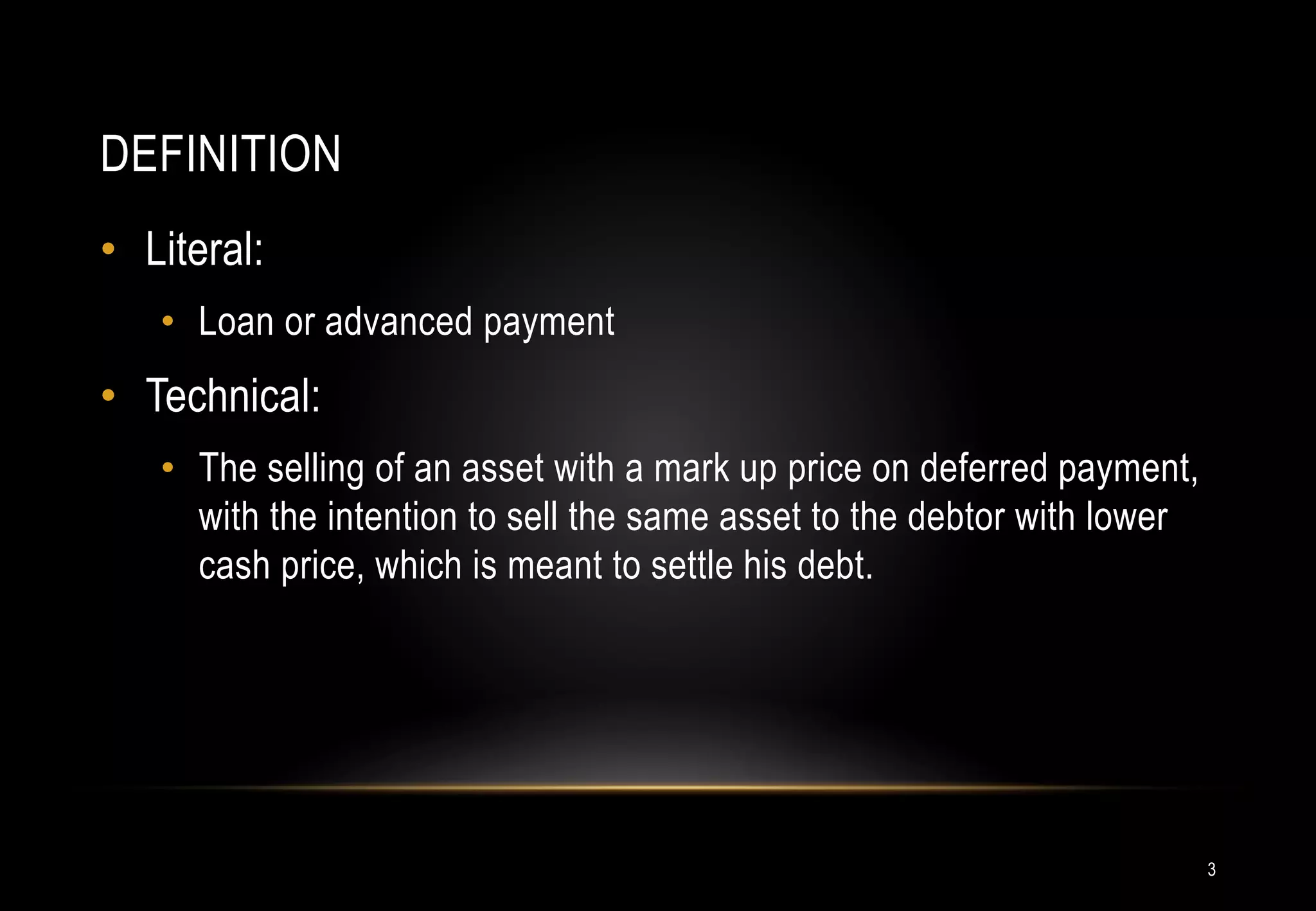

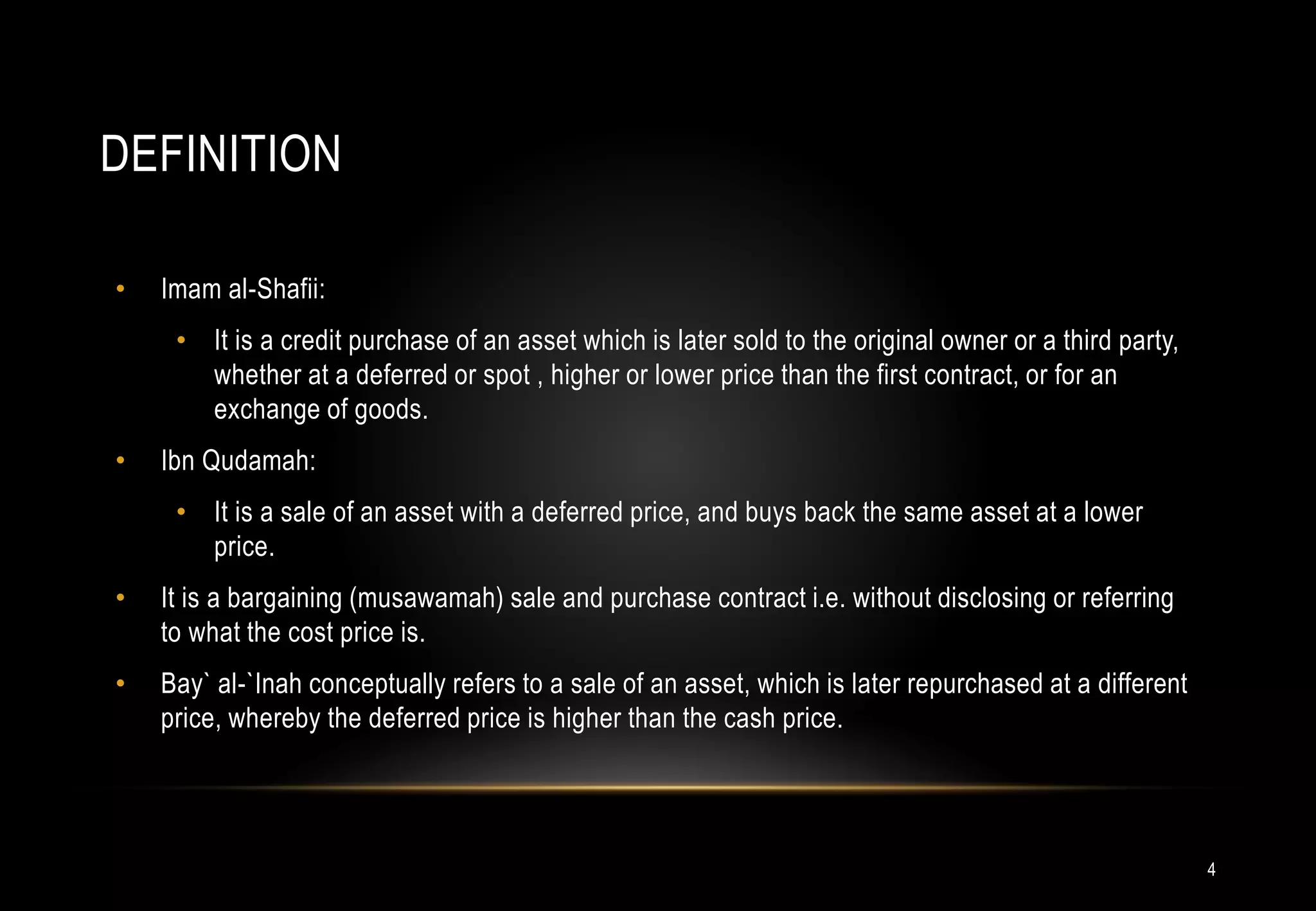

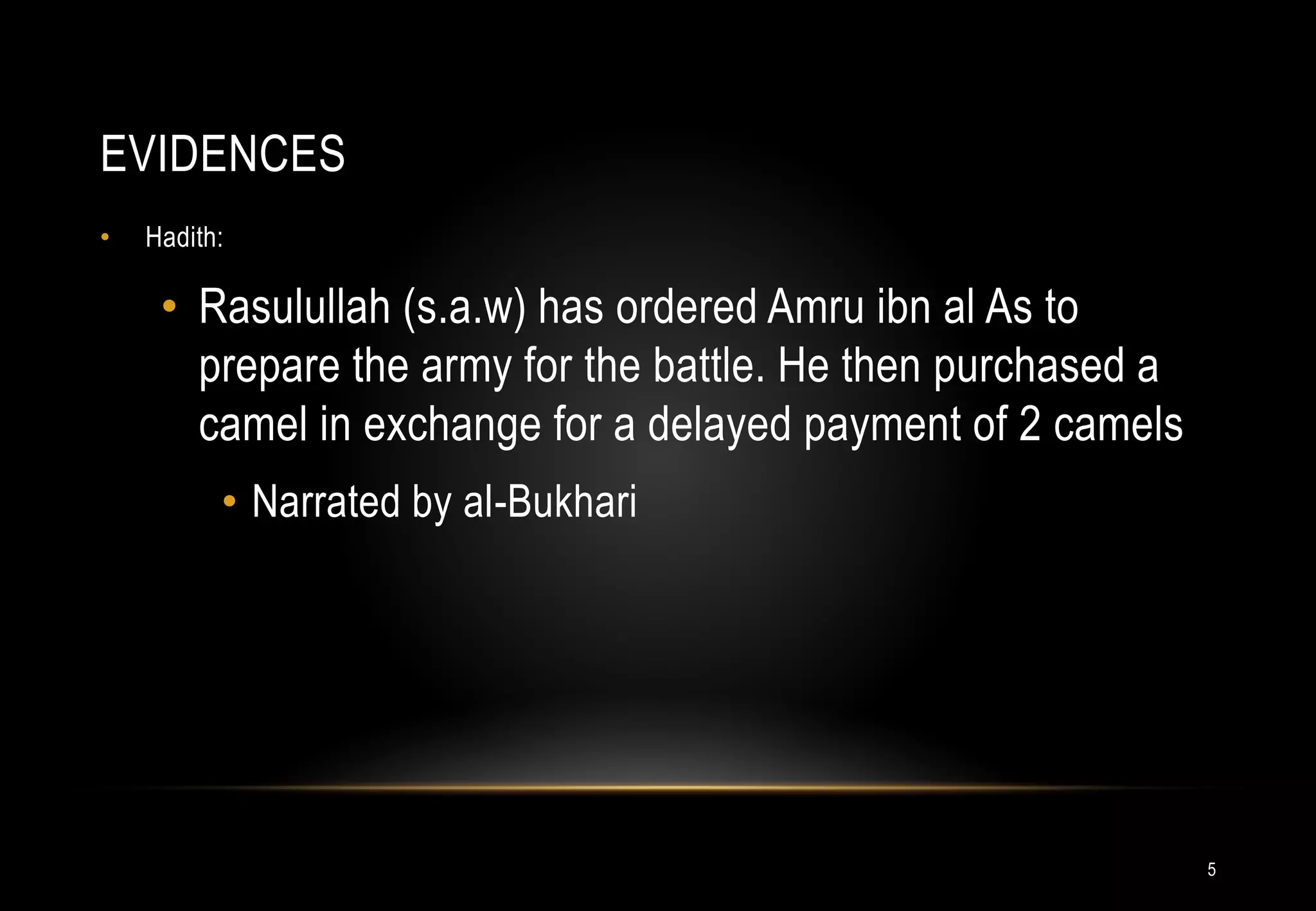

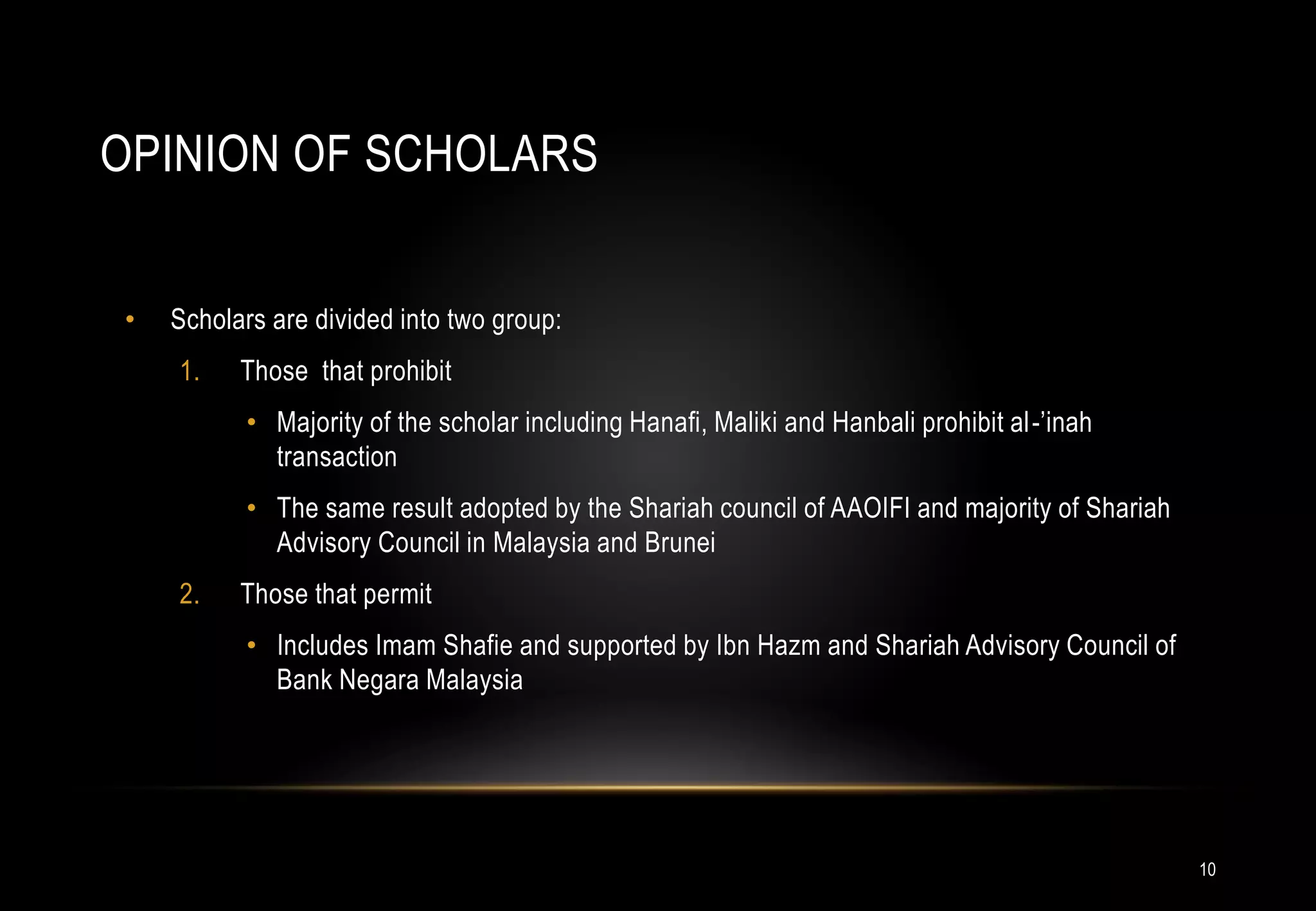

Bay al-Inah is a sale contract where an asset is sold with deferred payment at a higher price, and then the seller repurchases the same asset back from the buyer for a lower cash price. Scholars are divided, with the majority prohibiting it as a means to circumvent riba. Supporters argue it follows the rules of a valid sale contract. Modern applications include using it as the basis for various Islamic financing products in Malaysia, provided certain conditions are met.