Slight optimism outshines numerous challenges

As 2016 rolls to a close, the Ukrainian economy is finding stronger footing. The pace of recovery remains slow, but it looks sustainable and the chances of a meaningful acceleration in 2017 are high. Inflation is still in the high single digits, but a hike in regulated utility tariffs should boost it to near the NBU’s 12% target by year-end. The FX market is nearly balanced and the NBU is taking advantage of slight surpluses to replenish reserves. Ukraine’s external accounts look reasonably strong but they still pose a risk to the economy; any external shock could trigger market jitters. Smooth relations with the IMF and other IFIs remain a key precondition for the recovery of investor and domestic consumer confidence.

A Greater Manchester Business Perspective on Post-Referendum UKDuff & Phelps

Duff & Phelps has partnered with the Greater Manchester Chamber of Commerce to conduct a survey to discover how the EU Referendum vote in July has impacted business sentiment in the Greater Manchester region.

So far Sterling and Japanese and European equity markets have borne the brunt of the initial shock, while the FTSE is down only 3.3% since Thursday and most major and emerging market currencies have been reasonably well behaved (see Figure 1).

But there are still far many more questions than answers and the situation remains extremely fluid.

For starters there is no precedent for a country leaving the EU and thus no clear-cut rulebook to rely on. The government has limited institutional capacity to start negotiations with the UK’s 27 EU partners until Article 50 of the Lisbon Treaty is triggered and no timeline has been provided for when this will happen (assuming it is triggered at all).

Perhaps unsurprisingly given the mammoth task ahead, the Leave campaign leaders have been very short on specifics regarding the mechanics and timing of the UK’s exit from the EU, the likely shape of future trade treaties and national policies such as immigration. Prime Minister Cameron’s de-facto resignation and wholesale changes in personnel in the opposition Labour Party are adding to the head-scratching.

Moreover, it is not one country seeking to leave the EU, but a union of four countries – England, Wales, Scotland and Northern Ireland – which further complicates matters as both Scotland and Northern Ireland seem intent on remaining part of the EU and potentially breaking free from the UK.

At this point in time, all we can do is take stock of what we know (or at least we think we know) and what we don’t know (but can tentatively try to forecast).

I would conclude, as I did in Europe – the Final Countdown (21 June 2016), that the many layers of political, legal, economic and financial uncertainty are likely to keep UK investment, consumption and employment, as well as Sterling on the back-foot for months to come. Financial market volatility is also likely to remain elevated in coming weeks.

In this context the US Federal Reserve is likely to keep rates on hold in coming months and the European Central Bank can probably afford to do little for the time being. The Bank of England is likely to seriously contemplate cutting its policy rate while the Bank of Japan will be under renewed pressure to curb soaring Yen strength.

Of course, British policy-makers and business associations have come out and said the right things in order to limit the carnage and contagion. But they have far more limited room to reflate the economy and fade gyrations in financial markets than they did during the 2008-2009 great financial crisis. They are not in control at this juncture and it is not obvious who is.

Post-Recession CEE: Relative Potential Amid The Global RecoveryJustin Patrie

A presentation delivered to the EBRD\'s Eastern European Business Information Conference on the opportunities and risks in post-recession Central and Eastern Europe. Particular emphasis on the global outlook and the relative positioning of individual CEE economies.

Slight optimism outshines numerous challenges

As 2016 rolls to a close, the Ukrainian economy is finding stronger footing. The pace of recovery remains slow, but it looks sustainable and the chances of a meaningful acceleration in 2017 are high. Inflation is still in the high single digits, but a hike in regulated utility tariffs should boost it to near the NBU’s 12% target by year-end. The FX market is nearly balanced and the NBU is taking advantage of slight surpluses to replenish reserves. Ukraine’s external accounts look reasonably strong but they still pose a risk to the economy; any external shock could trigger market jitters. Smooth relations with the IMF and other IFIs remain a key precondition for the recovery of investor and domestic consumer confidence.

A Greater Manchester Business Perspective on Post-Referendum UKDuff & Phelps

Duff & Phelps has partnered with the Greater Manchester Chamber of Commerce to conduct a survey to discover how the EU Referendum vote in July has impacted business sentiment in the Greater Manchester region.

So far Sterling and Japanese and European equity markets have borne the brunt of the initial shock, while the FTSE is down only 3.3% since Thursday and most major and emerging market currencies have been reasonably well behaved (see Figure 1).

But there are still far many more questions than answers and the situation remains extremely fluid.

For starters there is no precedent for a country leaving the EU and thus no clear-cut rulebook to rely on. The government has limited institutional capacity to start negotiations with the UK’s 27 EU partners until Article 50 of the Lisbon Treaty is triggered and no timeline has been provided for when this will happen (assuming it is triggered at all).

