Download to read offline

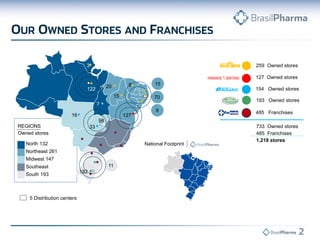

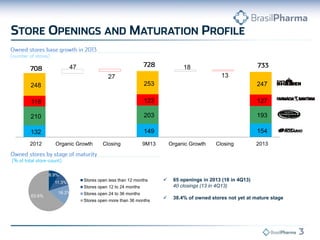

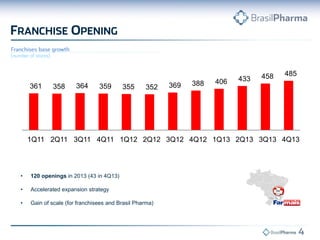

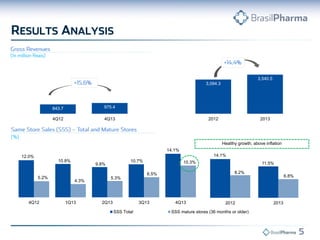

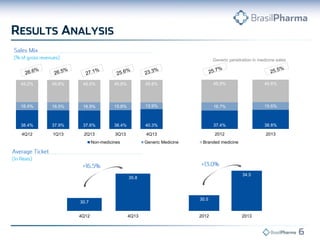

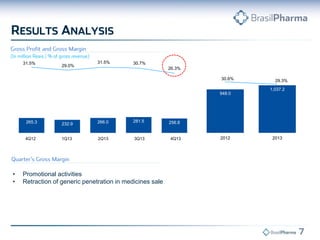

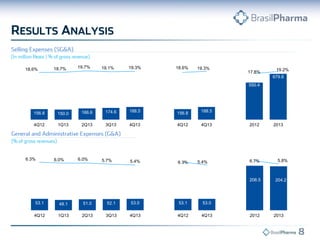

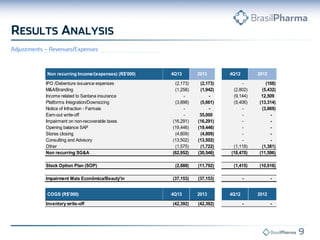

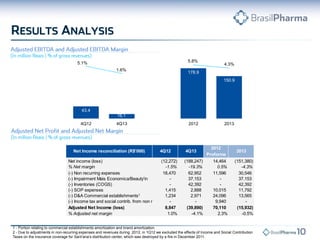

- Brasil Pharma reported gross revenues of R$3.5 billion for full year 2013, an increase of 14.4% over 2012. Gross margin was 27.9% and total same-store sales growth was 11.5%. - Adjusted EBITDA was R$150.9 million with a margin of 4.3%. The company reported an adjusted net loss of R$15.9 million after excluding various one-time expenses. - The company opened 65 new owned stores and 120 franchise stores in 2013, ending the year with a total of 1,218 stores across Brazil.