

Profit & LossSummary 162,000

Capital, Brian 81,000

Capital, Spencer 81,000

Income Allocation Example

Assume that in its first year of operation, B&S

partnership earns $162,000 of income.

What journal entry would B&S make to allocate

the profits between the two partners?

37.

15-37

Sharing Profits andLosses

Partners can share profits and losses in

any way they choose.

Possible ways include

ratios

salary allowances and ratios

imputed interest on capital, salary

allowances, and ratios

capital balances only

performance methods

38.

15-38

REQUIRED

1. Prepare aschedule showing how the profit would be divided,

assuming the partnership profit or loss is:

a. $ 102,000

b. $ 57,000

c. $(34,000)

2. What journal entry should be made to allocate the profit or loss

for each of the three cases listed above?

Group Exercise 1: Allocating Profit and Loss,

No Restrictions

The partnership of Alex and James has the following provisions:

• Alex and James receive salary allowances of $37,000 and $18,000,

respectively.

• Interest is imputed at 10% on the average capital investment.

• Any remaining profit or loss is shared between Alex and James in

a 3:2 ratio, respectively.

• Average Capital investments: Alex, $ 50,000; James, 130,000

39.

15-39

ALLOCATED TO

Alex JamesTotal

Total Profit 102,000)

Salary

Interest on Capital

Residual Profit

Allocate Profit

Group Exercise 1: Solution for part a

37,000 18,000 (55,000)

5,000 13,000 (18,000)

29,000

17,400 11,600 (29,000)

59,400 42,600 0

Income Summary 102,000

Capital, Alex 59,400

Capital, James 42,600

40.

15-40

REQUIRED

1. Prepare aschedule showing how the profit would be divided,

assuming the partnership profit or loss is:

a. $ 102,000

b. $ 57,000

c. $(34,000)

2. What journal entry should be made to allocate the profit or loss

for each of the three cases listed above?

Group Exercise 1: Allocating Profit and Loss,

No Restrictions

The partnership of Alex and James has the following provisions:

• Alex and James receive salary allowances of $37,000 and $18,000,

respectively.

• Interest is imputed at 10% on the average capital investment.

• Any remaining profit or loss is shared between Alex and James in

a 3:2 ratio, respectively.

• Average Capital investments: Alex, $ 50,000; James, 130,000

41.

15-41

Income Summary 57,000

Capital,Alex 32,400

Capital, James 24,600

ALLOCATED TO

Alex James Total

Total Profit 57,000)

Salary 37,000) 18,000) (55,000)

Interest on Capital 5,000) 13,000) (18,000)

Residual Profit (16,000)

Allocate Profit (9,600) (6,400) 16,000)

32,400) 24,600) 0)

Group Exercise 1: Solution for part b

42.

15-42

REQUIRED

1. Prepare aschedule showing how the profit would be divided,

assuming the partnership profit or loss is:

a. $ 102,000

b. $ 57,000

c. $(34,000)

2. What journal entry should be made to allocate the profit or loss

for each of the three cases listed above?

Group Exercise 1: Allocating Profit and Loss,

No Restrictions

The partnership of Alex and James has the following provisions:

• Alex and James receive salary allowances of $37,000 and $18,000,

respectively.

• Interest is imputed at 10% on the average capital investment.

• Any remaining profit or loss is shared between Alex and James in

a 3:2 ratio, respectively.

• Average Capital investments: Alex, $ 50,000; James, 130,000

43.

15-43

Capital, Alex 22,200

Capital,James 11,800

Income Summary 34,000

ALLOCATED TO

Alex James Total

Total Profit (34,000)

Salary 37,000) 18,000) (55,000)

Interest on Capital 5,000) 13,000) (18,000)

Residual Profit (107,000)

Allocate Profit (64,200) (42,800) 107,000)

(22,200) (11,800) 0)

Group Exercise 1: Solution for part c

44.

15-44

Methods to ShareProfits and Losses: “To the

Extent Possible” Limitations

When a “limit” provision exists:

The next lower level method of sharing can be

reached if and only if there is still unallocated

profit remaining after dealing with the current

level.

