Improving profitability for small businessBen Wann

In this comprehensive presentation, we will explore strategies and practical tips for enhancing profitability in small businesses. Tailored to meet the unique challenges faced by small enterprises, this session covers various aspects that directly impact the bottom line. Attendees will learn how to optimize operational efficiency, manage expenses, and increase revenue through innovative marketing and customer engagement techniques.

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

The world of search engine optimization (SEO) is buzzing with discussions after Google confirmed that around 2,500 leaked internal documents related to its Search feature are indeed authentic. The revelation has sparked significant concerns within the SEO community. The leaked documents were initially reported by SEO experts Rand Fishkin and Mike King, igniting widespread analysis and discourse. For More Info:- https://news.arihantwebtech.com/search-disrupted-googles-leaked-documents-rock-the-seo-world/

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

Remote sensing and monitoring are changing the mining industry for the better. These are providing innovative solutions to long-standing challenges. Those related to exploration, extraction, and overall environmental management by mining technology companies Odisha. These technologies make use of satellite imaging, aerial photography and sensors to collect data that might be inaccessible or from hazardous locations. With the use of this technology, mining operations are becoming increasingly efficient. Let us gain more insight into the key aspects associated with remote sensing and monitoring when it comes to mining.

Attending a job Interview for B1 and B2 Englsih learnersErika906060

It is a sample of an interview for a business english class for pre-intermediate and intermediate english students with emphasis on the speking ability.

[Note: This is a partial preview. To download this presentation, visit:

https://www.oeconsulting.com.sg/training-presentations]

Sustainability has become an increasingly critical topic as the world recognizes the need to protect our planet and its resources for future generations. Sustainability means meeting our current needs without compromising the ability of future generations to meet theirs. It involves long-term planning and consideration of the consequences of our actions. The goal is to create strategies that ensure the long-term viability of People, Planet, and Profit.

Leading companies such as Nike, Toyota, and Siemens are prioritizing sustainable innovation in their business models, setting an example for others to follow. In this Sustainability training presentation, you will learn key concepts, principles, and practices of sustainability applicable across industries. This training aims to create awareness and educate employees, senior executives, consultants, and other key stakeholders, including investors, policymakers, and supply chain partners, on the importance and implementation of sustainability.

LEARNING OBJECTIVES

1. Develop a comprehensive understanding of the fundamental principles and concepts that form the foundation of sustainability within corporate environments.

2. Explore the sustainability implementation model, focusing on effective measures and reporting strategies to track and communicate sustainability efforts.

3. Identify and define best practices and critical success factors essential for achieving sustainability goals within organizations.

CONTENTS

1. Introduction and Key Concepts of Sustainability

2. Principles and Practices of Sustainability

3. Measures and Reporting in Sustainability

4. Sustainability Implementation & Best Practices

To download the complete presentation, visit: https://www.oeconsulting.com.sg/training-presentations

Accpac to QuickBooks Conversion Navigating the Transition with Online Account...PaulBryant58

This article provides a comprehensive guide on how to

effectively manage the convert Accpac to QuickBooks , with a particular focus on utilizing online accounting services to streamline the process.

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

What are the main advantages of using HR recruiter services.pdfHumanResourceDimensi1

HR recruiter services offer top talents to companies according to their specific needs. They handle all recruitment tasks from job posting to onboarding and help companies concentrate on their business growth. With their expertise and years of experience, they streamline the hiring process and save time and resources for the company.

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

Premium MEAN Stack Development Solutions for Modern BusinessesSynapseIndia

Stay ahead of the curve with our premium MEAN Stack Development Solutions. Our expert developers utilize MongoDB, Express.js, AngularJS, and Node.js to create modern and responsive web applications. Trust us for cutting-edge solutions that drive your business growth and success.