Perhaps unsurprisingly given the mammoth task ahead, the Leave campaign leaders have been very short on specifics regarding the mechanics and timing of the UK’s exit from the EU, the likely shape of future trade treaties and national policies such as immigration. Prime Minister Cameron’s de-facto resignation and wholesale changes in personnel in the opposition Labour Party are adding to the head-scratching.

Moreover, it is not one country seeking to leave the EU, but a union of four countries – England, Wales, Scotland and Northern Ireland – which further complicates matters as both Scotland and Northern Ireland seem intent on remaining part of the EU and potentially breaking free from the UK.

At this point in time, all we can do is take stock of what we know (or at least we think we know) and what we don’t know (but can tentatively try to forecast).

I would conclude, as I did in Europe – the Final Countdown (21 June 2016), that the many layers of political, legal, economic and financial uncertainty are likely to keep UK investment, consumption and employment, as well as Sterling on the back-foot for months to come. Financial market volatility is also likely to remain elevated in coming weeks.

In this context the US Federal Reserve is likely to keep rates on hold in coming months and the European Central Bank can probably afford to do little for the time being. The Bank of England is likely to seriously contemplate cutting its policy rate while the Bank of Japan will be under renewed pressure to curb soaring Yen strength.

Of course, British policy-makers and business associations have come out and said the right things in order to limit the carnage and contagion. But they have far more limited room to reflate the economy and fade gyrations in financial markets than they did during the 2008-2009 great financial crisis. They are not in control at this juncture and it is not obvious who is.

Post-Recession CEE: Relative Potential Amid The Global RecoveryJustin Patrie

A presentation delivered to the EBRD\'s Eastern European Business Information Conference on the opportunities and risks in post-recession Central and Eastern Europe. Particular emphasis on the global outlook and the relative positioning of individual CEE economies.

Capitalstars, financial research private limited is a SEBI Registered, provide Stock Tips,Share Market Tips , commodity & currency tips.

http://www.capitalstars.com/tracksheet-stock-tips/

Vietnam Macro and Stock Market Q4 2015

The Biggest Winner From TPP Trade Deal May Be Vietnam, and one of the most attractive Stock markets.

BIDV securrities

BIDV Securities Company (BSC)

Established on November 26th 1999, BIDV Securities Company (BSC) is honor to become one of the first securities firms in Vietnam. Being a subsidiary of the Bank for Investment and Development of Vietnam (BIDV) – one of the largest four State owned Commercial Banks in Vietnam, BSC inherit both the 50 years of experience in investment, banking, finance and the nation-wide network of enterprises . BSC is ranked number one for bond brokerage BSC is ranked top 7 for stock brokerage

Mr Long Tran Thang proud to work for BIDV Securities Company (BSC) as Head of Research and before that as Deputy head of Investment and analyst since 2007. BIDV Securities Company (BSC) is one of the first securities firms in Vietnam. Being a subsidiary of BIDV – the largest commercial Banks in Vietnam, BSC inherit both the 55 years of experience in investment, banking, finance and the nation-wide network of enterprises.

Mr Long Tran Thang earned an MBA from Solvay Brussels School (ULB) in 2014. Mr Long graduated with BA in Economics from the ANU Australian National University (ANU) and BA in Finance from The National Economics University (NEU).

Lekcija: Eirozonas ekonomika un monetārā politika (ENG)Latvijas Banka

Prezentācijā apskatītas šādas tēmas:

Eirozonas ekonomikas aktualitātes.

Eiro zonas monetārās politikas galvenais mērķis – cenu stabilitāte.

Cenu stabilitāte un inflācija.

Monetārās politikas transmisijas mehānisms un Eiropas Centrālās bankas ietekme uz makroekonomiskajiem rādītājiem.

Monetārās politikas praktiskā īstenošana eiro zonā: monetārās politikas īstenošanas pamatprincipi, instrumenti.

SapForex24 recommend Accurate Forex Trading Signals for International Market. So catch out our FOREX and COMEX signal.

Read More:- http://www.sapforex24.com/

From the BPV Capital Management investment team comes our most recent update on capital markets. In this issue, we examine the Brexit vote and global uncertainty and market volatility as a result of that vote.

Bullard Fed US Macroeconomic Outlook 2017AtoZForex.com

St. Louis President and Chief Executive of the Federal Reserve Bank James Bullard addresses the Fed US Macroeconomic Outlook 2017 during an International Distinguished Lecture at the Australian Center for Financial Studies.