45.

15-45

Group Exercise 2:Allocating Profit and Loss—

“Limit”

Assume the same information provided in Group Exercise 1,

except that the partnership agreement stipulates the following

order of priority:

1. Salary allowances (only to the extent available)

2. Imputed interest on average capital investments (only to

the extent available).

3. Any remaining profit in a 3:2 ratio. (No mention is made

regarding losses.)

REQUIRED:

The requirements are the same as for Group Exercise 1 (i.e.,

calculate the allocations and prepare journal entries).

a. $ 102,000

b. $ 57,000

c. $ (34,000)

46.

15-46

Income Summary 102,000

Capital,Alex 59,400

Capital, James 42,600

ALLOCATED TO

Alex James Total

Total Profit 102,000)

Salary 37,000) 18,000) (55,000)

Interest on Capital 5,000) 13,000) (18,000)

Residual Profit 29,000)

Allocate Profit 17,400) 11,600) (29,000)

59,400) 42,600) 0)

Group Exercise 2: Solution for part a

47.

15-47

Group Exercise 2:Allocating Profit and Loss—

“Limit”

Assume the same information provided in Group Exercise 1,

except that the partnership agreement stipulates the following

order of priority:

1. Salary allowances (only to the extent available)

2. Imputed interest on average capital investments (only to

the extent available).

3. Any remaining profit in a 3:2 ratio. (No mention is made

regarding losses.)

REQUIRED:

The requirements are the same as for Group Exercise 1 (i.e.,

calculate the allocations and prepare journal entries).

a. $ 102,000

b. $ 57,000

c. $ (34,000)

48.

15-48

Income Summary 57,000

Capital,Alex 37,556

Capital, James 19,444

ALLOCATED TO

Alex James Total

Total Profit 57,000)

Salary 37,000) 18,000) (55,000)

2,000)

Interest on Capital * 556) 1,444) (2,000)

Residual Profit 0)

Allocate Profit 0) 0) 0)

37,556) 19,444) 0)

Group Exercise 2: Solution for part b

* $2,000 x (5,000 ÷ $18,000) = 556

$2,000 x ($13,000 ÷ $18,000) = 1,444

49.

15-49

Group Exercise 2:Solution for part c

In this case, the partnership agreement is

vague. An argument can be made for allocating

the loss equally pursuant the UPA 1997 because

the partnership agreement is silent with respect

to losses.

Alternatively, we could presume that losses were

intended to be shared in the residual profit-

sharing ratio.

In these cases, the accountant should seek

clarification from each partner.

50.

15-50

Practice Quiz Question#4

Matt and Chad created a partnership (M&C)

on 12/31/X8 (sharing profits 50/50). Matt

contributed equipment from his sole

proprietorship having a carrying value of

$4,000 and a fair value of $8,000. In 20X9,

M&C had profits of $96,000 and borrowed

$20,000 from a bank. In 2009, Matt withdrew

$35,000 cash. Matt’s Y/E capital balance is

a. $11,000.

b. $17,000.

c. $21,000.

d. $56,000.

51.

15-51

Practice Quiz Question#4 Solution

Matt and Chad created a partnership (M&C)

on 12/31/X8 (sharing profits 50/50). Matt

contributed equipment from his sole

proprietorship having a carrying value of

$4,000 and a fair value of $8,000. In 20X9,

M&C had profits of $96,000 and borrowed

$20,000 from a bank. In 2009, Matt withdrew

$35,000 cash. Matt’s Y/E capital balance is

a. $11,000.

b. $17,000.

c. $21,000 ($8,000 + $96,000/2 - $35,000)

d. $56,000.

15-53

Partner’s Admission: Purchaseof An Existing

Interest

The purchase of an interest from

one or more of a partnership’s

existing partners is a:

personal transaction between the

incoming partner and the selling

partner(s).

The only entry required on the

partnership’s books is to transfer

an amount:

from the selling partner’s Capital

account.

to the new partner’s Capital account.

