Downloaded 106 times

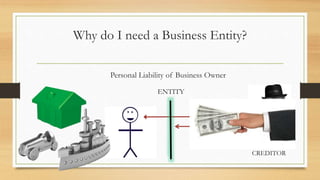

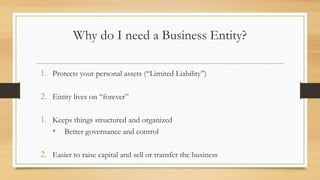

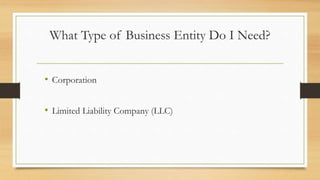

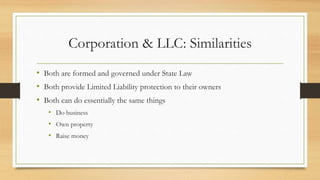

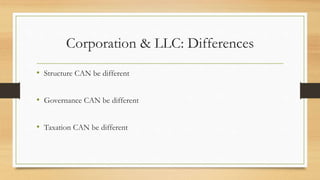

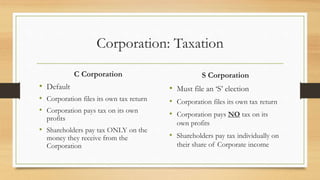

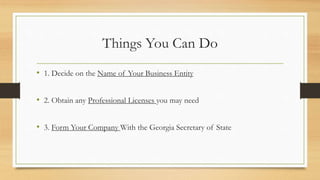

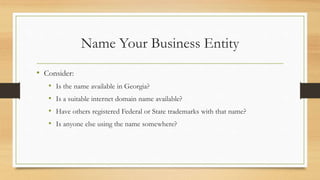

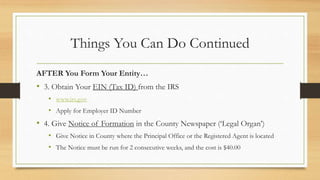

The document presents a comprehensive overview of business formation, focusing on the legal perspectives of establishing a company, including the importance of having a business entity for limited liability and asset protection. It outlines the differences and similarities between corporations and LLCs, their taxation structures, and the necessary steps for forming a business in Georgia. Furthermore, it highlights the significance of obtaining professional assistance for various legal and operational considerations during the setup process.

![The Future Of Education [Publication]](https://cdn.slidesharecdn.com/ss_thumbnails/futureofeducation-091013015209-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)