During the second quarter of 2016, acquisitive middle-market issuers capitalized on lenders’ increased risk appetite by entering into attractively priced and structured financings. The dramatic rally in Treasury yields (and other safe haven assets) triggered by the “Brexit” referendum at quarter’s end, augurs well for further improvement in domestic credit market conditions.

Economic outlook for 2018 – more bumps in the road?DIXI Group

Macro FI CEE Special Ukraine

After a rather stable 2017, 2018 could become bumpier as elections and debt payments loom in 2019

Relations with foreign partners more strained on limited reform zeal and less patience of partners

Baseline scenario of moderate growth, somewhat weaker UAH and a return to single digit infl ation

No rating and outlook change expected; tight Eurobonds spreads might see a correction in the short run

Capitalstars Financial Research Private Limited(SEBI Registered, CRISIL-NSIC Rated , ISO Certified) is a research house where we provide calls for traders which include tips like Stock Tips, Commodity Tips, MCX Tips, Equity Tips and Intraday Tips also we provide free trials for better Satisfaction.

For More Information Call On 9977499927.

Lekcija: Pasaules tautsaimniecības izaicinājumi un perspektīvasLatvijas Banka

Prezentācija izmantota lekcijā Biznesa augstskola Turība 2016. gada 20. oktobrī.

Pasaules ekonomikas un lielāko pasaules valstu ekonomiku attīstības prognozes, balstoties uz jaunāko Starptautiskā Valūtas fonda veikto analīzi. Prezentācijā apskatīti aktuālie ekonomikas jautājumi un nozīmīgākie attīstību kavējošie riski.

Forex and comex daily report 17 june 16vanessa semos

SapForex24 recommend Accurate Forex Trading Signals for International Market. So catch out our FOREX and COMEX signal.

Read More:- http://www.sapforex24.com/

In the current issue of Economy Matters, we cover the implications of Brexit for Britain and India, update on recent forecasts by World Bank, economic prospects of US economy and European Central Bank’s policy stance in the section on Global Trends. In Domestic Trends, Mr. Ajay Shriram, Past President, CII writes an article on the two years of Modi Government. Additionally, we also analyse the trends emanating out of the recent releases on GDP, IIP, Inflation, Monetary Policy, Trade and Balance of Payments. In Corporate Performance section we examine the corporate profitability trends for firms for the year FY16. From this issue, we have introduced a new section named as Policy Focus, in which we analyse the key policy documents released during the May-June 2016. In Focus of the Month, we cover the topic ‘India’s Trade & International Alliances’.

Dear Investors,

Billionaire investor Wilbur Ross said "Ultimately, I think it will be the world's most expensive divorce. But like most divorces, it's probably going to take a lot longer than it should." The Brexit vote to leave the European Union sent shock waves across the globe. Though the pre-poll surveys had indicated a close call, it was largely expected that sanity would prevail on referendum day and the British populace would vote to Remain. The ramifications of an eventual Brexit are likely to be long-drawn and far-reaching. Apart from the impact it has had on the currency markets, there is an imminent danger of other countries wanting to follow suit. This may lead to the ultimate breakdown of the EU, causing geo-political chaos with the danger of recession.

The equity markets seemed to have temporarily shrugged off the event. While the Sensex tanked by over 1000 points when the Brexit result was declared, it has since recovered all its losses and closed the month of June at a YTD high of almost 27,000. Though there may be individual stocks and sectors where revenues are likely to be directly impacted, the market as a whole has shown significant resilience, waiting as it were for Britain to formally initiate the process of exit before assessing its overall impact.

After the uncertainty of the Brexit verdict got over, the market rallied in the last week. The market got off on the

wrong foot on the day of the Referendum results and corrected by almost 1000 points. But the market soon

realized that the renewal in trade agreement between UK and Euro is not going to happen anytime soon and it will

take around 1-2 years. India being an emerging nation, the impact of this event is quite limited. After this the

market resumed its upt uptrend. Since budget, the nifty is up by 1000 points, and in percentage terms it has gained

22%. We should remember that it is still 10% off of the it’s all time high, which was achieved in March 2015.

• Despite the fact that the PE multiple of the Indian Markets is 17 – 18 times, the FIIs continue to invest in India on

account of better growth prospects, better earning visibility. India is the only trillion dollar economy which is

growing on 7.5%, which makes it a lucrative long term story.

ShenZhen-HongKong Connect - Another milestone achievedNan BAI,CFA

ShenZhen – HongKong Connect program was officially announced on Aug 16th. According to the implementation timetable been released by HKEX, the official launch is scheduled in four months pending further tweaking of the rules and market education and rehearsal.

