How to Doxtabond2

How to Do xtabond2

David Roodman

David Roodman

Research Fellow

Research Fellow

Center for Global Development

Center for Global Development

2.

xtabond2 in anutshell

xtabond2 in a nutshell

First ado version in 11/03, Mata version in 11/05.

Extends built-in xtabond, to do system GMM,

Windmeijer correction, revamped syntax

Estimators designed for

– Small-T, large-N panels

– One dependent variable

– Dynamic

– Linear

– Regressors endogenous and predetermined

– Fixed individual effects

– Arbitrary autocorrelation and het. within panels

– General application

3.

Outline of paper

Outlineof paper

Introduction to linear GMM

Motivation and design of

difference and system GMM

xtabond2 syntax

4.

Black box problem

Blackbox problem

Canned & sophisticated procedure

Dangers in hidden sophistication

– finite sample ≠ asymptotic

Users should understand motivation and

limits of estimator

5.

Linear GMM inone slide

Linear GMM in one slide

Instrument vector z such that 0

z

]

E[

# instruments > # parameters so can’t have 0

E

Z

z

ˆ

]

[

E '

1

N

N

Want to “minimize” E

Z ˆ

'

1

N in some sense

In what sense? By a pos-semi-def. quad. form given by A:

E

ZAZ

E

E

Z

A

E

Z

E

Z

z

A

A

ˆ

ˆ

1

ˆ

1

ˆ

1

ˆ

1

E '

'

'

'

'

'

N

N

N

N

N

N

Given A, minimizing leads to Y

ZAZ

X

X

ZAZ

X

A

'

'

1

'

'

ˆ

β

Always unbiased, but which A is efficient? Answer: A should weight

moments E

z'

i inversely with their variances and

covariances:

1

'

1

'

1

'

,

Var

,

Var

Z

Ω

Z

Z

Z

X

E

Z

Z

X

E

Z

AEGMM

To make feasible, choose arbitrary proxy for ,

Ω call it H. Do GMM

(one-step). Use residuals to make robust sandwich estimator of

1

'

Z

Ω

Z . Rerun. Two-step is feasible, theoretically efficient.

6.

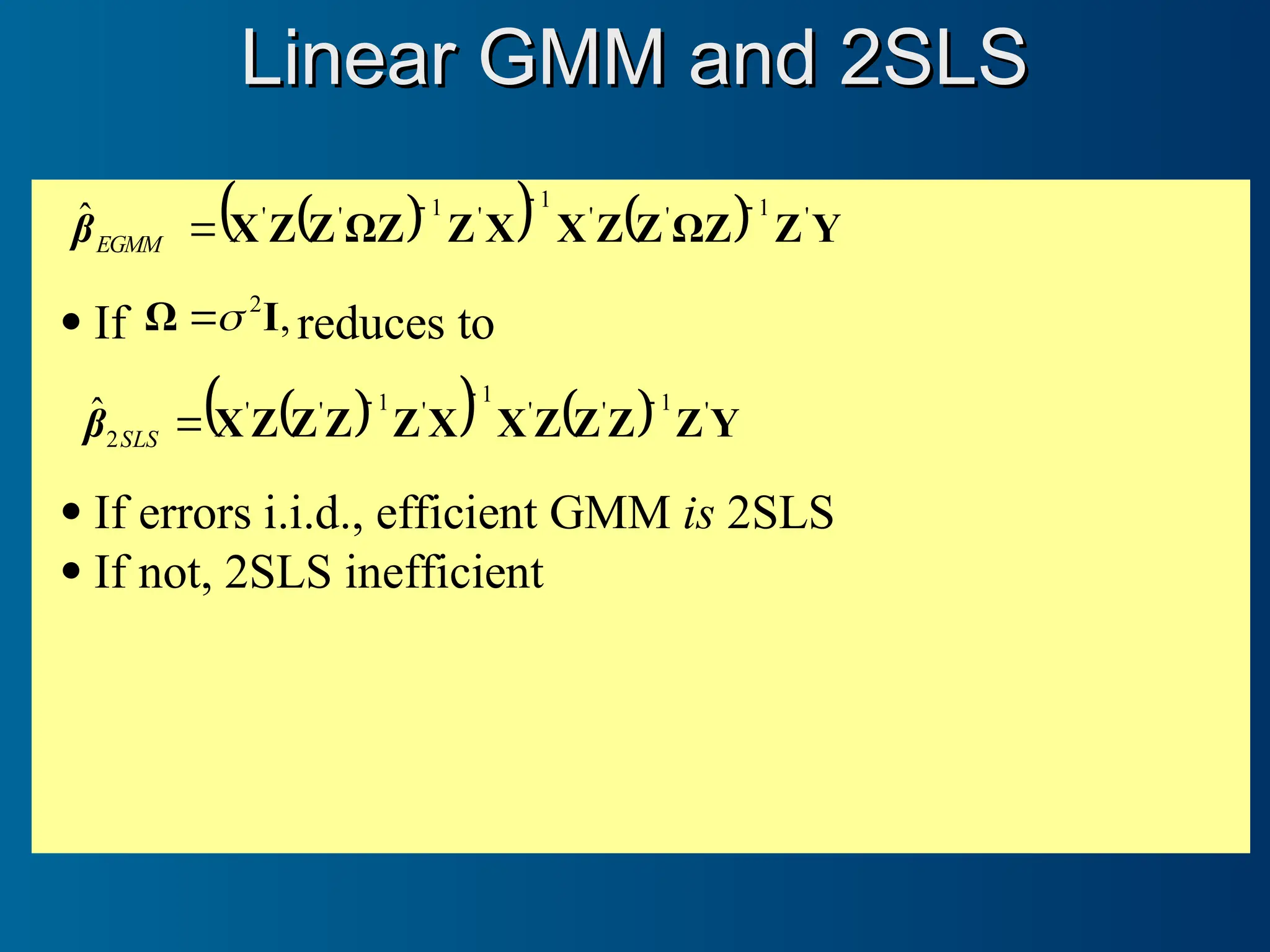

Linear GMM and2SLS

Linear GMM and 2SLS

Y

Z

Z

Ω

Z

Z

X

X

Z

Z

Ω

Z

Z

X '

1

'

'

1

'

1

'

'

ˆ

EGMM

β

If ,

2

I

Ω

reduces to

Y

Z

Z

Z

Z

X

X

Z

Z

Z

Z

X '

1

'

'

1

'

1

'

'

2

ˆ

SLS

β

If errors i.i.d., efficient GMM is 2SLS

If not, 2SLS inefficient

7.