C

Interest $

AB

Partnership

A B

54.

15-54

Partner’s Admission: Addinga New Partner

Key Objective

Achieve equity among the partners

AB

Partnership

A B

+

C

Assets

= ABC

Partnership

A B C

55.

15-55

How to AchieveEquity?

Example

AB

Partnership

A B

+

C

Assets

= ABC

Partnership

A B C

How much would C have to contribute?

What factors would you have to consider?

Cash $100,000 Capital, A $100,000

Land 100,000 Capital, B 100,000

Total Assets $200,000 Total Equity $200,000

56.

15-56

How to AchieveEquity?

Example

Q: What if the land has a current value of $200,000?

Assume C contributes $150,000 (FMV of value

owned by A and B) for a 1/3 interest in assets,

profits, and losses.

Q: What if the land is sold the next day for $200,000?

Cash $100,000 Capital, A $100,000

Land 100,000 Capital, B 100,000

Total Assets $200,000 Total Equity $200,000

57.

15-57

Minimizing Inequities

TheThree Methods

The revaluing of assets / goodwill method

The bonus method

The special profit-and-loss sharing

provision method

Some methods can still result in

inequities if events do not materialize as

assumed.

≠

58.

15-58

Minimizing Inequities

TheThree Methods

The revaluing of assets / goodwill method

The bonus method

The special profit-and-loss sharing

provision method

Some methods can still result in

inequities if events do not materialize as

assumed.

≠

59.

15-59

(1) Revaluing ofAssets Method

Q: What if the land has a current value of $200,000?

A: Simply “revalue” the land before admitting C!

Q: How do you record C’s contribution?

Q: What if the land is sold two years later for $230,000?

A: Each gets $10,000 of gain.

Cash $100,000 Capital, A $150,000

Land 200,000 Capital, B 150,000

Total Assets $300,000 Total Equity $300,000

Land 100,000

Capital, A 50,000

Capital, B 50,000

Cash 150,000

Capital, C 150,000

60.

15-60

Q: Given thatthe land has a current value of $200,000?

(2) Bonus Method

The partners agree to share equally in all future gains or

losses on the disposal of the land. However, C’s capital

account is decreased up front by the amount of the first

$100,000 of gain that he/she will receive ($33,333). This

decrease is added to A’s and B’s capital accounts up front.

Cash 150,000

Capital, A 16,667

Capital, B 16,667

Capital, C 116,667

Q: What if the land is sold two years later for $230,000?

A: Each gets $43,333 of gain.

61.

15-61

(3) Special Profitand Loss Sharing Provision

Q: Given that the land has a current value of $200,000?

Q: What if the land is sold two years later for $230,000?

A: A and B share equally in the first $100,000 of gain and all

partners share equally in the additional $30,000 of gain.

A and B each get $60,000 and C gets $10,000 of the gain.

Cash 150,000

Capital, C 150,000

Specify in the new partnership agreement that the land’s

current value is $200,000 and that partners A and B share

equally (or in some other specified manner) in the first

$100,000 of gain when the land is disposed of.

62.

15-62

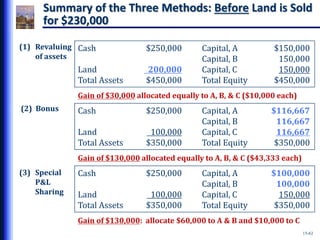

Cash $250,000 Capital,A $150,000

Capital, B 150,000

Land 200,000 Capital, C 150,000

Total Assets $450,000 Total Equity $450,000

Cash $250,000 Capital, A $100,000

Capital, B 100,000

Land 100,000 Capital, C 150,000

Total Assets $350,000 Total Equity $350,000

Cash $250,000 Capital, A $116,667

Capital, B 116,667

Land 100,000 Capital, C 116,667

Total Assets $350,000 Total Equity $350,000

(1) Revaluing

of assets

(3) Special

P&L

Sharing

(2) Bonus

Gain of $30,000 allocated equally to A, B, & C ($10,000 each)

Gain of $130,000: allocate $60,000 to A & B and $10,000 to C

Gain of $130,000 allocated equally to A, B, & C ($43,333 each)

Summary of the Three Methods: Before Land is Sold

for $230,000

63.