Capitalstars, financial research private limited is a SEBI Registered, provide Stock Tips,Share Market Tips , commodity & currency tips.

http://www.capitalstars.com/tracksheet-stock-tips/

Vietnam Macro and Stock Market Q4 2015

The Biggest Winner From TPP Trade Deal May Be Vietnam, and one of the most attractive Stock markets.

BIDV securrities

BIDV Securities Company (BSC)

Established on November 26th 1999, BIDV Securities Company (BSC) is honor to become one of the first securities firms in Vietnam. Being a subsidiary of the Bank for Investment and Development of Vietnam (BIDV) – one of the largest four State owned Commercial Banks in Vietnam, BSC inherit both the 50 years of experience in investment, banking, finance and the nation-wide network of enterprises . BSC is ranked number one for bond brokerage BSC is ranked top 7 for stock brokerage

Mr Long Tran Thang proud to work for BIDV Securities Company (BSC) as Head of Research and before that as Deputy head of Investment and analyst since 2007. BIDV Securities Company (BSC) is one of the first securities firms in Vietnam. Being a subsidiary of BIDV – the largest commercial Banks in Vietnam, BSC inherit both the 55 years of experience in investment, banking, finance and the nation-wide network of enterprises.

Mr Long Tran Thang earned an MBA from Solvay Brussels School (ULB) in 2014. Mr Long graduated with BA in Economics from the ANU Australian National University (ANU) and BA in Finance from The National Economics University (NEU).

Lekcija: Eirozonas ekonomika un monetārā politika (ENG)Latvijas Banka

Prezentācijā apskatītas šādas tēmas:

Eirozonas ekonomikas aktualitātes.

Eiro zonas monetārās politikas galvenais mērķis – cenu stabilitāte.

Cenu stabilitāte un inflācija.

Monetārās politikas transmisijas mehānisms un Eiropas Centrālās bankas ietekme uz makroekonomiskajiem rādītājiem.

Monetārās politikas praktiskā īstenošana eiro zonā: monetārās politikas īstenošanas pamatprincipi, instrumenti.

SapForex24 recommend Accurate Forex Trading Signals for International Market. So catch out our FOREX and COMEX signal.

Read More:- http://www.sapforex24.com/

From the BPV Capital Management investment team comes our most recent update on capital markets. In this issue, we examine the Brexit vote and global uncertainty and market volatility as a result of that vote.

Bullard Fed US Macroeconomic Outlook 2017AtoZForex.com

St. Louis President and Chief Executive of the Federal Reserve Bank James Bullard addresses the Fed US Macroeconomic Outlook 2017 during an International Distinguished Lecture at the Australian Center for Financial Studies.

During the second quarter of 2016, acquisitive middle-market issuers capitalized on lenders’ increased risk appetite by entering into attractively priced and structured financings. The dramatic rally in Treasury yields (and other safe haven assets) triggered by the “Brexit” referendum at quarter’s end, augurs well for further improvement in domestic credit market conditions.

Economic outlook for 2018 – more bumps in the road?DIXI Group

Macro FI CEE Special Ukraine

After a rather stable 2017, 2018 could become bumpier as elections and debt payments loom in 2019

Relations with foreign partners more strained on limited reform zeal and less patience of partners

Baseline scenario of moderate growth, somewhat weaker UAH and a return to single digit infl ation

No rating and outlook change expected; tight Eurobonds spreads might see a correction in the short run

Capitalstars Financial Research Private Limited(SEBI Registered, CRISIL-NSIC Rated , ISO Certified) is a research house where we provide calls for traders which include tips like Stock Tips, Commodity Tips, MCX Tips, Equity Tips and Intraday Tips also we provide free trials for better Satisfaction.

For More Information Call On 9977499927.

Lekcija: Pasaules tautsaimniecības izaicinājumi un perspektīvasLatvijas Banka

Prezentācija izmantota lekcijā Biznesa augstskola Turība 2016. gada 20. oktobrī.

Pasaules ekonomikas un lielāko pasaules valstu ekonomiku attīstības prognozes, balstoties uz jaunāko Starptautiskā Valūtas fonda veikto analīzi. Prezentācijā apskatīti aktuālie ekonomikas jautājumi un nozīmīgākie attīstību kavējošie riski.

Forex and comex daily report 17 june 16vanessa semos

SapForex24 recommend Accurate Forex Trading Signals for International Market. So catch out our FOREX and COMEX signal.