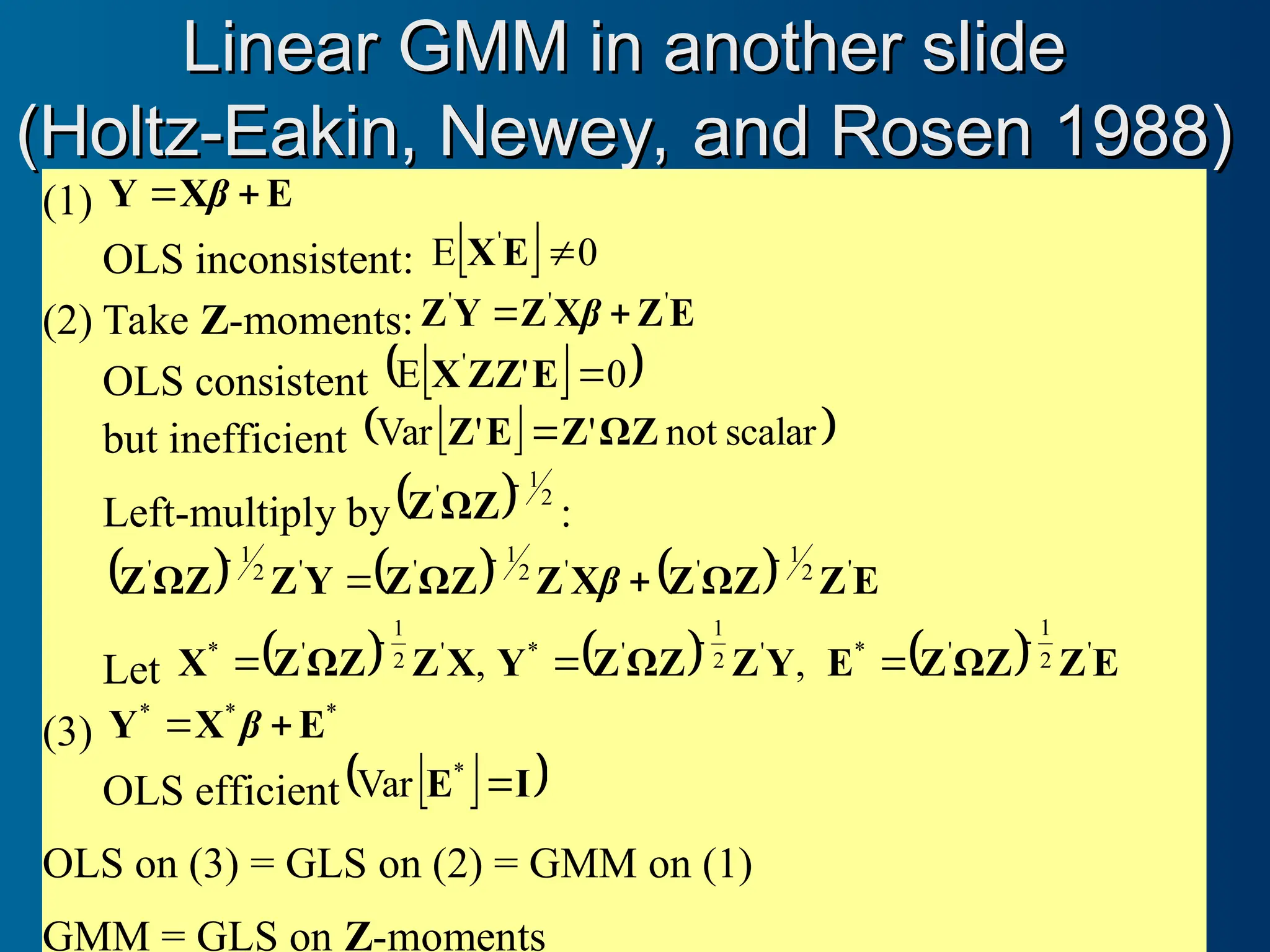

Linear GMM inanother slide

Linear GMM in another slide

(Holtz-Eakin, Newey, and Rosen 1988)

(Holtz-Eakin, Newey, and Rosen 1988)

(1) E

X

Y

β

OLS inconsistent: 0

E '

E

X

(2) Take Z-moments: E

Z

X

Z

Y

Z '

'

'

β

OLS consistent

0

'

E '

E

ZZ

X

but inefficient

scalar

not

'

'

Var ΩZ

Z

E

Z

Left-multiply by 2

1

'

ΩZ

Z :

E

Z

ΩZ

Z

X

Z

ΩZ

Z

Y

Z

ΩZ

Z '

2

1

'

'

2

1

'

'

2

1

'

β

Let ,

'

2

1

'

*

X

Z

ΩZ

Z

X

,

'

2

1

'

*

Y

Z

ΩZ

Z

Y

E

Z

ΩZ

Z

E '

2

1

'

*

(3)

*

*

*

E

X

Y

β

OLS efficient

I

E

Var *

OLS on (3) = GLS on (2) = GMM on (1)

GMM = GLS on Z-moments

8.

Difference and systemGMM

Difference and system GMM

Basic model:

0

E

E

E

'

1

,

it

i

it

i

it

i

it

it

it

t

i

it y

y

β

x

Conceptual starting point: OLS

9.

Fixed effects indisturbance term make 1

,

t

i

y endogenous

o Example: Indonesia

A problem of short panels

Individual dummies (=Within Groups) don’t help

o Transformed 1

,

t

i

y endogenous, as are deeper lags

Problem: Dynamic Panel Bias (Nickell 1981)

Problem: Dynamic Panel Bias (Nickell 1981)

10.

it

it

t

i

it y

y

β

'

1

, x

Purges fixed effects, doesn’t spread endogeneity much

Transformed 1

,

t

i

y still becomes endogenous since the

1

,

t

i

y in 2

,

1

,

1

,

t

i

t

i

t

i y

y

y correlates with the 1

,

t

i

in

1

,

t

i

it

it

But deeper lags exogenous if no AR(), offering

instruments

Partial solution: OLS in differences

Partial solution: OLS in differences

11.

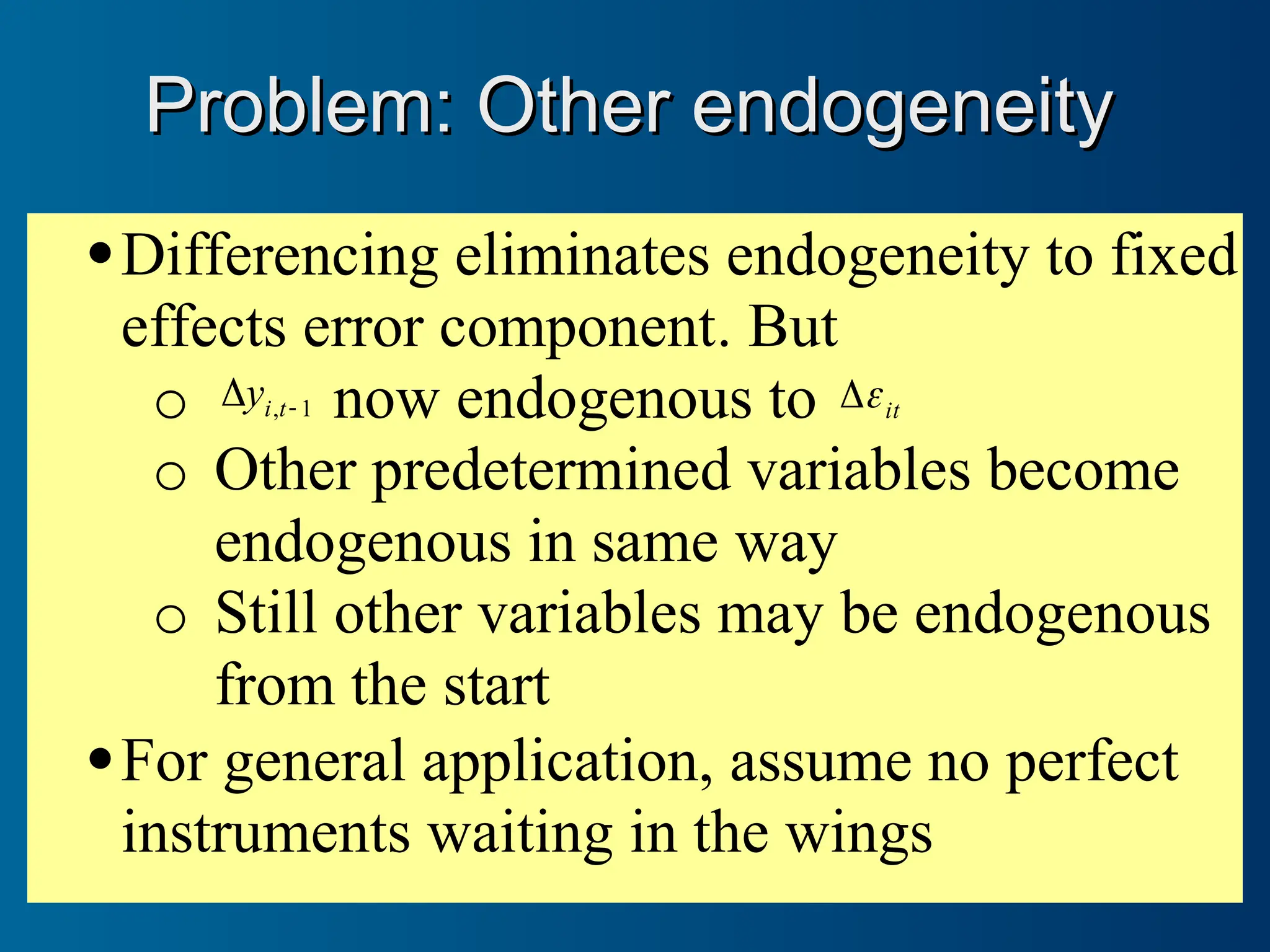

Differencing eliminates endogeneityto fixed

effects error component. But

o 1

,

t

i

y now endogenous to it

o Other predetermined variables become

endogenous in same way

o Still other variables may be endogenous

from the start

For general application, assume no perfect

instruments waiting in the wings

Problem: Other endogeneity

Problem: Other endogeneity

12.

