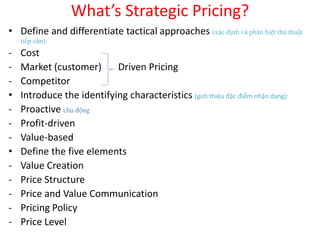

This document outlines strategic pricing approaches and concepts. It discusses cost-plus pricing, which sets price as costs plus a percentage markup. Customer-driven pricing sets price based on customer perceived value rather than costs. Share-driven pricing matches competitors' prices to gain market share. Strategic pricing is defined as proactive, profit-driven, and value-based. It considers five elements: value creation, price structure, communicating price and value, pricing policy, and price level. Strategic pricing creates a pricing pyramid to maximize profits.