Read More:- http://www.sapforex24.com/

In the current issue of Economy Matters, we cover the implications of Brexit for Britain and India, update on recent forecasts by World Bank, economic prospects of US economy and European Central Bank’s policy stance in the section on Global Trends. In Domestic Trends, Mr. Ajay Shriram, Past President, CII writes an article on the two years of Modi Government. Additionally, we also analyse the trends emanating out of the recent releases on GDP, IIP, Inflation, Monetary Policy, Trade and Balance of Payments. In Corporate Performance section we examine the corporate profitability trends for firms for the year FY16. From this issue, we have introduced a new section named as Policy Focus, in which we analyse the key policy documents released during the May-June 2016. In Focus of the Month, we cover the topic ‘India’s Trade & International Alliances’.

Dear Investors,

Billionaire investor Wilbur Ross said "Ultimately, I think it will be the world's most expensive divorce. But like most divorces, it's probably going to take a lot longer than it should." The Brexit vote to leave the European Union sent shock waves across the globe. Though the pre-poll surveys had indicated a close call, it was largely expected that sanity would prevail on referendum day and the British populace would vote to Remain. The ramifications of an eventual Brexit are likely to be long-drawn and far-reaching. Apart from the impact it has had on the currency markets, there is an imminent danger of other countries wanting to follow suit. This may lead to the ultimate breakdown of the EU, causing geo-political chaos with the danger of recession.

The equity markets seemed to have temporarily shrugged off the event. While the Sensex tanked by over 1000 points when the Brexit result was declared, it has since recovered all its losses and closed the month of June at a YTD high of almost 27,000. Though there may be individual stocks and sectors where revenues are likely to be directly impacted, the market as a whole has shown significant resilience, waiting as it were for Britain to formally initiate the process of exit before assessing its overall impact.

After the uncertainty of the Brexit verdict got over, the market rallied in the last week. The market got off on the

wrong foot on the day of the Referendum results and corrected by almost 1000 points. But the market soon

realized that the renewal in trade agreement between UK and Euro is not going to happen anytime soon and it will

take around 1-2 years. India being an emerging nation, the impact of this event is quite limited. After this the

market resumed its upt uptrend. Since budget, the nifty is up by 1000 points, and in percentage terms it has gained

22%. We should remember that it is still 10% off of the it’s all time high, which was achieved in March 2015.

• Despite the fact that the PE multiple of the Indian Markets is 17 – 18 times, the FIIs continue to invest in India on

account of better growth prospects, better earning visibility. India is the only trillion dollar economy which is

growing on 7.5%, which makes it a lucrative long term story.

ShenZhen-HongKong Connect - Another milestone achievedNan BAI,CFA

ShenZhen – HongKong Connect program was officially announced on Aug 16th. According to the implementation timetable been released by HKEX, the official launch is scheduled in four months pending further tweaking of the rules and market education and rehearsal.

Stephany Cuevas, EdM Presentation at 2016 Science of HOPE

In this session, participants will be introduced to family and community engagement research in order to begin to interrogate why we need to partner with families and communities in service work.

Participants will be exposed to different narratives and perspectives about families and communities and will be engaged in conversations about how to push beyond deficit thinking and stereotypes, which often deter partnership opportunities. Additionally, participants will be introduced to frameworks, including research-based best practices, which allow us to understand how to do partnership work in a mutually benefiting and respectful matter.

Presented by Michelle Di Miscio, MSW, Andrea Lopez–Diaz, Vicky Navarro, Angeles Solis at the 2016 Science of HOPE.

Description:

Social Connections are all about the bonds we make and keep in our communities.

The more connected we are the healthier we are. Research shows positive social connection has a direct impact on our health. Positive social bonds are associated with lower blood pressure, stronger immunity, decreased risk of chronic disease and increased resilience. This is especially important for advancing equity in our communities.

This workshop invites you to recognize and rely on social connection as a strength.

In the spirit of popular education, we believe you bring the wisdom, and we learn in community.

You will walk away having had the opportunity to share stories, lessons learned, and make valuable connections.

This workshop was designed in partnership with members of the King County Promotores Network: a 250+ member network composed of community members, service providers and systems representatives serving communities of color, immigrant, migrant and refugee populations in King County.

In this special edition of Valuation Insights, we discuss some of the key valuation and compliance impacts that will likely result from Brexit. Specifically, we review the short-term and long-term economic implications, as well as compliance and regulatory considerations. We also highlight valuation issues, including how companies and investors determine cost of capital and measure risk in the current environment, and discuss implications for transfer pricing with respect to EU Directives. While all industries will be impacted by Brexit, in this issue we focus on the banking and financial services sectors, which stand to be the most heavily affected.

Capital-Infraestructure-spending-outlook-2016PwC España

El Informe "Capital Project and Infraestructure Spending Outlook" de PwC estima que en 2016 la inversión mundial en infraestructuras aumente un 2%. A partir de 2017, se espera que este ritmo se acelere paulatinamente hasta alcanzar una inversión total, en 2020, de 28,3 billones de dólares.