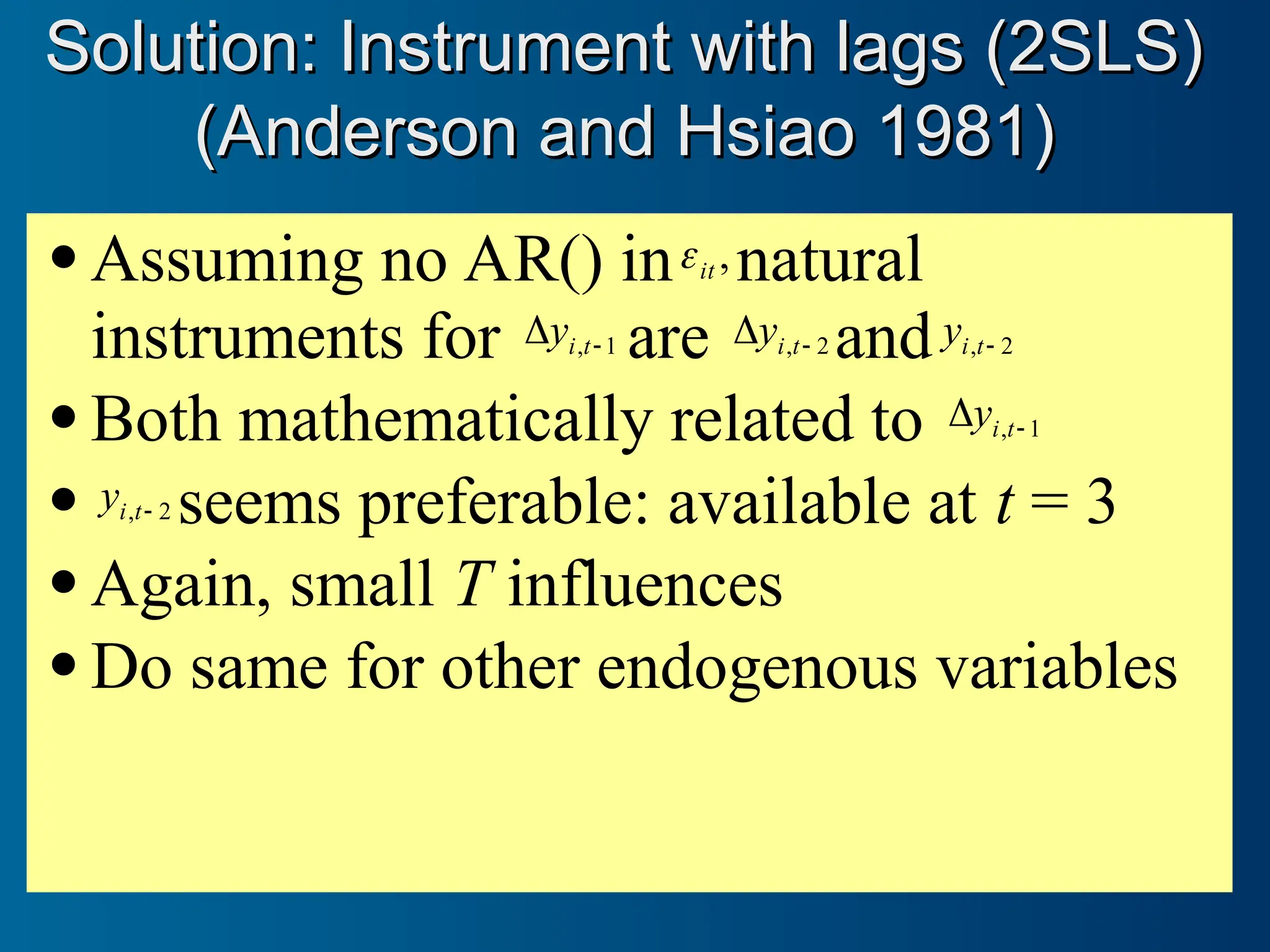

Assuming noAR() in ,

it

natural

instruments for 1

,

t

i

y are 2

,

t

i

y and 2

,

t

i

y

Both mathematically related to 1

,

t

i

y

2

,

t

i

y seems preferable: available at t = 3

Again, small T influences

Do same for other endogenous variables

Solution: Instrument with lags (2SLS)

Solution: Instrument with lags (2SLS)

(Anderson and Hsiao 1981)

(Anderson and Hsiao 1981)

13.

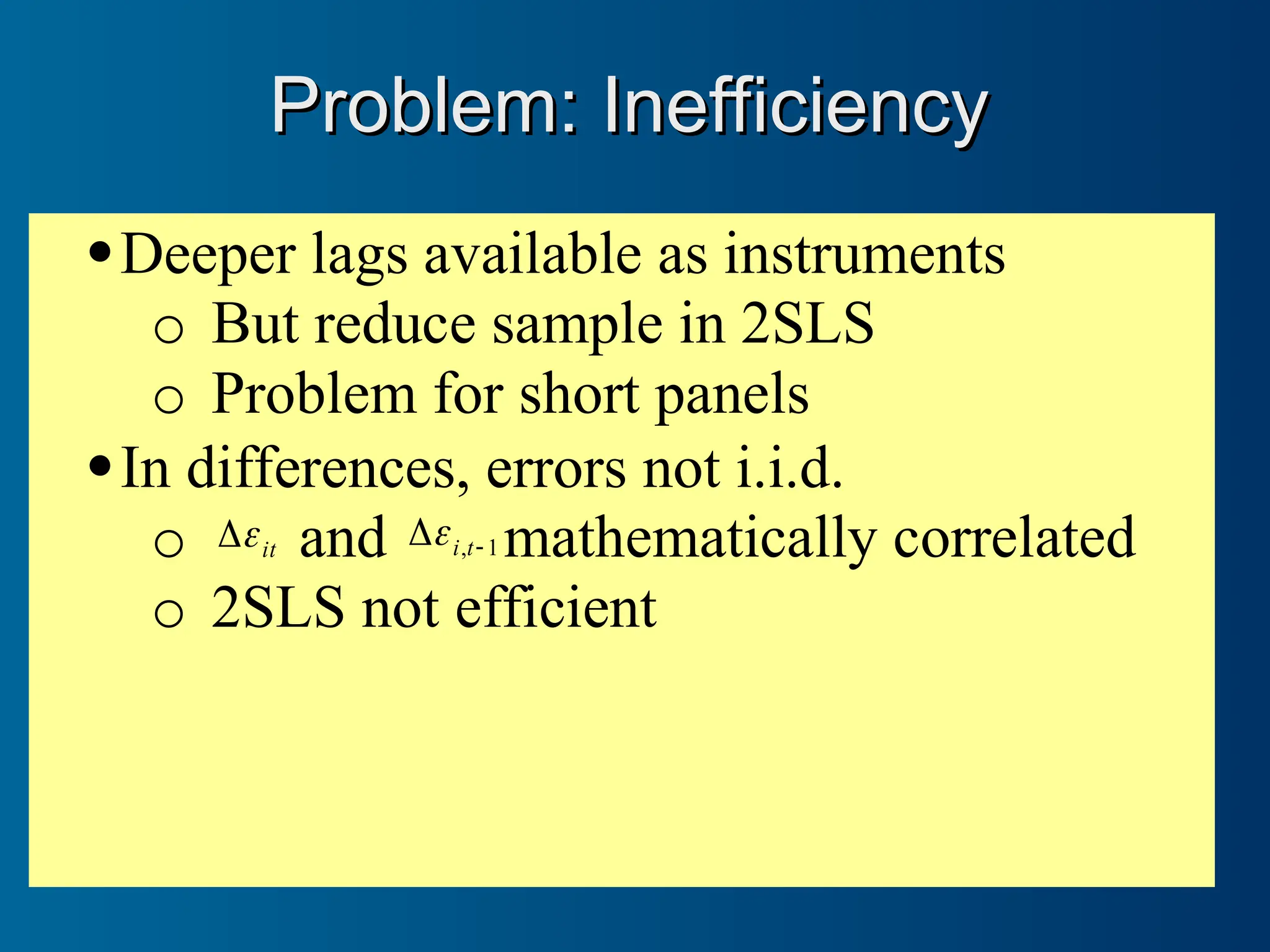

Deeper lags availableas instruments

o But reduce sample in 2SLS

o Problem for short panels

In differences, errors not i.i.d.

o it

and 1

,

t

i

mathematically correlated

o 2SLS not efficient

Problem: Inefficiency

Problem: Inefficiency

14.

Use many lags,replacing missing with zero

Generate separate instrument for each lag and time

period instrumented

IV-style:

2

,

1

.

.

T

i

i

y

y

GMM-style:

.

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

1

2

3

1

2

1

i

i

i

i

i

i

y

y

y

y

y

y

Result: Arellano-Bond (1991) difference GMM

Solution: GMM & GMM-style instruments

Solution: GMM & GMM-style instruments

(Holtz-Eakin, Newey, and Rosen 1988)

(Holtz-Eakin, Newey, and Rosen 1988)

15.

E.g., ifit

are AR(1), then it

t

i

t

i

t

i

y

~

~

~ 1

,

2

,

2

,

Must assume 2

,

t

i

y is invalid instrument in i,t

Problem: Autocorrelation

Problem: Autocorrelation

16.