15-63

Cash $480,000 Capital,A $160,000

Capital, B 160,000

Capital, C 160,000

Total Assets $480,000 Total Equity $480,000

Cash $480,000 Capital, A $160,000

Capital, B 160,000

Capital, C 160,000

Total Assets $480,000 Total Equity $480,000

Cash $480,000 Capital, A $160,000

Capital, B 160,000

Capital, C 160,000

Total Assets $480,000 Total Equity $480,000

(1) Revaluing

of assets

(3) Special

P&L

Sharing

(2) Bonus

We get the same result under each method!

Summary of the Three Methods: After Land is Sold

for $230,000

64.

15-64

Minimizing Inequities

Onlythe special profit-and loss sharing

provision method will prevent an

inequity to one or more of the partners in

the event that

the agreed-upon values of the assets are

erroneous.

the agreed-upon value of goodwill does not

materialize.

≠

65.

15-65

Key Differences BetweenRevaluation /

Goodwill and Bonus Methods

Revaluation/Goodwill Method

Revalue the balance sheet by

recording goodwill or revaluing

existing assets.

Thus, we now have a bigger “pie”

to divide up among the partners.

Land 100,000

Capital, A 50,000

Capital, B 50,000

Excess Value

Book Value

of Net Assets

66.

15-66

Key Differences BetweenRevaluation /

Goodwill and Bonus Methods

Revaluation/Goodwill Method

Revalue the balance sheet by

recording goodwill or revaluing

existing assets.

Thus, we now have a bigger “pie”

to divide up among the partners.

The new partner’s capital account

will be equal to his/her ownership

percentage of the “Big Pie.”

Cash 150,000

Capital, C 150,000

Land = $100,000

Small Pie =

200,000 +

150,000 =

350,000

x 1/3 =

$150,000

67.

15-67

Key Differences BetweenRevaluation /

Goodwill and Bonus Methods

Bonus Method

Do not revalue the balance sheet.

Only leaves the book value of net

assets on the balance sheet.

Book Value

of Net Assets

68.

15-68

Key Differences BetweenRevaluation /

Goodwill and Bonus Methods

Bonus Method

Do not revalue the balance sheet.

Only leaves the book value of net

assets on the balance sheet.

The new partner’s capital account

will be equal to his/her ownership

percentage of the “Small Pie.”

Small Pie =

200,000 +

150,000 =

350,000

x 1/3 =

$116,667

Cash 150,000

Capital, A 16,667

Capital, B 16,667

Capital, C 116,667

69.

15-69

The Revaluing ofAssets / Goodwill Method

Advantages

Credit to incoming partner always at least

equal to cash contribution

Can be important “psychologically”

Disadvantages

Departs from GAAP

Complicates income tax preparation

70.

15-70

The Bonus Method

Major Advantages

Does not result in a departure from GAAP

Minimizes bookkeeping and tax return effort

Major Disadvantages

A portion of one or more partner’s capital balance

is transferred to one or more other partners.

The hope is that the transferred amount will later be

recouped via future profits.

Incoming partner’s capital account may be less

than his/her cash contribution!

71.

15-71

Determining the Valueof Goodwill

Steps to follow:

1. Estimate the implied value of the partnership based on

the new partner’s contribution.

New capital contribution ÷ new partner ownership %

2. Estimate the implied value of the partnership based on

the old partners’ total equity.

Total old partner capital balance ÷ total old ownership %

3. Calculate the amount of existing net assets.

The sum of old partner capital and new partner contributed

capital.

4. Calculate implied goodwill

Implied value (greater of 1 or 2) – existing net assets (3)

5. Determine whether the new or old partners possess

goodwill.

The smaller of 1 or 2

The one who paid less for their relative share.