The EU Referendum: The Future of the UK and Europe - Third Edition - July 2016Ewan Kinnear

The EU Referendum - the Future of the UK and Europe. Lloyds Banking Group has prepared this fact based and objective document to help inform about the technical and mechanical aspects around the various models for a future UK-EU relationship and what happens next.

The global economy remains fragile going into 2023. There are possibilities of mild recession and stagflation in some economies. Deloitte 2023 Banking & Capital Markets Outlook shares comprehensive overview insights into the Banking and Capital market segments. Uncover about Retail Banking: Envisioning new ways to serve and engage with customers, Consumer Payments- build deeper financial relationships beyond transaction flows.

The quarterly CFO Survey is firmly established with media and policy makers as the authoritative barometer of UK corporates’ sentiment and strategies. It is the only survey of major corporate users of capital that gauges attitudes to valuations, risk and financing.

Emerging Capital Markets: The Road to 2030Credit Suisse

1/2014

For the most part, emerging nation capital markets remain underdeveloped relative to the size of their economies, despite rapid growth in capital-raising over the past two decades. We believe this gap will close, driven by a disproportionately large contribution from emerging equity and corporate bond supply and demand, given relatively high savings ratios prevalent among emerging economies.

In this proprietary study, we extrapolate established historical patterns of growth in emerging and developed capital markets to assist in projecting their absolute and relative dimension and composition of market value by the year 2030.

China bond inclusion in Citi bond indiciesNan BAI,CFA

Citi just announced the inclusion of Chinese bond in three of its indices: the Emerging Markets Government Bond Index (EMGBI), Asian Government Bond Index (AGBI), and the Asia Pacific Government Bond Index (APGBI).

The global high yield bond markets have witnessed sentiment to risk-off mode. This has since been partially significant growth and diversification over the last few years aided by the extraordinary monetary policy accommodation provided by central banks across the world. The unprecedented liquidity made available at record low yields has thus led to a significant pick up in both primary market and secondary market activity in the asset class. Banking disintermediation in Europe and regulatory changes in the financial sector further contributed to the deepening and diversification of the high yield bond markets even as emerging market issuances entered the fray.

In this backdrop, Aranca’s special report – High Yield Bonds - The Rise of the Fallen – examines how liquidity concerns have increased with changing regulatory environment, rising capital requirements and declining risk appetite leading to decreasing bond inventories at both banks and other dealers even as corporate bond issuances are at an all-time high.

If you are looking for a pi coin investor. Then look no further because I have the right one he is a pi vendor (he buy and resell to whales in China). I met him on a crypto conference and ever since I and my friends have sold more than 10k pi coins to him And he bought all and still want more. I will drop his telegram handle below just send him a message.

@Pi_vendor_247

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

Exploring Abhay Bhutada’s Views After Poonawalla Fincorp’s Collaboration With...beulahfernandes8

The financial landscape in India has witnessed a significant development with the recent collaboration between Poonawalla Fincorp and IndusInd Bank.

The launch of the co-branded credit card, the IndusInd Bank Poonawalla Fincorp eLITE RuPay Platinum Credit Card, marks a major milestone for both entities.

This strategic move aims to redefine and elevate the banking experience for customers.

how to sell pi coins in all Africa Countries.DOT TECH

Yes. You can sell your pi network for other cryptocurrencies like Bitcoin, usdt , Ethereum and other currencies And this is done easily with the help from a pi merchant.

What is a pi merchant ?

Since pi is not launched yet in any exchange. The only way you can sell right now is through merchants.

A verified Pi merchant is someone who buys pi network coins from miners and resell them to investors looking forward to hold massive quantities of pi coins before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

what is the best method to sell pi coins in 2024DOT TECH

The best way to sell your pi coins safely is trading with an exchange..but since pi is not launched in any exchange, and second option is through a VERIFIED pi merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and pioneers and resell them to Investors looking forward to hold massive amounts before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade pi coins with.

@Pi_vendor_247

Currently pi network is not tradable on binance or any other exchange because we are still in the enclosed mainnet.

Right now the only way to sell pi coins is by trading with a verified merchant.

What is a pi merchant?

A pi merchant is someone verified by pi network team and allowed to barter pi coins for goods and services.

Since pi network is not doing any pre-sale The only way exchanges like binance/huobi or crypto whales can get pi is by buying from miners. And a merchant stands in between the exchanges and the miners.

I will leave the telegram contact of my personal pi merchant. I and my friends has traded more than 6000pi coins successfully

Tele-gram

@Pi_vendor_247

Introduction to Indian Financial System ()Avanish Goel

The financial system of a country is an important tool for economic development of the country, as it helps in creation of wealth by linking savings with investments.