If wefind AR(l) in it

, use lags l + 1 and deeper

Solution: Restrict to deeper lags

Solution: Restrict to deeper lags

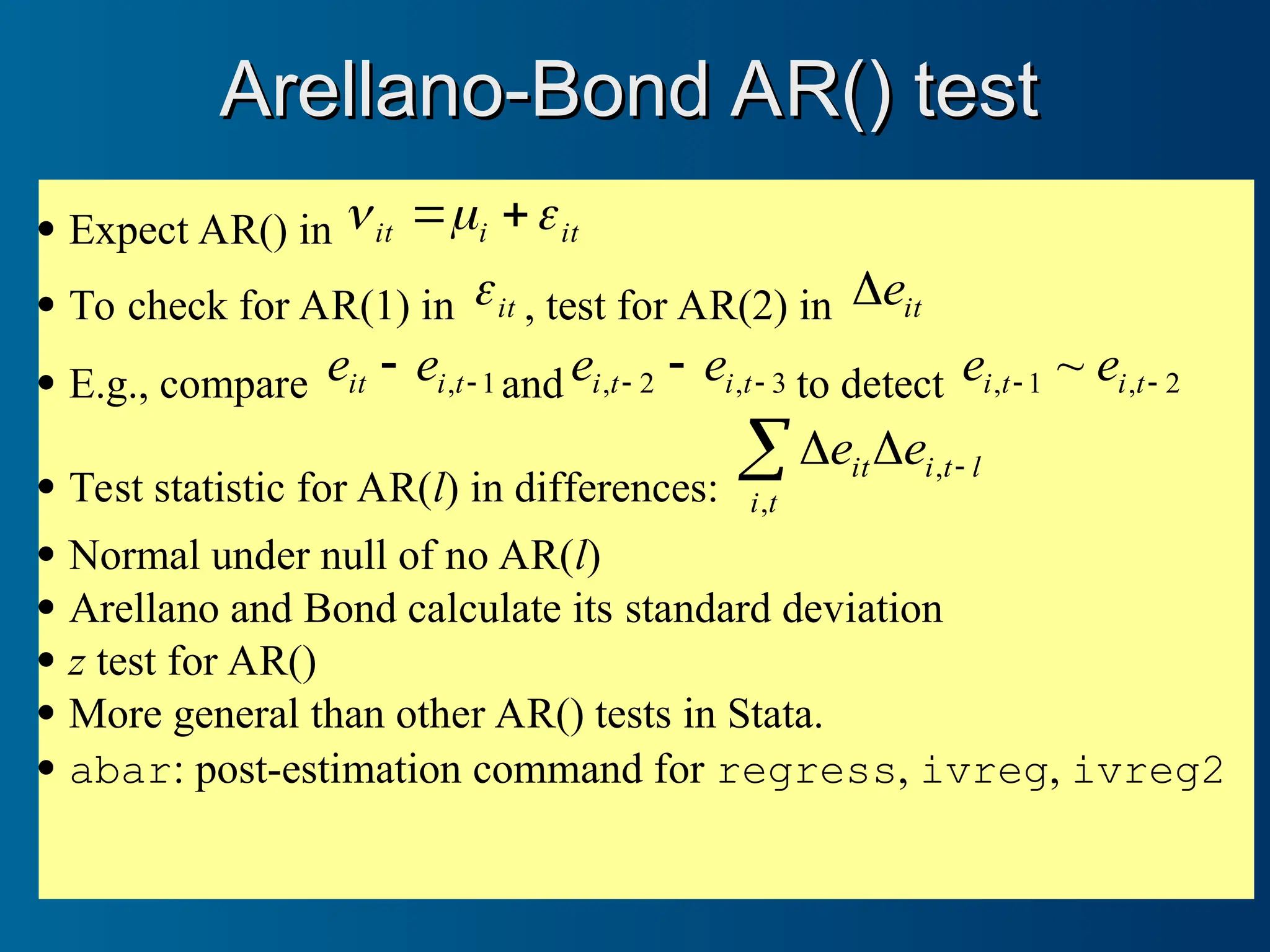

17.

Expect AR()in it

i

it

To check for AR(1) in it

, test for AR(2) in it

e

E.g., compare 1

,

t

i

it e

e and 3

,

2

,

t

i

t

i e

e to detect 2

,

1

, ~

t

i

t

i e

e

Test statistic for AR(l) in differences:

t

i

l

t

i

it e

e

,

,

Normal under null of no AR(l)

Arellano and Bond calculate its standard deviation

z test for AR()

More general than other AR() tests in Stata.

abar: post-estimation command for regress, ivreg, ivreg2

Arellano-Bond AR() test

Arellano-Bond AR() test

18.

If y isnearly a random walk, 1

,

t

i

y is a poor

instrument for it

y

, mathematical

relationship notwithstanding

Problem: Weak instruments

Problem: Weak instruments

19.

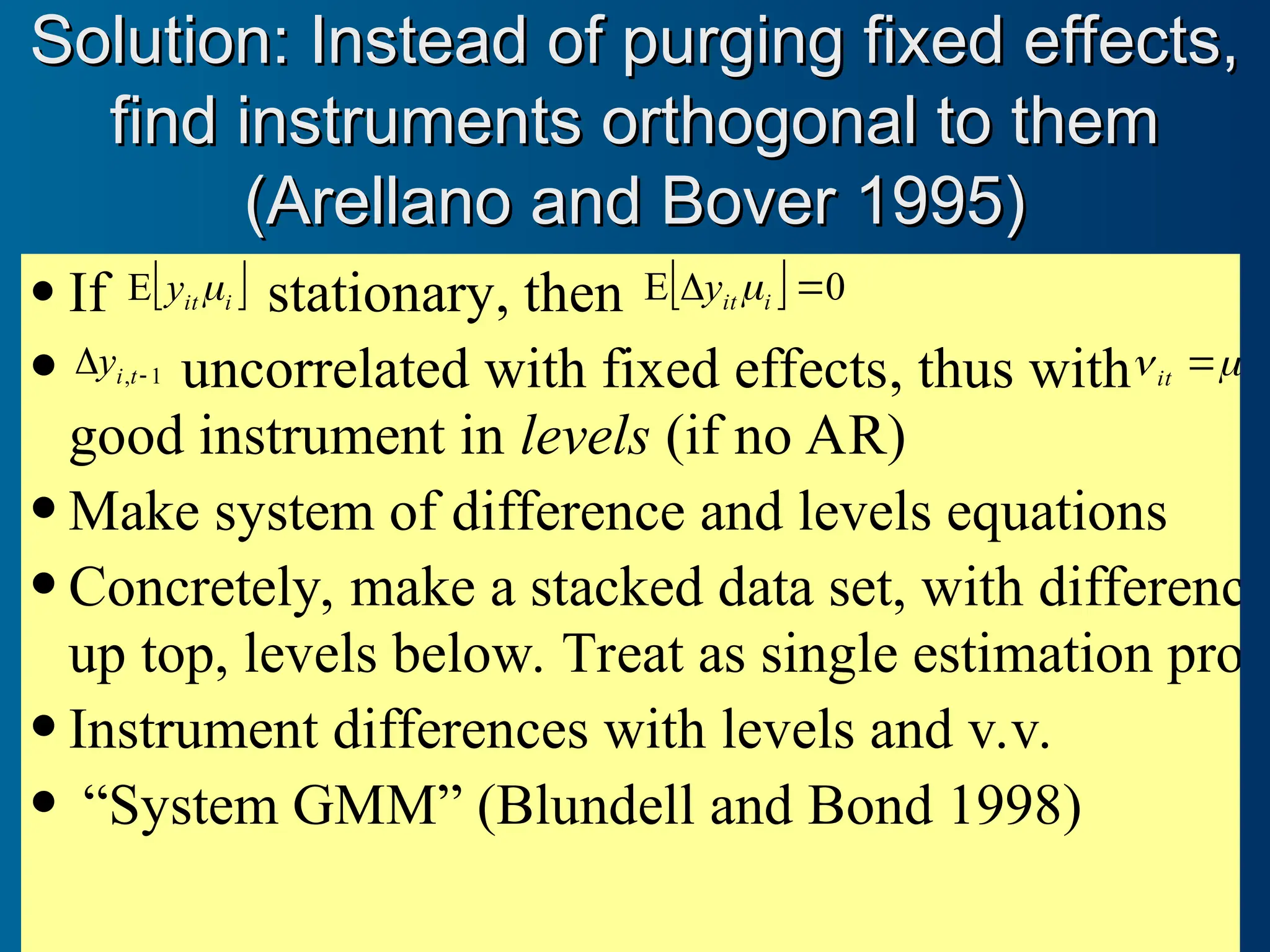

If

i

it

y

E stationary, then 0

E

i

it

y

1

,

t

i

y uncorrelated with fixed effects, thus with i

it

good instrument in levels (if no AR)

Make system of difference and levels equations

Concretely, make a stacked data set, with difference

up top, levels below. Treat as single estimation prob

Instrument differences with levels and v.v.

“System GMM” (Blundell and Bond 1998)

Solution: Instead of purging fixed effects,

Solution: Instead of purging fixed effects,

find instruments orthogonal to them

find instruments orthogonal to them

(Arellano and Bover 1995)

(Arellano and Bover 1995)

20.