72.

15-72

Practice Quiz Question#5a

Betsy contributes $54,000 cash for a 25% interest

in the new net assets of the partnership (that has

existing equity of $180,000). The old partners

capital accounts are not to decrease (i.e., use the

Revaluation / Goodwill method). Betsy’s capital

account is credited:

a. $ 9,000

b. $54,000

c. $58,500

d. $60,000

e. $76,500

73.

15-73

Solution, Summary

1. Newimplied value: $ 54,000 ÷ 25% = $216,000

2. Old implied value: $180,000 ÷ 75% = $240,000

3. BV of net assets: $180,000 + $54,000 = $234,000

4. Implied Goodwill = $240,000 $234,000 = $ 6,000

5. Goodwill belongs to new partner (because

$216,000 is less than $240,000). [Implies that

she paid less for her relative share of the business.]

Since we’re revaluing, use the BIG pie:

x 25% = $60,000

GW = 6,000

234,000

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

74.

15-74

Practice Quiz Question#5a Solution

Betsy contributes $54,000 cash for a 25% interest

in the new net assets of the partnership (that has

existing equity of $180,000). The old partners

capital accounts are not to decrease (i.e., use the

Revaluation / Goodwill method). Betsy’s capital

account is credited:

a. $ 9,000

b. $54,000

c. $58,500

d. $60,000 ($240,000 x 25%)

e. $76,500

Betsy’s share of the “big pie.”

Cash 54,000

Goodwill 6,000

Capital, Betsy 60,000

75.

15-75

Practice Quiz Question#5b

Betsy contributes $54,000 cash for a 25%

interest in the new net assets of the partnership

(that has existing equity of $180,000). Use the

Bonus Method. Betsy’s capital account is

credited

a. $ 9,000.

b. $54,000.

c. $58,500.

d. $60,000.

e. $76,500.

76.

15-76

Solution, Summary

1. Newimplied value: $ 54,000 ÷ 25% = $216,000

2. Old implied value: $180,000 ÷ 75% = $240,000

3. BV of net assets: $180,000 + $54,000 = $234,000

4. Implied Goodwill = $240,000 $234,000 = $ 6,000

5. Goodwill belongs to new partner (because

$216,000 is less than $240,000). [Implies that

she paid less for her relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

Small Pie

= 180,000

+ 54,000

= 234,000 x 25% = $58,500

Since we’re not

revaluing, use the

Small pie:

77.

15-77

Practice Quiz Question#5b Solution

Betsy contributes $54,000 cash for a 25%

interest in the new net assets of the partnership

(that has existing equity of $180,000). Use the

Bonus Method. Betsy’s capital account is

credited:

a. $ 9,000.

b. $54,000.

c. $58,500.

d. $60,000.

e. $76,500.

Betsy’s share of the “Small Pie.”

Cash 54,000

Capital, Old Part. 4,500

Capital, Betsy 58,500

78.

15-78

Group Exercise: GoodwillMethod

Scott and Stephanie are partners with capital balances

of $100,000 and $65,000, and they share profits and

losses in the ratio of 3:2, respectively. Zoe invests

$60,000 cash for a 25% interest in the capital and

profits of the new partnership. The partners agree that

the implied partnership goodwill is to be recorded

simultaneously with the admission of Zoe.

REQUIRED

1. Calculate the firm’s total implied goodwill.

2. Prepare the entry or entries to record the

admission of Zoe.

79.

15-79

Solution, Summary

1. Newimplied value: $ 60,000 ÷ 25% = $240,000

2. Old implied value: $165,000 ÷ 75% = $220,000

3. BV of net assets: $165,000 + $60,000 = $225,000

4. Implied Goodwill = $240,000 $225,000 = $ 15,000

5. Goodwill belongs to old partners (because

$220,000 is less than $240,000). [Implies that

they “gave” less for their relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

80.

15-80

Note that thisis 25% of the

“Big Pie” because we revalue

the balance sheet!

