Download to read offline

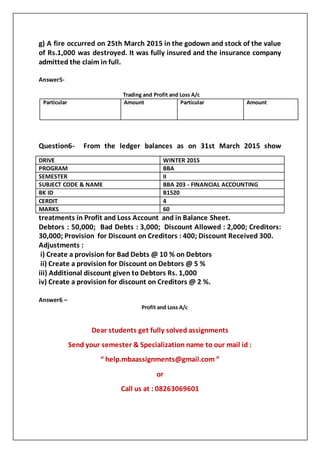

The document provides detailed instructions for MBA students regarding solved assignments in financial accounting, including multiple questions related to partnership balance sheets, cash books, goodwill treatment, and trading accounts. Students are required to prepare specific financial statements and accounts based on given data and adjustments. Additionally, students can seek assistance via email or phone for their assignments.