Know more: https://www.synapseindia.com/technology/mean-stack-development-company.html

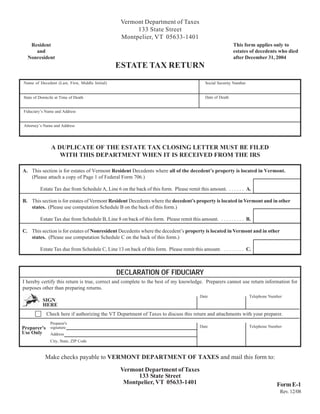

1. Vermont Department of Taxes

133 State Street

Montpelier, VT 05633-1401

This form applies only to

Resident

estates of decedents who died

and

after December 31, 2004

Nonresident

ESTATE TAX RETURN

Name of Decedent (Last, First, Middle Initial) Social Security Number

Date of Death

State of Domicile at Time of Death

Fiduciary’s Name and Address

Attorney’s Name and Address

A DUPLICATE OF THE ESTATE TAX CLOSING LETTER MUST BE FILED

WITH THIS DEPARTMENT WHEN IT IS RECEIVED FROM THE IRS

A. This section is for estates of Vermont Resident Decedents where all of the decedent’s property is located in Vermont.

(Please attach a copy of Page 1 of Federal Form 706.)

Estate Tax due from Schedule A, Line 6 on the back of this form. Please remit this amount. . . . . . . A.

B. This section is for estates of Vermont Resident Decedents where the decedent’s property is located in Vermont and in other

states. (Please use computation Schedule B on the back of this form.)

Estate Tax due from Schedule B, Line 8 on back of this form. Please remit this amount. . . . . . . . . . B.

C. This section is for estates of Nonresident Decedents where the decedent’s property is located in Vermont and in other

states. (Please use computation Schedule C on the back of this form.)

Estate Tax due from Schedule C, Line 13 on back of this form. Please remit this amount. . . . . . . . . C.

DECLARATION OF FIDUCIARY

I hereby certify this return is true, correct and complete to the best of my knowledge. Preparers cannot use return information for

purposes other than preparing returns.

Date Telephone Number

SIGN

HERE

Check here if authorizing the VT Department of Taxes to discuss this return and attachments with your preparer.

Preparer's

Date Telephone Number

Preparer's signature

Use Only Address

City, State, ZIP Code

Make checks payable to VERMONT DEPARTMENT OF TAXES and mail this form to:

Vermont Department of Taxes

133 State Street

Montpelier, VT 05633-1401 Form E-1

Rev. 12/08

2. COMPUTATION SCHEDULES

SCHEDULE A. Vermont Estate Tax Calculation - For use by all filers.

Before you begin the worksheet below, complete a pro forma Federal Form 706, Page 1, leaving Line 3b blank.

Attach to Vermont return.

1. Federal tentative taxable estate from Federal Form 706, Page 1, Line 3a . . . . . . . . . . . . . . . . . . . . . 1. ______________________

60,000.00

2. Adjustment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2. ______________________

3. Adjusted taxable estate. Subtract Line 2 from Line 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3. ______________________

4. Use the amount on Line 3 above to compute the estate tax liability

using the Vermont Estate Tax Table. Enter the tax amount here. . . . . . . . . . . . . . . . . . . . . . . . . . . . 4. ______________________

5. Enter amount from pro forma Federal Form 706, Page 1, Line 12 . . . . . . . . . . . . . . . . . . . . . . . . . . . 5. ______________________

6. Vermont estate tax. Enter the amount from Line 4 or Line 5, whichever is smaller. . . . . . . . . . . . . . 6. ______________________

Vermont Estate Tax Table - Computation of Estate Tax Liability

(1) (2) (3) (4) (1) (2) (3) (4)

Adjusted taxable Adjusted taxable Tax on amount in Rate of tax on Adjusted taxable Adjusted taxable Tax on amount in Rate of tax on

estate equal to or estate less than - column (1) excess over estate equal to or estate less than - column (1) excess over

more than - amount in more than - amount in

column (1) column (1)

(Percent) (Percent)

0 $40,000 0 None 2,040,000 2,540,000 106,800 8.0

$40,000 90,000 0 0.8 2,540,000 3,040,000 146,800 8.8

90,000 140,000 $400 1.6 3,040,000 3,540,000 190,800 9.6

140,000 240,000 1,200 2.4 3,540,000 4,040,000 238,800 10.4

240,000 440,000 3,600 3.2 4,040,000 5,040,000 290,800 11.2

440,000 640,000 10,000 4.0 5,040,000 6,040,000 402,800 12.0

640,000 840,000 18,000 4.8 6,040,000 7,040,000 522,800 12.8

840,000 1,040,000 27,600 5.6 7,040,000 8,040,000 650,800 13.6

1,040,000 1,540,000 38,800 6.4 8,040,000 9,040,000 786,800 14.4

1,540,000 2,040,000 70,800 7.2 9,040,000 10,040,000 930,800 15.2

10,040,000 --- 1,082,800 16.0

SCHEDULE B. Vermont Resident Decedents with real and tangible personal property located outside Vermont.