Group Exercise: Goodwill Method Solution

Entry to record Goodwill

Entry to record Zoe’s cash contribution

Goodwill 15,000

Capital, Scott 9,000

Capital, Stephanie 6,000

Cash 60,000

Capital, Zoe 60,000

x 25% = $60,000

GW = 15,000

165,000 +

60,000 =

225,000

81.

15-81

Group Exercise: BonusMethod

Jim and June are partners who share profits and losses

in the ratio of 2:1, respectively. On 12/31/X8 their

capital accounts are as follows:

Jim $ 40,000

June 30,000

Total $ 70,000

On that date, they agreed to admit Mel as a partner

with a 30% interest in the capital and profits and

losses for an investment of $15,000. The new

partnership will begin with total capital of $85,000.

REQUIRED

Prepare the entry or entries to record the

admission of Mel.

82.

15-82

Solution, Summary

1. Newimplied value: $ 15,000 ÷ 30% = $ 50,000

2. Old implied value: $ 70,000 ÷ 70% = $100,000

3. BV of net assets: $ 70,000 + $15,000 = $ 85,000

4. Implied Goodwill = $100,000 $85,000 = $ 15,000

5. Goodwill belongs to new partner (because

$50,000 is less than $100,000). [Implies that

he “gave” less for his relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

Note that we use the small pie here with bonus method.

83.

15-83

Note that thisis 30% of the

“Small Pie” because we don’t

revalue the balance sheet!

Group Exercise: Goodwill Method Solution

Entry to record admission of Mel

Cash 15,000

Capital, Jim 7,000

Capital, June 3,500

Capital, Mel 25,500

x 30% = $25,500

Small Pie =

70,000 +

15,000 =

85,000

Note: The bonus to the new partner is shared between the

old partners in their old profit and loss sharing ratio

of 2:1.

84.

15-84

Comprehensive Group Problem

Jennand Amanda are in partnership—they share profits and losses in

the ratio of 7:1, respectively, and they have capital balances of

$30,000 each. The partnership’s land has a fair value of $30,000 in

excess of book value. Tommy is admitted into the partnership for a

cash contribution of $25,000. The new profit and loss sharing

formula is Jenn, 70%, Amanda, 10%, and Tommy, 20%. The value of

the partnership’s existing goodwill is agreed to be $10,000.

REQUIRED

1. Prepare the required entries, assuming the land is to be revalued and the

goodwill is to be recorded on the partnership’s books.

2. Prepare the required entries, assuming that the bonus method is to be

used with respect to the undervalued existing assets and the goodwill.

Note that this goodwill number is given because it is a bit harder to

calculate when there is also unrecorded appreciation in existing

assets. However, the next slide shows the calculation.

85.

15-85

Solution, Summary

1. Newimplied value: $ 25,000 ÷ 20% = $125,000

2. Old implied value: $ 60,000 ÷ 80% = $ 75,000

3. BV of net assets: $ 60,000 + $25,000 = $ 85,000

4. Total Excess Value = $125,000 $85,000 = $ 40,000

Goodwill = Total Excess Value – Excess Land Value

Goodwill = $40,000 - $30,000 = $10,000

5. Goodwill belongs to the old partners (because

$75,000 is less than $125,000). [Implies that they

“gave” less for their relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

GW = 10,000

60,000 +

25,000 =

85,000

Land = 30,000

86.

15-86

Note that this

is20% of the

“Big Pie.”

Comprehensive Group Problem Solution

PART 1 (Revaluation / Goodwill Method):

To revalue existing assets to their current values.

To record goodwill.

To record cash contribution by Tommy.

Land 30,000

Capital, Jenn 26,250

Capital, Amanda 3,750

Goodwill 10,000

Capital, Jenn 8,750

Capital, Amanda 1,250

Cash 25,000

Capital, Tommy 25,000

x 20% = $25,000

GW = 10,000

60,000 +

25,000 =

85,000

Land = 30,000

87.

