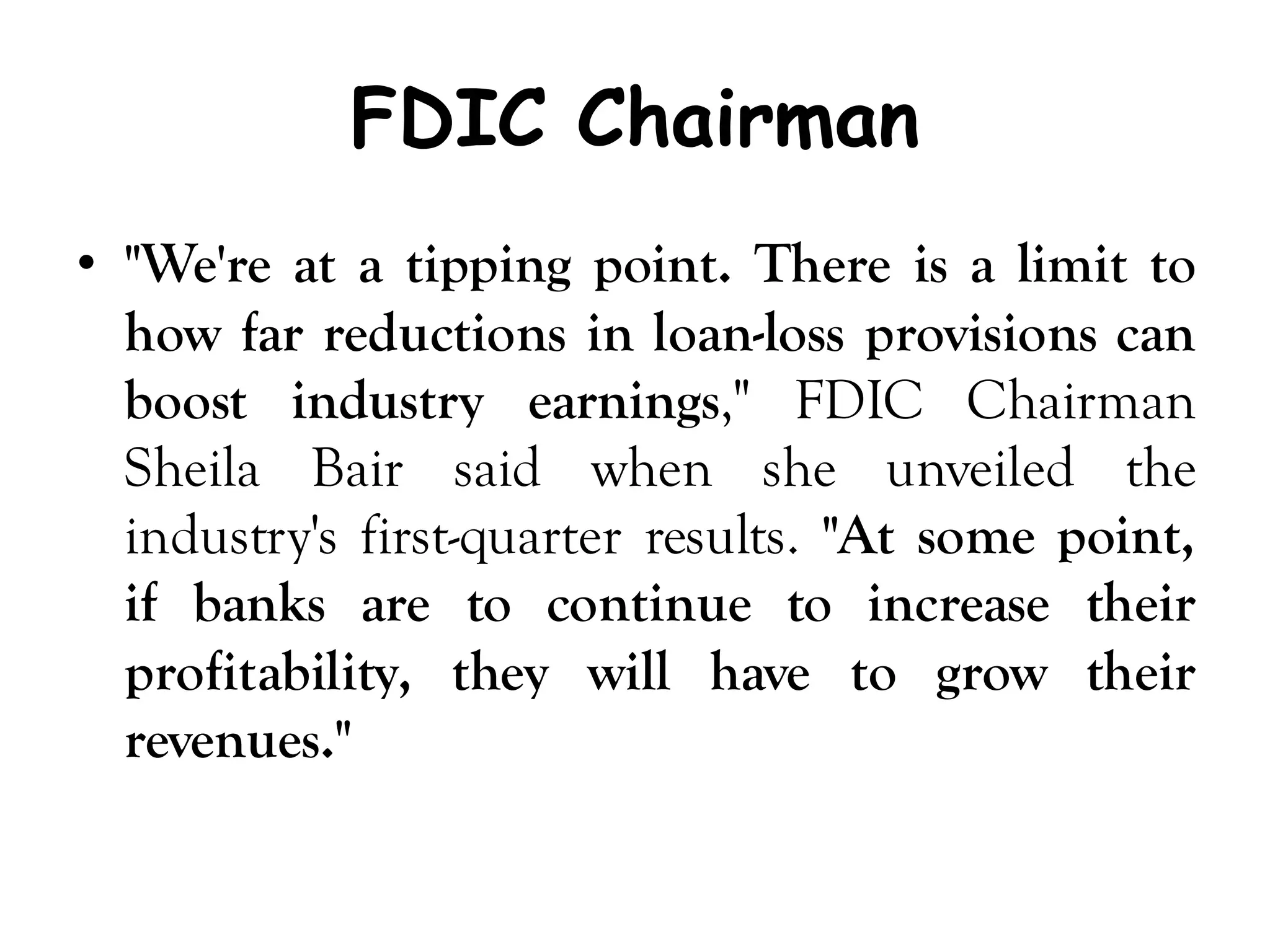

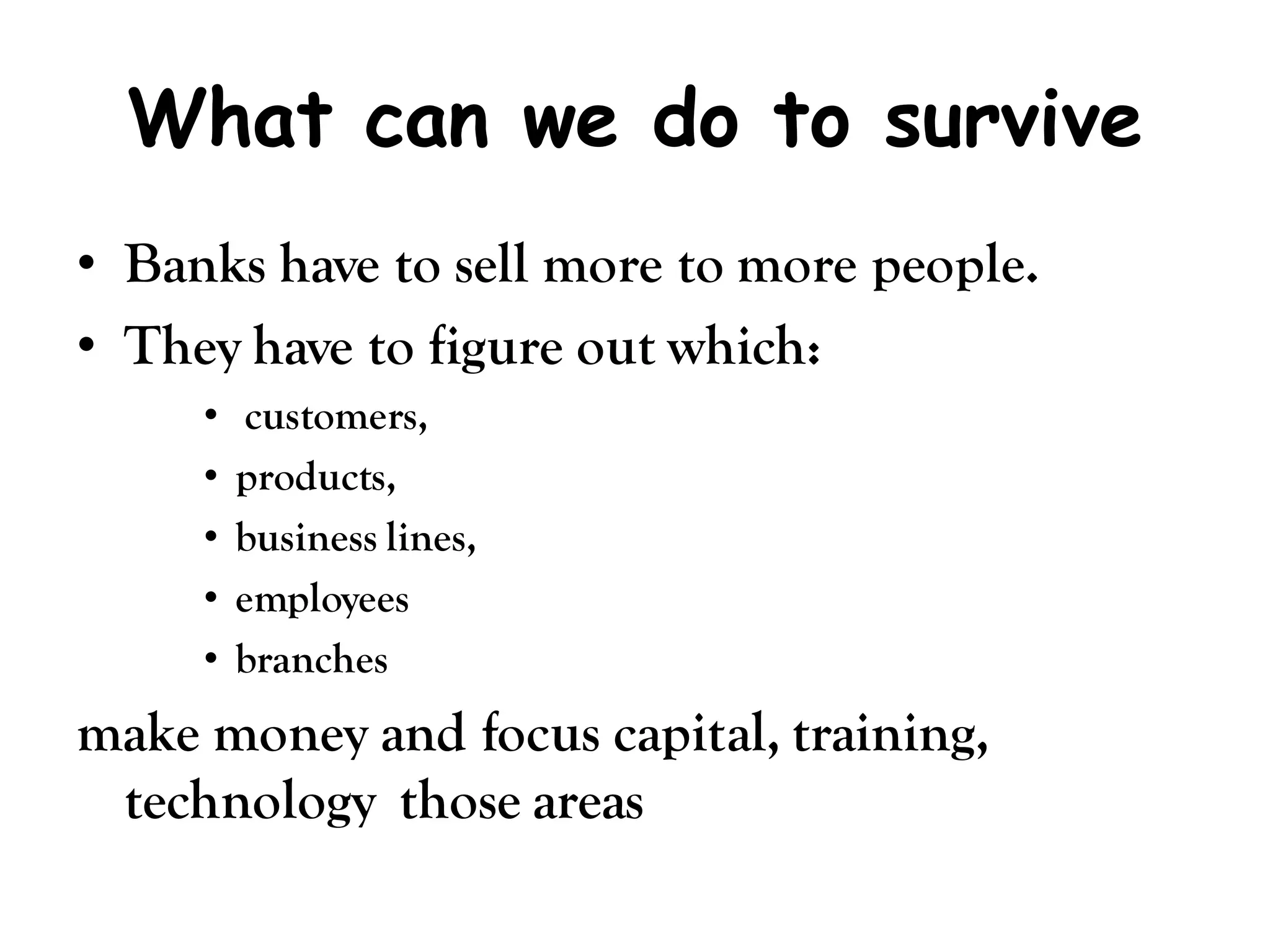

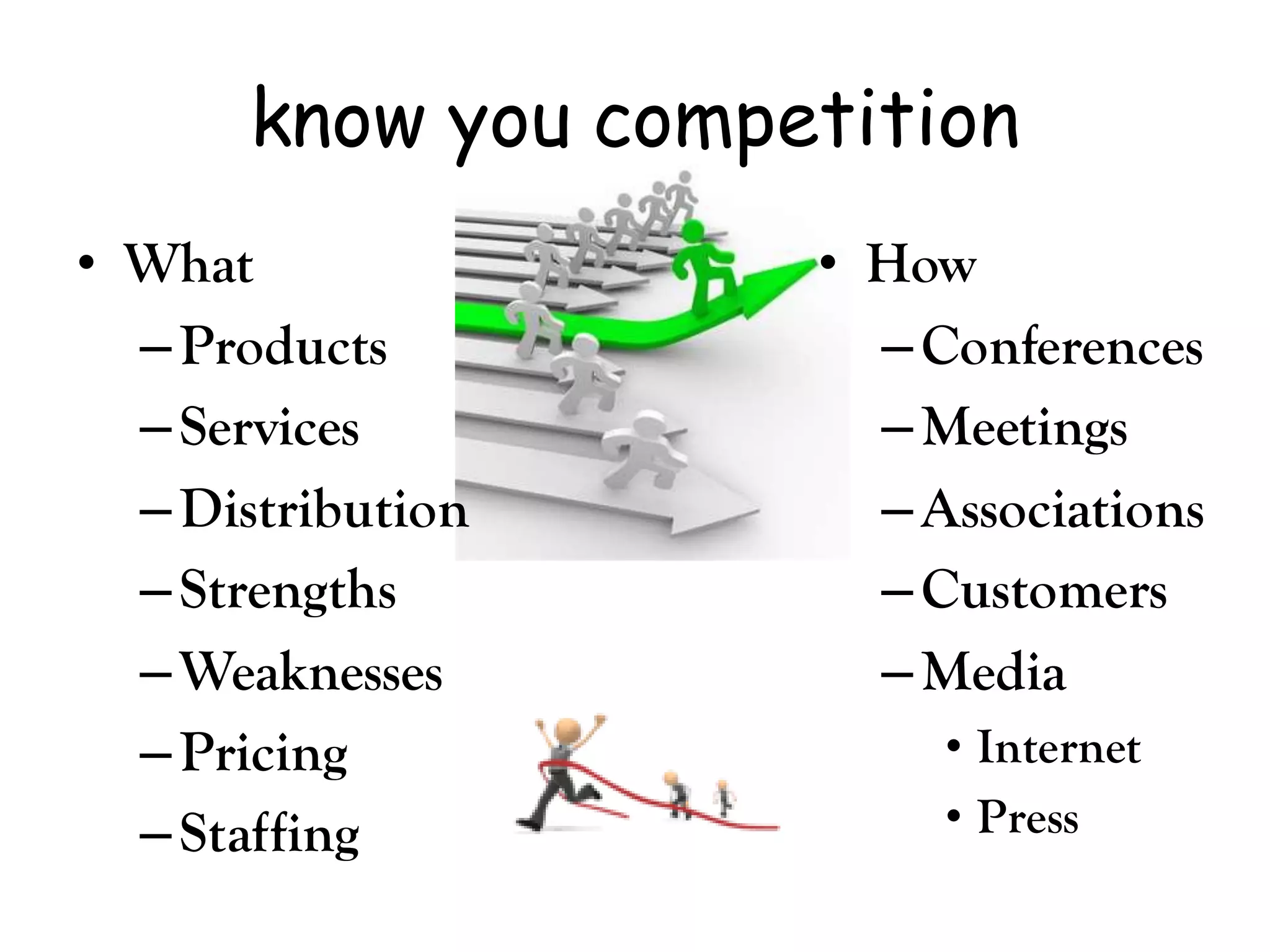

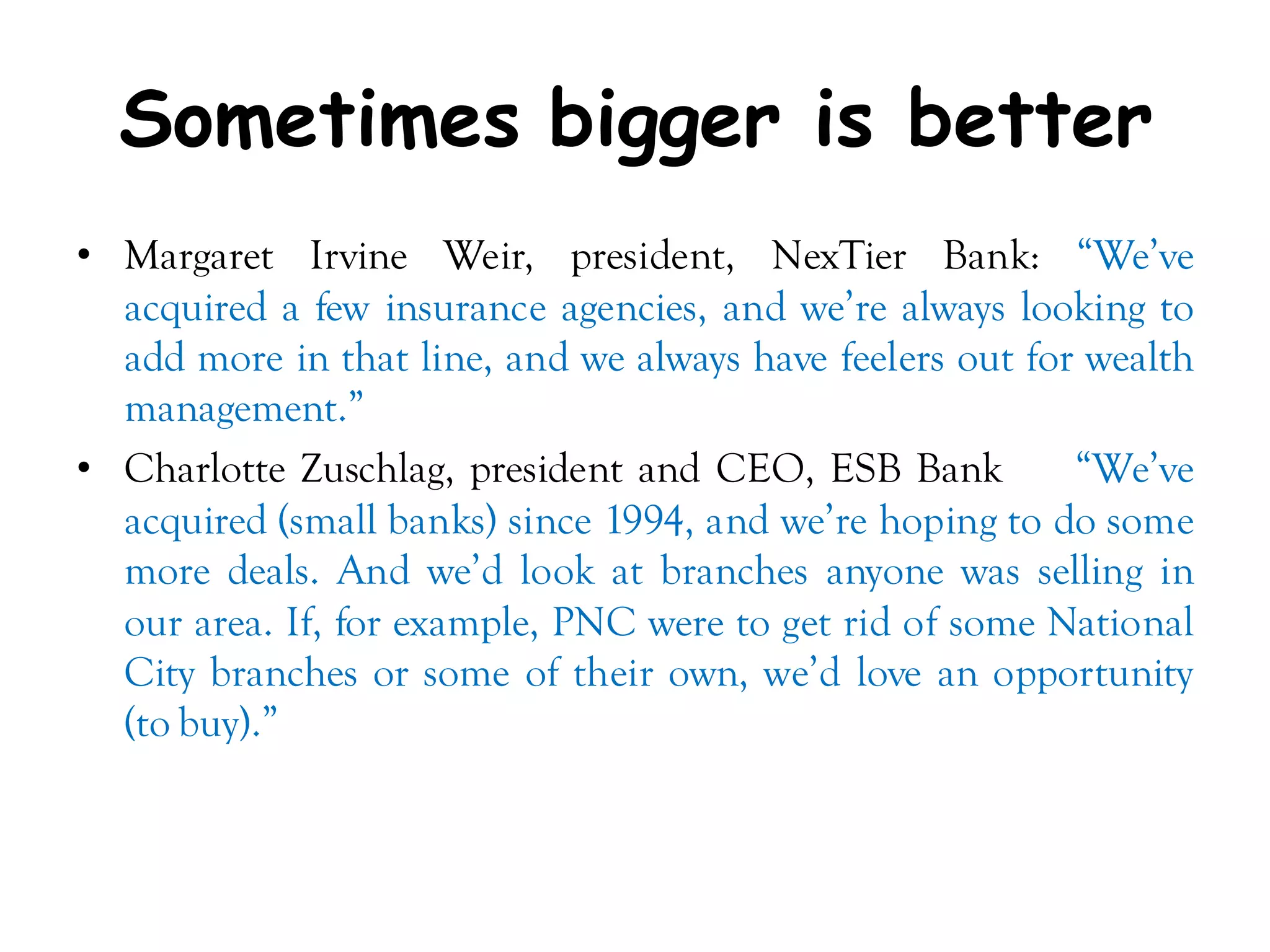

The document discusses strategies for banks to increase revenue in challenging economic environments. It recommends focusing on cross-selling additional products to existing customers, leveraging branch networks as distribution points, expanding small business lending, and using customer credit data to identify other opportunities. The document also suggests that mergers or acquisitions may be necessary for some banks to achieve necessary scale, expand into new markets, and diversify their business lines in order to survive difficult conditions.