4

4

3

4

2

4

1

4

4

3

3

3

2

3

1

3

4

2

3

2

2

2

1

2

4

1

3

1

2

1

1

1

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

E

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

i

w

w

w

w

L

w

D

w

w

w

L

w

D

w

D

w

w

L

w

D

w

D

w

D

w

Relationship among moments

Relationship among moments

(Tue Gorgens)

(Tue Gorgens)

L

L

L

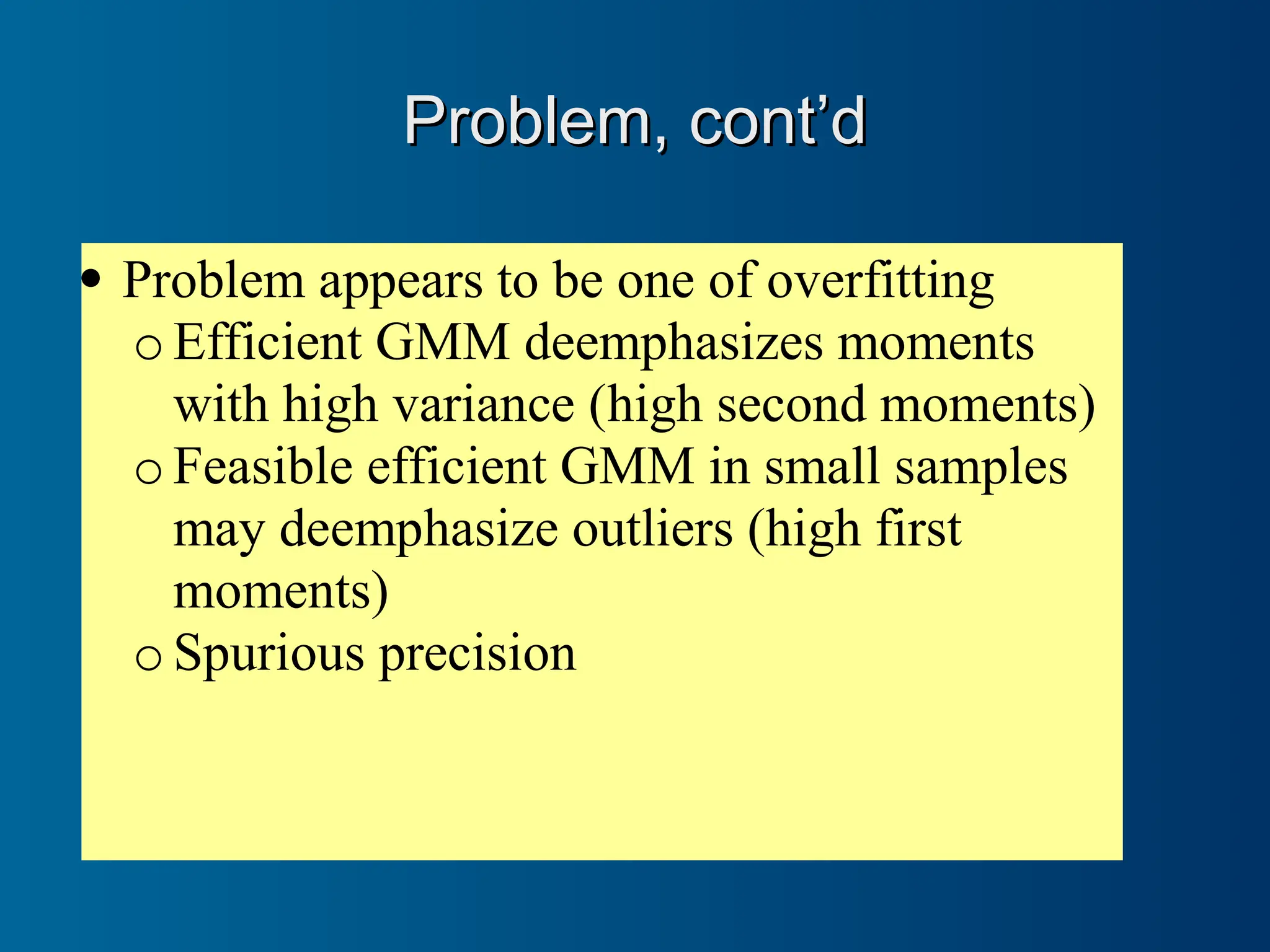

Problem appearsto be one of overfitting

o Efficient GMM deemphasizes moments

with high variance (high second moments)

o Feasible efficient GMM in small samples

may deemphasize outliers (high first

moments)

o Spurious precision

Problem, cont’d

Problem, cont’d

23.

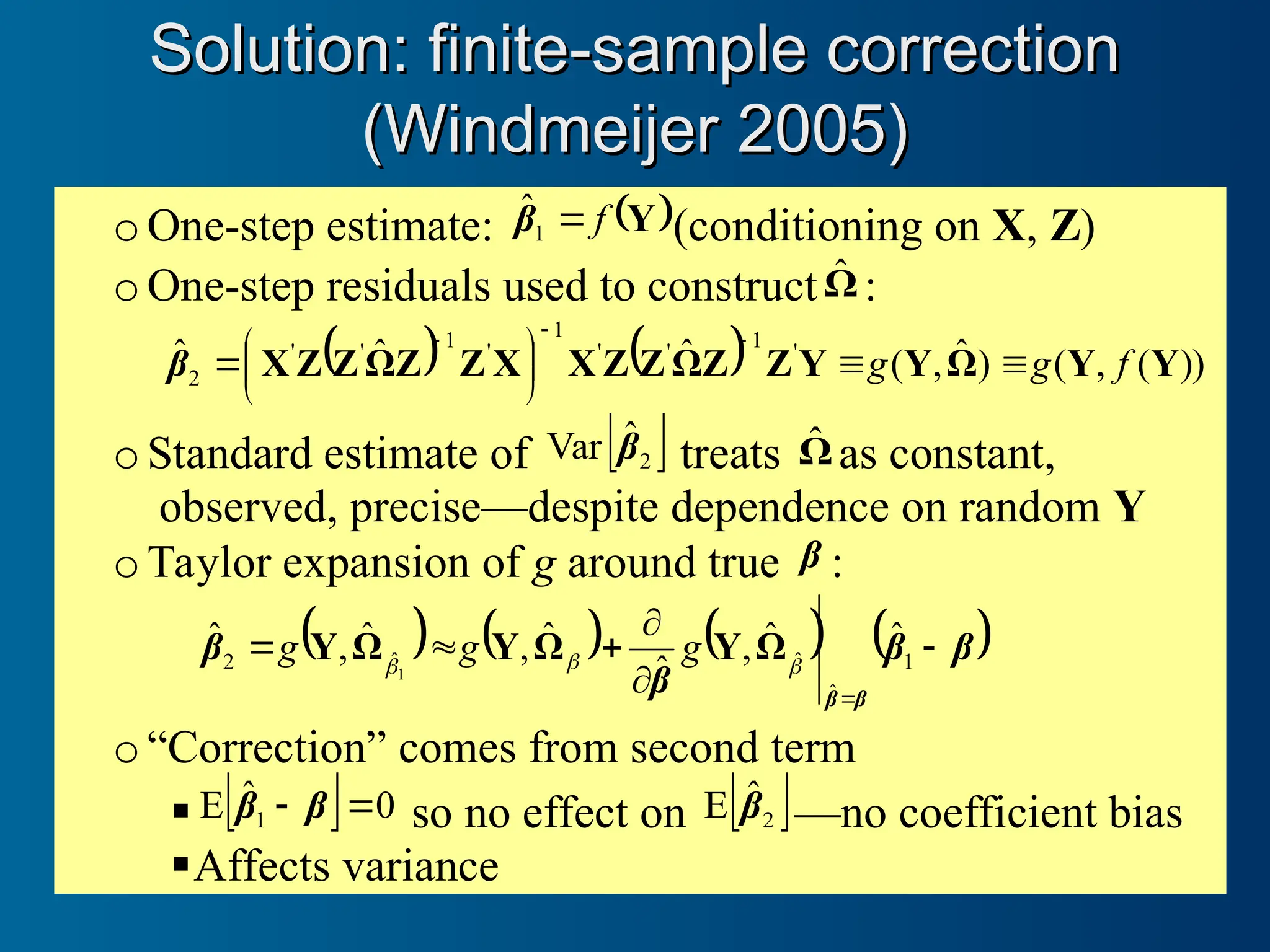

oOne-step estimate:

Y

f

1

β̂ (conditioning on X, Z)

oOne-step residuals used to constructΩ̂ :

))

(

,

(

)

ˆ

,

(

ˆ

ˆ

ˆ '

1

'

'

1

'

1

'

'

2 Y

Y

Ω

Y

Y

Z

Z

Ω

Z

Z

X

X

Z

Z

Ω

Z

Z

X f

g

g

β

oStandard estimate of

2

ˆ

Var β treats Ω̂ as constant,

observed, precise—despite dependence on random Y

oTaylor expansion of g around true β :

β

β

β

β

β

β

1

ˆ

ˆ

ˆ

2

ˆ

ˆ

,

ˆ

ˆ

,

ˆ

,

ˆ

1

Ω

Y

Ω

Y

Ω

Y g

g

g

o“Correction” comes from second term

0

ˆ

E 1

β

β so no effect on

2

ˆ

E β —no coefficient bias

Affects variance

Solution: finite-sample correction

Solution: finite-sample correction

(Windmeijer 2005)

(Windmeijer 2005)