15-87

Comprehensive Group ProblemSolution

PART 2 (Bonus Method):

If the partnership were sold one day after Tommy was admitted and the

selling price was $40,000 more than the book value of the net assets, Tommy

would share in the $40,000 gain to the extent of $8,000 (20% × $40,000), the

amount of his capital contribution that is given as a bonus to Jenn and

Amanda.

Cash 25,000

Capital, Jenn 7,000

Capital, Amanda 1,000

Capital, Tommy 17,000

Note that this is 20% of the

“Small Pie” without revaluing

the land ($60,000 + $25,000).

x 20% = $17,000

Small Pie =

60,000 +

25,000 =

85,000 Note: The bonus to be given the old partners is Tommy’s

profit and loss sharing percentage of 20%

multiplied by the sum of the undervalued existing

assets ($30,000) and the goodwill ($10,000).

88.

15-88

Legal Aspects: Joininga Partnership

A major risk of joining an existing

partnership is the general practice of

requiring the new partner to become

jointly responsible for

all pre-existing partnership liabilities.

all pre-existing contingent liabilities.

89.

15-89

Legal Aspects: Withdrawingfrom a Partnership

A partner that withdraws from a

partnership is still responsible for the

following items that exist at the time of the

withdrawal:

all partnership obligations, and

all contingent liabilities,

Only creditors can expressly release a

partner from this responsibility.

90.

15-90

Legal Aspects: Withdrawingfrom a Partnership

Disassociation

A broad term that refers to when a partner is no

longer associated with a partnership.

Dissolution

A narrow term that refers to when a

(1) partnership is dissolved, and

(2) its affairs must be wound up.

Thus, the partnership’s existence is terminated.

91.

15-91

Practice Quiz Question#6

Upon withdrawal from a partnership, Cliff

received $14,000 cash in excess of his capital

balance. Cliff’s share of profits and losses was

20%. Partnership land was undervalued by

$50,000. The total partnership goodwill is

a. $ 4,000.

b. $20,000.

c. $24,000

d. $70,000.

92.

15-92

Solution

Excess value ofland $50,000

x 20%

Cliff’s share $10,000

Total excess payment $14,000

Share of land excess 10,000

Cliff’s share of goodwill $ 4,000

20%

Total Goodwill $20,000

93.

15-93

Practice Quiz Question#6 Solution

Upon withdrawal from a partnership, Cliff

received $14,000 cash in excess of his capital

balance. Cliff’s share of profits and losses was

20%. Partnership land was undervalued by

$50,000. The total partnership goodwill is

a. $ 4,000.

b. $20,000. (5 x [$14,000 - {20% x $50,000}])

c. $24,000

d. $70,000.

94.

15-94

Group Exercise: Retirement

The6/30/X8 balance sheet of the partnership of Sandy, Rees, and

Raymond as follows. The partners share profits and losses in the ratio

of 2:2:6, respectively.

Assets at cost $145,000

Liabilities 26,000

Capital, Sandy 20,000

Capital, Rees 37,000

Capital, Raymond 62,000

Sandy retires from the partnership. By mutual agreement, the assets

are to be adjusted to their fair value of $150,000 at 6/30/X8. Rees

and Raymond agree that the partnership will pay Sandy $45,000 cash

for her partnership interest. No goodwill is to be recorded.

REQUIRED

1. Prepare the entry to record the revaluation of assets to fair value.

2. Prepare the entry to record Sandy’s retirement.

3. What is the implicit total goodwill for the partnership?

95.

15-95

Group Exercise Solution

PART1

Assets 5,000

Capital, Sandy 1,000

Capital, Rees 1,000

Capital, Raymond 3,000

PART 2

Capital, Sandy 21,000

Capital, Rees 6,000

Capital, Raymond 18,000

Cash 45,000

PART 3

To revalue assets to their current value.

To record the withdrawal of Sandy.

Sandy received a bonus of $24,000, which was equal to her share of the

goodwill. Because Sandy’s profit and loss sharing ratio was 20%, the total

goodwill must have been $120,000 ($24,000 ÷ 20%).