It facilitates the flow of funds form the households (savers) to business firms (investors) to aid in wealth creation and development of both the parties

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

USDA Loans in California: A Comprehensive Overview.pptxmarketing367770

USDA Loans in California: A Comprehensive Overview

If you're dreaming of owning a home in California's rural or suburban areas, a USDA loan might be the perfect solution. The U.S. Department of Agriculture (USDA) offers these loans to help low-to-moderate-income individuals and families achieve homeownership.

Key Features of USDA Loans:

Zero Down Payment: USDA loans require no down payment, making homeownership more accessible.

Competitive Interest Rates: These loans often come with lower interest rates compared to conventional loans.

Flexible Credit Requirements: USDA loans have more lenient credit score requirements, helping those with less-than-perfect credit.

Guaranteed Loan Program: The USDA guarantees a portion of the loan, reducing risk for lenders and expanding borrowing options.

Eligibility Criteria:

Location: The property must be located in a USDA-designated rural or suburban area. Many areas in California qualify.

Income Limits: Applicants must meet income guidelines, which vary by region and household size.

Primary Residence: The home must be used as the borrower's primary residence.

Application Process:

Find a USDA-Approved Lender: Not all lenders offer USDA loans, so it's essential to choose one approved by the USDA.

Pre-Qualification: Determine your eligibility and the amount you can borrow.

Property Search: Look for properties in eligible rural or suburban areas.

Loan Application: Submit your application, including financial and personal information.

Processing and Approval: The lender and USDA will review your application. If approved, you can proceed to closing.

USDA loans are an excellent option for those looking to buy a home in California's rural and suburban areas. With no down payment and flexible requirements, these loans make homeownership more attainable for many families. Explore your eligibility today and take the first step toward owning your dream home.

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

1. June 30 , 2016

1 / 4

BREXIT on China

The aftermath of the UK’s EU Referendum

Background

UK 52% to 48% vote to leave the EU marked a major set-back of globalization. It even hinted rising populism

globally and could have huge impact on geo-political landscape both in the EU and across the Atlantic.

Though less direct, BREXIT’simplication on China could be complicated and for years to come, namely in the

following three facets.

China Macro

RMB

Domestic Capital Markets

China Marco

China being one of the biggest beneficiaries of globalization in the past few decades may be hurt in terms of

export and investment once globalization were to be put in the reverse gear. Precedents from the EU

financial crisis in 2011-2012 point to immediate negative impact on export and GDP growth as well as

longer-term and more severe damages as the contagion spreads. (Exhibit 1)

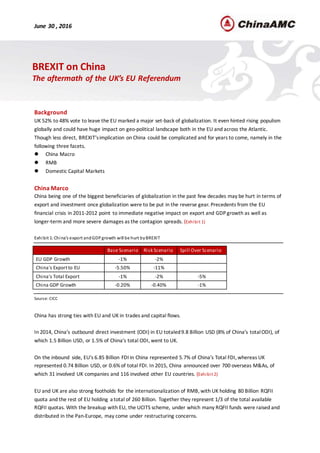

Exhibit 1:China’s export andGDPgrowth will be hurt byBREXIT

Source: CICC

China has strong ties with EU and UK in trades and capital flows.

In 2014, China’s outbound direct investment (ODI) in EU totaled9.8 Billion USD (8% of China’s totalODI), of

which 1.5 Billion USD, or 1.5% of China’s total ODI, went to UK.

On the inbound side, EU’s 6.85 Billion FDI in China represented 5.7% of China’s Total FDI, whereas UK

represented 0.74 Billion USD, or 0.6% of total FDI. In 2015, China announced over 700 overseas M&As, of

which 31 involved UK companies and 116 involved other EU countries. (Exhibit 2)

EU and UK are also strong footholds for the internationalization of RMB, with UK holding 80 Billion RQFII

quota and the rest of EU holding a total of 260 Billion. Together they represent 1/3 of the total available

RQFII quotas. With the breakup with EU, the UCITS scheme, under which many RQFII funds were raised and

distributed in the Pan-Europe, may come under restructuring concerns.

Base Scenario Risk Scenario Spill Over Scenario

EU GDP Growth -1% -2%

China's Exportto EU -5.50% -11%

China's Total Export -1% -2% -5%

China GDP Growth -0.20% -0.40% -1%

2. 2 / 4

Exhibit2:China’s investment ties withEU andUKare strong

Source: CICC

RMB

In longer term, the BREXIT result and the consequent British and EU economy deterioration could trigger

another round of liquidity supply in Europe and even outside the continent, and the potential US Fed rate

hike could also be delayed. (Exhibit 3) This could significantly ease the pressure of RMB depreciation in the

longer term, making China less worried about imported inflation and therefore giving its central bank more

room for monetary stimulation.