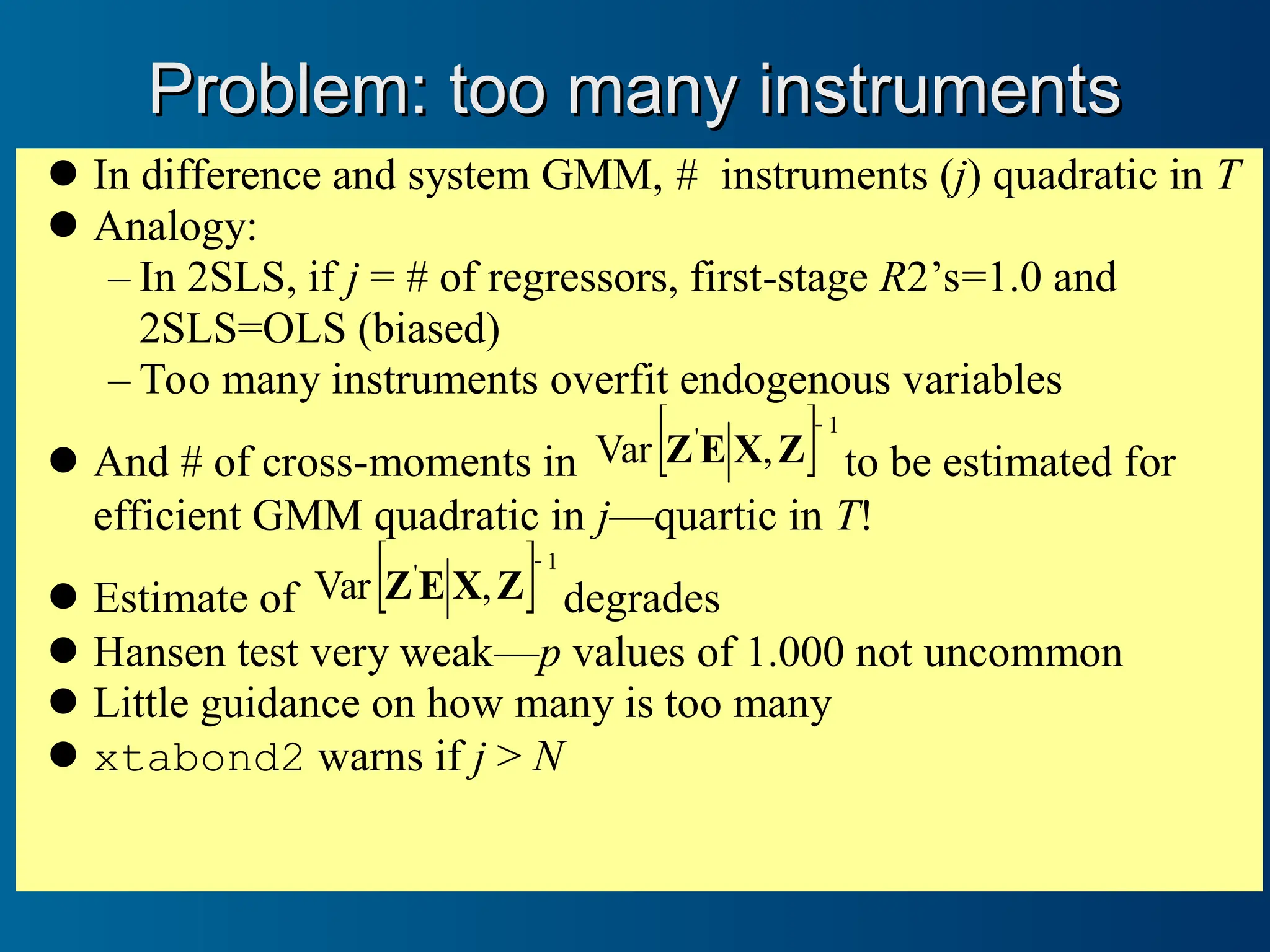

Problem: too manyinstruments

Problem: too many instruments

In difference and system GMM, # instruments (j) quadratic in T

Analogy:

– In 2SLS, if j = # of regressors, first-stage R2’s=1.0 and

2SLS=OLS (biased)

– Too many instruments overfit endogenous variables

And # of cross-moments in 1

'

,

Var

Z

X

E

Z to be estimated for

efficient GMM quadratic in j—quartic in T!

Estimate of 1

'

,

Var

Z

X

E

Z degrades

Hansen test very weak—p values of 1.000 not uncommon

Little guidance on how many is too many

xtabond2 warns if j > N

26.

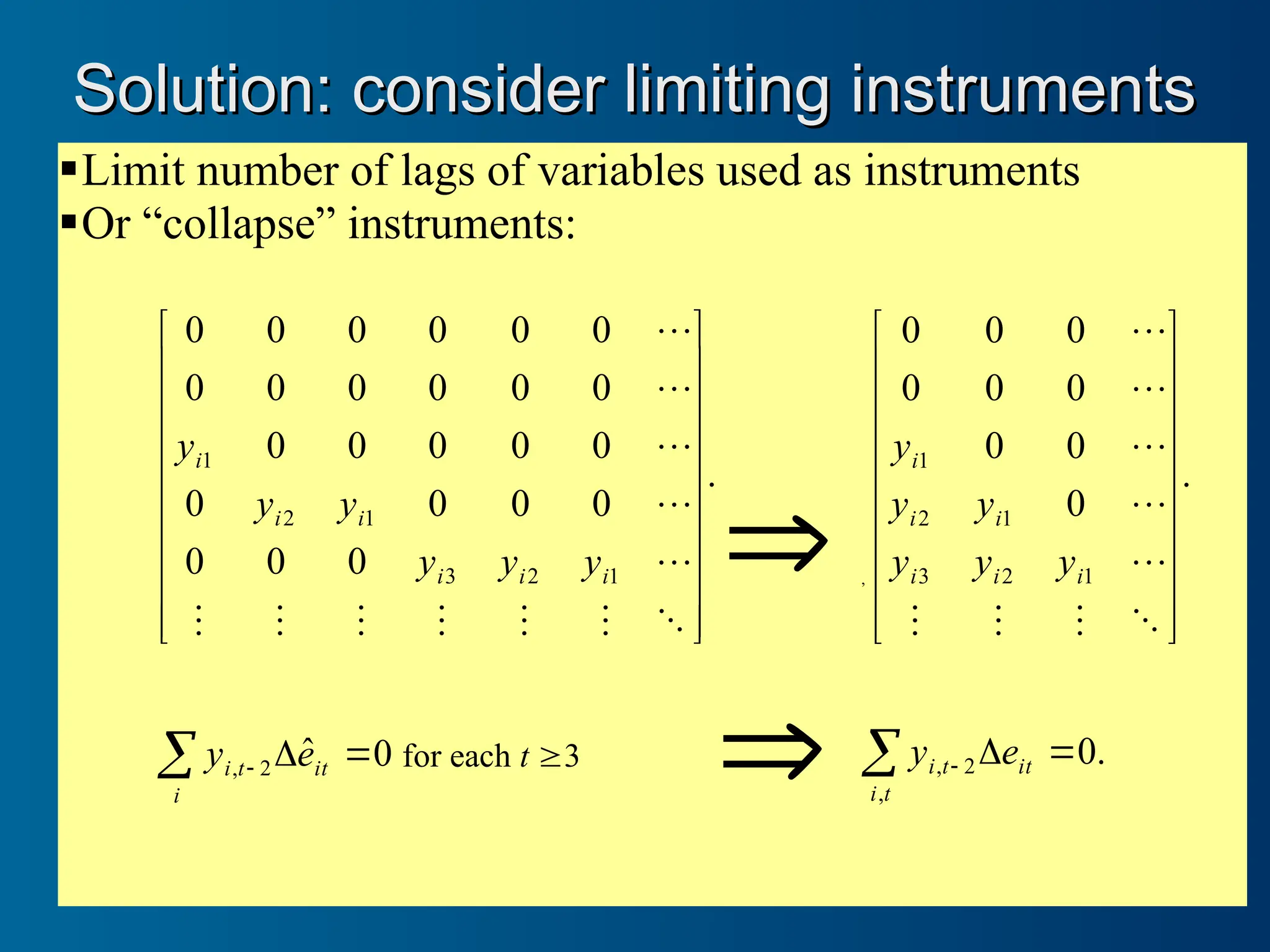

Limit number oflags of variables used as instruments

Or “collapse” instruments:

.

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

1

2

3

1

2

1

i

i

i

i

i

i

y

y

y

y

y

y

,

.

0

0

0

0

0

0

0

0

0

1

2

3

1

2

1

i

i

i

i

i

i

y

y

y

y

y

y

0

ˆ

2

,

it

i

t

i e

y for each t 3

.

0

,

2

,

it

t

i

t

i e

y

Solution: consider limiting instruments

Solution: consider limiting instruments

27.

xtabond2

xtabond2 syntax

syntax

xtabond2 depvarvarlist [if exp] [in range]

[, level(#) twostep robust noconstant small noleveleq

artests(#) arlevels h(#) nomata]

ivopt [ivopt ...] gmmopt [gmmopt ...]]

where gmmopt is

gmmstyle(varlist [, laglimits(# #) collapse

equation({diff | level | both}) passthru])

and ivopt is

ivstyle(varlist [, equation({diff | level | both})

passthru mz])

Y X Z

Classic

“GMM-style”

28.

