Download as PDF, PPTX

![Fund Based Advances

!

D CC - Demand Cash Credit

!

S OD - [Secured] Over Draft

!

Ad hoc Over Draft

!

EPC - Export Packing Credit

(Purchase Order Defacing)

!

TL - [Open] Term Loan

Non Fund Based Advances

!

BG - Bank Guarantee

!

Revolving BG

!

LC/LSC - Letter of [Small] Credit

!

Bill Discounting (Usanse /

Collection / Sight)

!

Buyers Credit

Banking and Advances

Bank Audit Through CBS

or the Line of Credit!](https://image.slidesharecdn.com/auditthroughcorebankingsolution-150402025054-conversion-gate01/85/Audit-through-core-banking-solution-6-320.jpg)

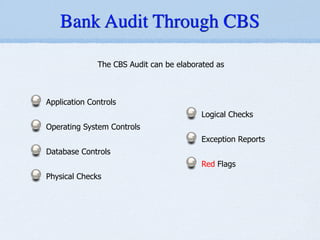

The document discusses the significance of auditing in banks within a computer-based banking system (CBS). It covers various aspects of CBS, such as control measures, menu functions, key features, and the importance of data validation and compliance. Additionally, it outlines the roles of different software vendors and provides insights into the potential risks and red flags associated with bank audits.