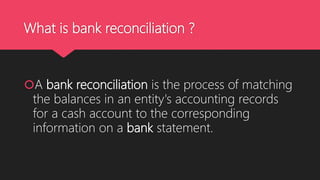

Bank reconciliation is the process of matching account balances in a company's records to the corresponding bank statement. This is done to equalize any differences between the two balances. Reasons for differences can include outstanding checks that have been written but not yet cashed, or deposits made but not processed by the bank in time to be included in the current statement. Performing regular bank reconciliations helps ensure accurate accounting records.

![Introduction to Banking Instruments @@@ [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/introductiontobankinginstrumentsautosaved-251224005412-0855ddf1-thumbnail.jpg?width=640&height=640&fit=bounds)