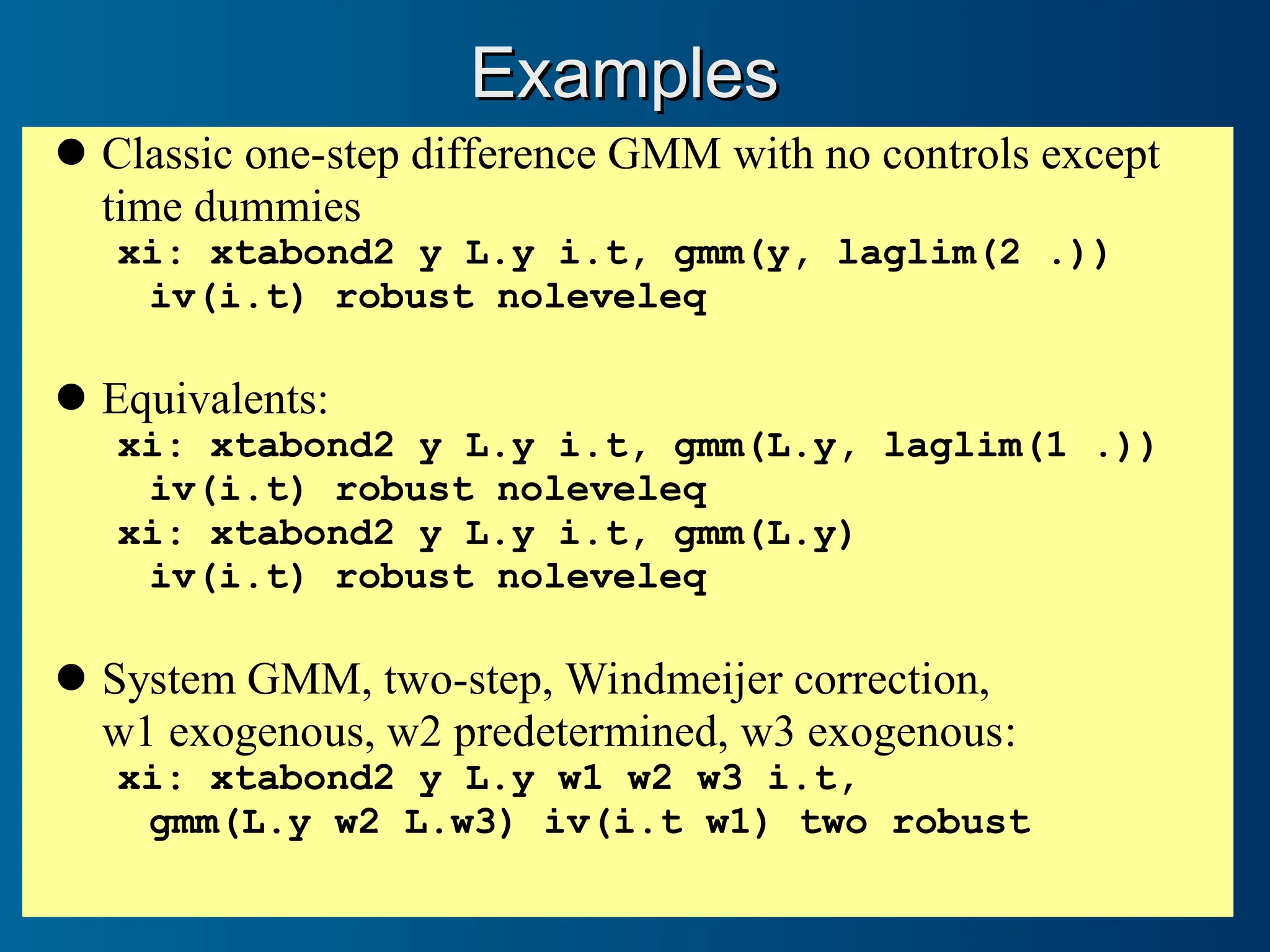

Examples

Examples

Classic one-step differenceGMM with no controls except

time dummies

xi: xtabond2 y L.y i.t, gmm(y, laglim(2 .))

iv(i.t) robust noleveleq

Equivalents:

xi: xtabond2 y L.y i.t, gmm(L.y, laglim(1 .))

iv(i.t) robust noleveleq

xi: xtabond2 y L.y i.t, gmm(L.y)

iv(i.t) robust noleveleq

System GMM, two-step, Windmeijer correction,

w1 exogenous, w2 predetermined, w3 exogenous:

xi: xtabond2 y L.y w1 w2 w3 i.t,

gmm(L.y w2 L.w3) iv(i.t w1) two robust

29.

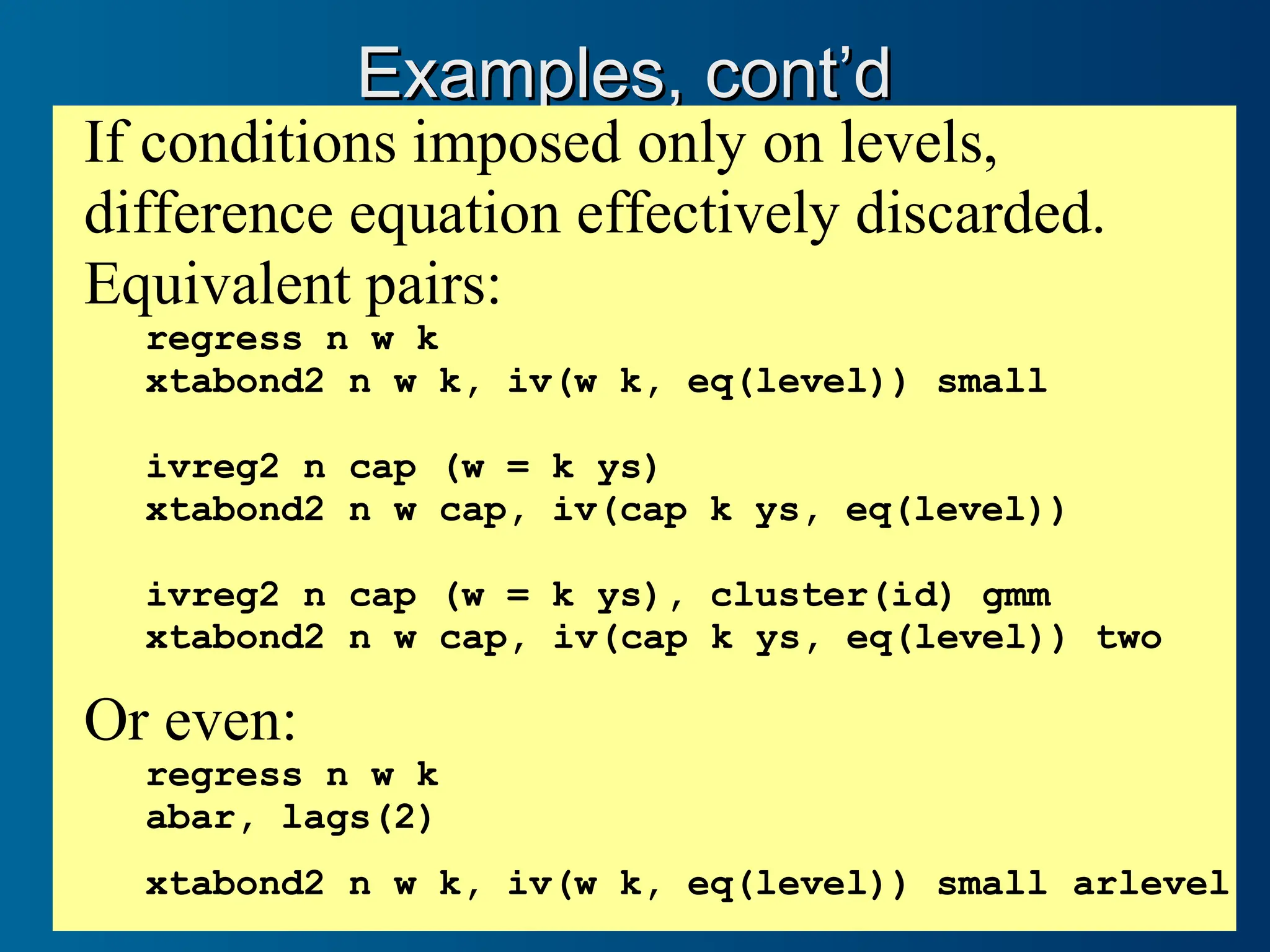

Examples, cont’d

Examples, cont’d

Ifconditions imposed only on levels,

difference equation effectively discarded.

Equivalent pairs:

regress n w k

xtabond2 n w k, iv(w k, eq(level)) small

ivreg2 n cap (w = k ys)

xtabond2 n w cap, iv(cap k ys, eq(level))

ivreg2 n cap (w = k ys), cluster(id) gmm

xtabond2 n w cap, iv(cap k ys, eq(level)) two

Or even:

regress n w k

abar, lags(2)

xtabond2 n w k, iv(w k, eq(level)) small arlevel

30.