(Attach a copy of the 706 excluding exhibits and appraisals.)

1. Vermont estate tax from Schedule A, Line 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1. $ 76543210987654321

76543210987654321

76543210987654321

2. Tax liability actually paid for death taxes to a state other than Vermont 76543210987654321

76543210987654321

(Copies of nonresident returns must be attached.) . . . . . . . . . . . . . . . . . . . . . . . . . 2. $ 76543210987654321

76543210987654321

76543210987654321

3. Federal Total Gross Estate from Federal Form 706, Page 1, Line 1 . . . . . . . . . . . . 3. $ 76543210987654321

76543210987654321

76543210987654321

4. Non-Vermont Gross Estate* (see instructions for definition) . . . . . . . . . . . . . . . . . 4. $ 76543210987654321

76543210987654321

76543210987654321

5. Ratio of non-Vermont Gross Estate to Federal Estate (Line 4 divided by Line 3) . . . 5. 76543210987654321

76543210987654321

76543210987654321

6. Adjusted Vermont estate tax (Multiply Line 1 by Line 5) . . . . . . . . . . . . . . . . . . . . . 6. $ 76543210987654321

7. Enter the lesser of Line 2 or 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7. $

8. Tax Due (Line 1 less Line 7). Enter here and on front of return, Section B . . . . . . . . . . . . . . . . . . . . . . . . . 8. $

SCHEDULE C. Nonresident Decedents with real and tangible personal property located in Vermont.

(Attach a copy of the 706 excluding exhibits and appraisals.)

76543210987654321

76543210987654321

76543210987654321

9. Vermont estate tax from Schedule A, Line 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9. $ 76543210987654321

76543210987654321

76543210987654321

10. Federal Total Gross from Federal Form 706, Page 1, Line 1 . . . . . . . . . . . . . . . . . . 10. $ 76543210987654321

76543210987654321

76543210987654321

11. Vermont Gross Estate** (see instructions for definition) . . . . . . . . . . . . . . . . . . . 11. $ 76543210987654321

76543210987654321

76543210987654321

12. Ratio of Vermont Gross Estate to Federal Estate (Line 11 divided by Line 10) . . . . 12. 76543210987654321

13. Adjusted Vermont estate tax (Multiply Line 9 by Line 12)

Tax Due. Enter here and on front of return, Section C . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13. $

3. NOTE: An estate with a closely-held farm business

may be eligible for a special reduction in the Vermont

estate tax. Contact the Vermont Department of Taxes

at (802) 828-2548 for more information.

GENERAL INSTRUCTIONS

Date of Filing Returns

Vermont Estate Tax Returns are required to be filed at the time the Federal Estate Tax Return is required to be filed under

the laws of the United States, including any extension of time for filing granted by federal authorities.

Tax Payable

The Vermont Estate Tax is due and payable by the executor or other fiduciary at the time the Vermont Estate Tax Return is

required to be filed. An extension of time to file the VT Estate Tax Return does not extend the time to pay. The tax

estimated to be due must be paid with the extension of time request.

Where to File

Vermont Department of Taxes

133 State Street

Montpelier, VT 05633-1401

Extension of Time

Prior to the due date of the return, a copy of the Federal application for extension of time to file or a letter requesting an

extension of time must be submitted to the Vermont Department of Taxes

VT ESTATE TAX DEFINITIONS

Vermont Resident Decedent means a person whose domicile is in Vermont at date of death.

* Non-Vermont Gross Estate for a Vermont Resident Decedent means the total value of real estate and tangible personal

property (cars, boats, clothes, jewelry, furniture, etc.) which is located outside Vermont at the date of death and is

taxed by another state.

** Vermont Gross Estate for a nonresident decedent means the value of real estate and tangible personal property (cars,

boats, clothes, jewelry, furniture, etc.) located in Vermont at date of death.

PLEASE NOTE: Bank accounts, stocks, bonds and mortgages are intangible assets and are taxable by the State in

which the decedent was a resident at time of death regardless of where the asset was located at the date of death.