Exhibit 3:Probabilityof US rate hike collapsed

Source: Haitong Securities

Exhibit 4:RMB performance on Jun 24th

Source: CICC

In the short term, the sharp devaluation of GBP and EUR boosted USD index by 3.5%. RMB, which is

declared to be pegged to a basket of major currencies, had fared steady on June 24th, except for against USD

and JPY. (Exhibit 4) The rise of the USD index gives the PBoC an excuse to slightly depreciate RMB against USD,

as is evidenced by the offshore USD/RMB jump from 6.58 to 6.68 in two days.

Domestic Capital Markets

BREXIT ‘s impact on China’s domestic market is mixed coupled with a great level of uncertainty. The only

certainty among all is the elevated risk aversion in the short term, which will boost the domestic bond

market as investors takerefuge.

Rising expectation for accommodative fiscal as well as monetary policies to weather expected external

3. 3 / 4

shocks is also benefiting the bond market at least in the short term. However, with the domestic yields

already quite low and out of fear of putting additional pressure on the currency, the medium-term picture

of the bond market is a bit vague at this moment.

On the equity side, domestic risk aversion sentiment went full-blown on the day of the BREXIT, yet it

seemed to be short-lived. The Shanghai Composite index since then went on a four-day rising streak,

reflecting the spooked domestic investors finding comfort in their home markets. (Exhibit 5)

Exhibit 5: SHCOMPPerformance (Jun22-30)

Source: Wind, ChinaAMC

The strategy we have been implementing so far this year has focused on value and consistency between

valuation and earnings growth. With this philosophy, we believe that the downside risk is well managed

even after the shock of BREXIT.

We will overweight stocks with steady performance and visible prospects in the future, such as Consumer

Staples, and will keep performance of current portfolio holdings in close check, and will cut underperformed

positions as we see fit.

We still see structural opportunities existing in the A-share market and will keep looking for investment

opportunities in the emerging industries, including semiconductor and new-energy vehicles. In cases of a

market correction, we will view it as an opportunity to pick up additional names whose valuations are in our

comfort zone.

2800

2820

2840

2860

2880

2900

2920

2940

2960

2016-06-22

2016-06-22

2016-06-22

2016-06-22

2016-06-22

2016-06-22

2016-06-22

2016-06-23

2016-06-23

2016-06-23

2016-06-23

2016-06-23

2016-06-23

2016-06-24

2016-06-24

2016-06-24

2016-06-24

2016-06-24

2016-06-24

2016-06-27

2016-06-27

2016-06-27

2016-06-27

2016-06-27

2016-06-27

2016-06-28

2016-06-28

2016-06-28

2016-06-28

2016-06-28

2016-06-28

2016-06-28

2016-06-29

2016-06-29

2016-06-29

2016-06-29

2016-06-29

2016-06-29

2016-06-30

2016-06-30

2016-06-30

2016-06-30

2016-06-30

2016-06-30

4. 4 / 4

Disclaimer

Important Information

This report is intended only for the use of our clients and prospects. Neither this report nor any of its contents may

be reproduced or published for any other purpose without the prior written consent of China Asset Management Co.

Ltd (“ChinaAMC” ). All the investment strategy illustrated in this report was made on a preliminary basis only, no

representation or warranty is made as to the efficacy of any particular strategy or the actual returns that may be

achieved.

The information in this report reflects prevailing market conditions and our judgment as of this date, which are subject

to change. In preparing this report, we have relied upon and assumed without independent verification, the accuracy

and completeness of all information available from public sources. We consider the information in this report to be

reliable, but we do not represent that it is complete or accurate. ChinaAMC, its affiliates, directors, officers or

employees accept no liability for any errors or omissions relating to information available in this report, and will not be

liable for any damages or costs arising out of or in any way connected with the use of the information provided in this

report.

Any information given or representation made by any dealer, salesman or other person and (in either case) not

contained herein should be regarded as unauthorized and, accordingly, should not be relied upon. Accordingly, no

person receiving a copy of this report in any territory may treat the same as constituting an invitation to him to

purchase or subscribe for the participating shares of the Fund nor should he in any event use the Fund’s subs cription

agreement unless in the relevant jurisdiction such invitation and distribution islawfully made.

Contact Information

China Asset Management Co. Ltd.

8F, Tower 7, One Yuetan Street South, Xicheng District, Beijing100045, China

IB@ChinaAMC.com

Tel:+86 10 8806 6688/ Fax:+86 10 8806 6330