![15-73

Solution, Summary

1. New implied value: $ 54,000 ÷ 25% = $216,000

2. Old implied value: $180,000 ÷ 75% = $240,000

3. BV of net assets: $180,000 + $54,000 = $234,000

4. Implied Goodwill = $240,000 $234,000 = $ 6,000

5. Goodwill belongs to new partner (because

$216,000 is less than $240,000). [Implies that

she paid less for her relative share of the business.]

Since we’re revaluing, use the BIG pie:

x 25% = $60,000

GW = 6,000

234,000

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)](https://image.slidesharecdn.com/chapter15akl-230901024827-42585ab4/85/chapter-15-akl-pptx-73-320.jpg)

![15-76

Solution, Summary

1. New implied value: $ 54,000 ÷ 25% = $216,000

2. Old implied value: $180,000 ÷ 75% = $240,000

3. BV of net assets: $180,000 + $54,000 = $234,000

4. Implied Goodwill = $240,000 $234,000 = $ 6,000

5. Goodwill belongs to new partner (because

$216,000 is less than $240,000). [Implies that

she paid less for her relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

Small Pie

= 180,000

+ 54,000

= 234,000 x 25% = $58,500

Since we’re not

revaluing, use the

Small pie:](https://image.slidesharecdn.com/chapter15akl-230901024827-42585ab4/85/chapter-15-akl-pptx-76-320.jpg)

![15-79

Solution, Summary

1. New implied value: $ 60,000 ÷ 25% = $240,000

2. Old implied value: $165,000 ÷ 75% = $220,000

3. BV of net assets: $165,000 + $60,000 = $225,000

4. Implied Goodwill = $240,000 $225,000 = $ 15,000

5. Goodwill belongs to old partners (because

$220,000 is less than $240,000). [Implies that

they “gave” less for their relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)](https://image.slidesharecdn.com/chapter15akl-230901024827-42585ab4/85/chapter-15-akl-pptx-79-320.jpg)

![15-82

Solution, Summary

1. New implied value: $ 15,000 ÷ 30% = $ 50,000

2. Old implied value: $ 70,000 ÷ 70% = $100,000

3. BV of net assets: $ 70,000 + $15,000 = $ 85,000

4. Implied Goodwill = $100,000 $85,000 = $ 15,000

5. Goodwill belongs to new partner (because

$50,000 is less than $100,000). [Implies that

he “gave” less for his relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

Note that we use the small pie here with bonus method.](https://image.slidesharecdn.com/chapter15akl-230901024827-42585ab4/85/chapter-15-akl-pptx-82-320.jpg)

![15-85

Solution, Summary

1. New implied value: $ 25,000 ÷ 20% = $125,000

2. Old implied value: $ 60,000 ÷ 80% = $ 75,000

3. BV of net assets: $ 60,000 + $25,000 = $ 85,000

4. Total Excess Value = $125,000 $85,000 = $ 40,000

Goodwill = Total Excess Value – Excess Land Value

Goodwill = $40,000 - $30,000 = $10,000

5. Goodwill belongs to the old partners (because

$75,000 is less than $125,000). [Implies that they

“gave” less for their relative share of the business.]

The BIG PIE (BV of NA + Goodwill)

The SMALL PIE (BV Only)

GW = 10,000

60,000 +

25,000 =

85,000

Land = 30,000](https://image.slidesharecdn.com/chapter15akl-230901024827-42585ab4/85/chapter-15-akl-pptx-85-320.jpg)

![15-93

Practice Quiz Question #6 Solution

Upon withdrawal from a partnership, Cliff

received $14,000 cash in excess of his capital

balance. Cliff’s share of profits and losses was

20%. Partnership land was undervalued by

$50,000. The total partnership goodwill is

a. $ 4,000.

b. $20,000. (5 x [$14,000 - {20% x $50,000}])

c. $24,000

d. $70,000.](https://image.slidesharecdn.com/chapter15akl-230901024827-42585ab4/85/chapter-15-akl-pptx-93-320.jpg)