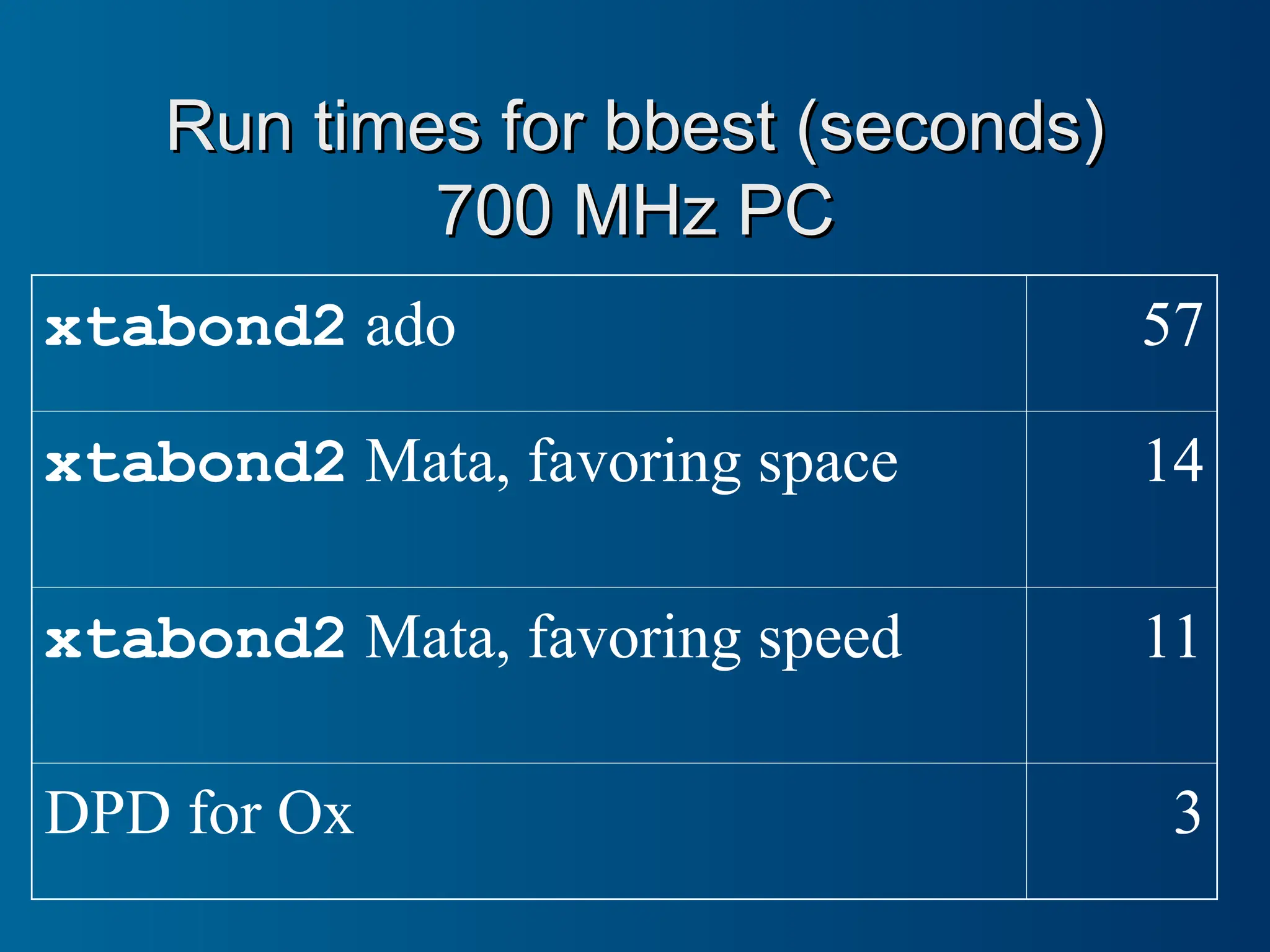

Run times forbbest (seconds)

Run times for bbest (seconds)

700 MHz PC

700 MHz PC

xtabond2 ado 57

xtabond2 Mata, favoring space 14

xtabond2 Mata, favoring speed 11

DPD for Ox 3

![Linear GMM in one slide

Linear GMM in one slide

Instrument vector z such that 0

z

]

E[

# instruments > # parameters so can’t have 0

E

Z

z

ˆ

]

[

E '

1

N

N

Want to “minimize” E

Z ˆ

'

1

N in some sense

In what sense? By a pos-semi-def. quad. form given by A:

E

ZAZ

E

E

Z

A

E

Z

E

Z

z

A

A

ˆ

ˆ

1

ˆ

1

ˆ

1

ˆ

1

E '

'

'

'

'

'

N

N

N

N

N

N

Given A, minimizing leads to Y

ZAZ

X

X

ZAZ

X

A

'

'

1

'

'

ˆ

β

Always unbiased, but which A is efficient? Answer: A should weight

moments E

z'

i inversely with their variances and

covariances:

1

'

1

'

1

'

,

Var

,

Var

Z

Ω

Z

Z

Z

X

E

Z

Z

X

E

Z

AEGMM

To make feasible, choose arbitrary proxy for ,

Ω call it H. Do GMM

(one-step). Use residuals to make robust sandwich estimator of

1

'

Z

Ω

Z . Rerun. Two-step is feasible, theoretically efficient.](https://image.slidesharecdn.com/how2doxtabond2-250630154849-b60c9212/75/Cach-s-d-ng-XTABOND2-trong-STATA-v-i-GMM-5-2048.jpg)

![Problem: Two-step errors too small

Problem: Two-step errors too small

Regression for Arellano-Bond (1991) column (a1), Table 4

Arellano-Bond dynamic panel-data estimation, one-step difference GMM results

------------------------------------------------------------------------------

| Robust

| Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

n |

L1. | .6862261 .1445943 4.75 0.000 .4003376 .9721147

L2. | -.0853582 .0560155 -1.52 0.130 -.1961109 .0253944

w |

--. | -.6078208 .1782055 -3.41 0.001 -.9601647 -.2554769

L1. | .3926237 .1679931 2.34 0.021 .0604714 .7247759

k |

--. | .3568456 .0590203 6.05 0.000 .240152 .4735392

Arellano-Bond dynamic panel-data estimation, two-step difference GMM results

------------------------------------------------------------------------------

| Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

n |

L1. | .6287089 .0904543 6.95 0.000 .4498646 .8075531

L2. | -.0651882 .0265009 -2.46 0.015 -.1175852 -.0127912

w |

--. | -.5257597 .0537692 -9.78 0.000 -.6320709 -.4194485

L1. | .3112899 .0940116 3.31 0.001 .1254122 .4971675

k |

--. | .2783619 .0449083 6.20 0.000 .1895702 .3671537](https://image.slidesharecdn.com/how2doxtabond2-250630154849-b60c9212/75/Cach-s-d-ng-XTABOND2-trong-STATA-v-i-GMM-21-2048.jpg)

![Arellano-Bond dynamic panel-data estimation, one-step difference GMM results

------------------------------------------------------------------------------

| Robust

| Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

n |

L1. | .6862261 .1445943 4.75 0.000 .4003376 .9721147

L2. | -.0853582 .0560155 -1.52 0.130 -.1961109 .0253944

w |

--. | -.6078208 .1782055 -3.41 0.001 -.9601647 -.2554769

L1. | .3926237 .1679931 2.34 0.021 .0604714 .7247759

k |

--. | .3568456 .0590203 6.05 0.000 .240152 .4735392

Arellano-Bond dynamic panel-data estimation, two-step difference GMM results

------------------------------------------------------------------------------

| Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

n |

L1. | .6287089 .0904543 6.95 0.000 .4498646 .8075531

L2. | -.0651882 .0265009 -2.46 0.015 -.1175852 -.0127912

w |

--. | -.5257597 .0537692 -9.78 0.000 -.6320709 -.4194485

L1. | .3112899 .0940116 3.31 0.001 .1254122 .4971675

k |

--. | .2783619 .0449083 6.20 0.000 .1895702 .3671537

Arellano-Bond dynamic panel-data estimation, two-step difference GMM results

------------------------------------------------------------------------------

| Corrected

| Coef. Std. Err. t P>|t| [95% Conf. Interval]

-------------+----------------------------------------------------------------

n |

L1. | .6287089 .1934138 3.25 0.001 .2462954 1.011122

L2. | -.0651882 .0450501 -1.45 0.150 -.1542602 .0238838

w |

--. | -.5257597 .1546107 -3.40 0.001 -.8314524 -.2200669

L1. | .3112899 .2030006 1.53 0.127 -.0900784 .7126582

k |

--. | .2783619 .0728019 3.82 0.000 .1344196 .4223043](https://image.slidesharecdn.com/how2doxtabond2-250630154849-b60c9212/75/Cach-s-d-ng-XTABOND2-trong-STATA-v-i-GMM-24-2048.jpg)

![xtabond2

xtabond2 syntax

syntax

xtabond2 depvar varlist [if exp] [in range]

[, level(#) twostep robust noconstant small noleveleq

artests(#) arlevels h(#) nomata]

ivopt [ivopt ...] gmmopt [gmmopt ...]]

where gmmopt is

gmmstyle(varlist [, laglimits(# #) collapse

equation({diff | level | both}) passthru])

and ivopt is

ivstyle(varlist [, equation({diff | level | both})

passthru mz])

Y X Z

Classic

“GMM-style”](https://image.slidesharecdn.com/how2doxtabond2-250630154849-b60c9212/75/Cach-s-d-ng-XTABOND2-trong-STATA-v-i-GMM-27-2048.jpg)