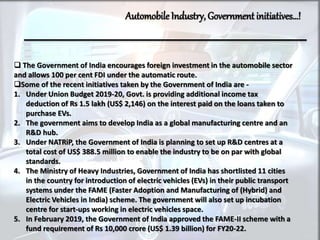

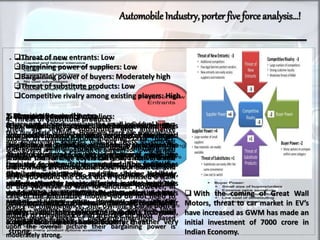

The document provides a comprehensive analysis of the automobile industry, detailing its economic significance, market growth projections, and government initiatives supporting foreign investment and electric vehicle adoption in India. It also includes a Porter’s Five Forces analysis, indicating low threats of new entrants and substitutes, high rivalry among existing players, and moderate buyer bargaining power. Key industry trends include a significant growth in domestic automobile sales and production, with projections for the global automotive market reaching USD 83 billion by 2022.

![Automobile industry presentation [autosaved]](https://cdn.slidesharecdn.com/ss_thumbnails/automobileindustrypresentationautosaved-120202020248-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)