Downloaded 15 times

![Capital Markets Overview

Markets – A place where exchange of goods and services happen

Capital Market

•Place where capital (fund) requirements of the issuers are

met; i.e. Issuers (Corporate, Government, etc) raise funds

•Trades in these markets are for debt, equity securities or

other instruments

•Organized, as they are governed by regulatory bodies

[Securities & Exchange Board of India, RBI]

11](https://image.slidesharecdn.com/bankingpresentation-120917055601-phpapp02/85/Banking-presentation-11-320.jpg)

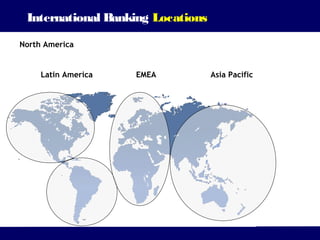

![Products: Derivatives

FX Option

Big company now have the right to use [exercise] this trade for settlement on March 7th

What are the key dates?

The FX Option Expiry Date:

Buyer: Big Company

Date that Big Company have to decide whether to exercise the Option

Seller: JPMorgan

Delivery Date:

FX Option Details Date that transfer of funds would occur if Big Company Ltd

exercise this Option

Call: GBP: 1,000,000

Put: USD: 1,500,000

Strike Price 1.5 Other FX Option Components

Expiry Date 5th March 2004

Delivery date 7th March 2004 Call:

Currency that the buyer of the Option would receive

Premium: $5000 Put:

Currency that the buyer of the Option would sell

Strike:

Exchange Rate that would be used if Option is exercised

Page 45-49 in Workbook

67](https://image.slidesharecdn.com/bankingpresentation-120917055601-phpapp02/85/Banking-presentation-67-320.jpg)

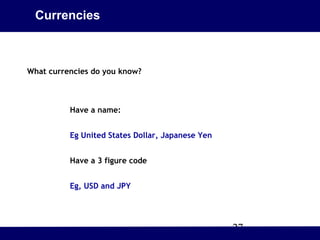

![Products: Derivatives

FX Option

How do Big company know whether to exercise the Option?

On 5th March

The FX Option

Buyer: Big Company

Seller: JPMorgan • Look at current FX [Spot] rate

FX Option Details

Call: GBP: 1,000,000 • If they used the spot rate (Not the Option Strike rate)

Put: USD: 1,500,000 how much would it cost to buy the £1,000,000?

Strike Price 1.5

Expiry Date 5th March 2004

• Would it be cheaper to use the Spot rate and let the

Delivery date 7th March 2004

Option expire or…

Premium: $5000

• Use the Option because the spot price in market would

cost more in USD.

Lets look at possible choices Big Company Could make

Page 45-49 in Workbook

68](https://image.slidesharecdn.com/bankingpresentation-120917055601-phpapp02/85/Banking-presentation-68-320.jpg)

Here is a conceptual example of how a bond trade works: 1. Big Company Ltd wants to acquire Small Company Inc for $1,000,000 but needs to raise capital to do so. 2. Big Company Ltd issues bonds to investors, effectively borrowing $1,000,000. 3. Investors purchase the bonds, providing Big Company Ltd with the $1,000,000 needed for the acquisition. 4. Big Company Ltd now owns Small Company Inc. 5. Big Company Ltd makes regular coupon payments to investors over the 10 year term of the bond. At maturity, Big Company Ltd repays the $1,000,000 principal amount to the investors. In this way