VIP Call Girl in Mira Road 💧 9920725232 ( Call Me ) Get A New Crush Everyday ...

Trading,pl and balance sheet

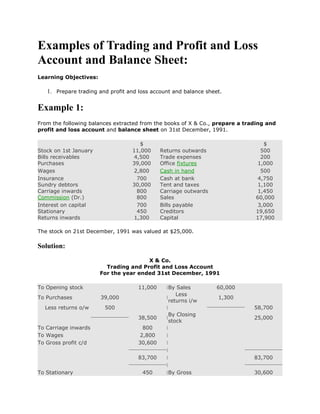

1. Examples of Trading and Profit and Loss

Account and Balance Sheet:

Learning Objectives:

1. Prepare trading and profit and loss account and balance sheet.

Example 1:

From the following balances extracted from the books of X & Co., prepare a trading and

profit and loss account and balance sheet on 31st December, 1991.

$ $

Stock on 1st January 11,000 Returns outwards 500

Bills receivables 4,500 Trade expenses 200

Purchases 39,000 Office fixtures 1,000

Wages 2,800 Cash in hand 500

Insurance 700 Cash at bank 4,750

Sundry debtors 30,000 Tent and taxes 1,100

Carriage inwards 800 Carriage outwards 1,450

Commission (Dr.) 800 Sales 60,000

Interest on capital 700 Bills payable 3,000

Stationary 450 Creditors 19,650

Returns inwards 1,300 Capital 17,900

The stock on 21st December, 1991 was valued at $25,000.

Solution:

X & Co.

Trading and Profit and Loss Account

For the year ended 31st December, 1991

To Opening stock 11,000 |By Sales 60,000

Less

To Purchases 39,000 | 1,300

returns i/w

Less returns o/w 500 | 58,700

By Closing

38,500 | 25,000

stock

To Carriage inwards 800 |

To Wages 2,800 |

To Gross profit c/d 30,600 |

|

83,700 | 83,700

|

To Stationary 450 |By Gross 30,600

2. profit b/d

To Rent and rates 1,100 |

To Carriage

1,450 |

outwards

To Insurance 700 |

To Trade expenses 200 |

To Commission 800 |

To Interest on

700 |

capital

To Net profit |

transferred to 25,200

capital a/c |

|

30,600 | 30,600

|

X & Co.

Balance Sheet

As at 31st December, 1991

Liabilities $ | Assets $

Creditors 19,650 |

Cash in hand 500

Bills payable 3,000 |

Cash at bank 4,750

Capital 17,900 |

Sundry debtors 30,000

Add Net profit 25,200 |

Bill receivable 4,500

43,100 |

Stock 25,000

|

Office equipment 1,000

|

65,750 |

65,750

|

Example 2:

The following trial balance was taken from the books of Habib-ur-Rehman on December 31,

19 ....

Cash 13,000

Sundry debtors 10,000

Bill receivable 8,500

Opening stock 45,000

Building 50,000

Furniture and fittings 10,000

Investment (Temporary) 5,000

Plant and Machinery 15,500

Bills payable 9,000

Sundry creditors 20,000

Habib's capital 78,200

3. Habib's drawings 1,000

Sales 100,000

Sales discount 400

Purchases 30,000

Freight in 1,000

Purchase discount 500

Sales salary expenses 5,000

Advertising expenses 4,000

Miscellaneous sales expenses 500

Office salary expenses 8,000

Misc. general expenses 1,000

Interest income 1,000

Interest expenses 800

2,08,700 2,08,700

Closing stock on December 31, 19 ... was $10,000

Required: Prepare income statement/trading and profit and loss account and balance sheet

from the above trial balance in report form.

Solution:

Habib-ur-Rehman

Income Statement/Profit and Loss Account

For the year ended December 31, 19.....

Gross sales 100,000

Less: Sales discount 400

Net Sales 99,600

Cost of Goods Sold:

Opening stock 45,000

Purchases 30,000

Add: Freight in 1,000

31,000

Less purchase discount 500

Net purchases 30,500

Cost of goods available fort sale 75,500

Less closing stock 10,000

Cost of goods sold 65,500

4. Gross profit 34,100

Operating Expenses:

Selling Expenses:

Sales salary expenses 5,000

Advertising expenses 4,000

Misc. selling expenses 500

9,500

General Expense:

Office salaries expenses 8,000

Misc. general expenses 1,000

9,000

Total operating expenses 18,500

Net profit from operations 15,600

Other Expenses and Incomes:

Interest income 1,000

Interest expenses 800

Net increase 200

Net income 15,800

Habib-ur-Rehman

Balance Sheet

As at December 31, 19.....

ASSETS

Current Assets:

Cash 13,000

Sundry debtors 10,000

Bills receivable 8,500

Stock on Dec. 31, 19 .. 10,000

Investment 5,000

Total Current Assets 46,500

Fixed Assets:

Buildings 50,000

Plant and Machinery 15,500

Furniture and fittings 10,000

Total Fixed Assets 75,500

5. Total Assets 122,000

LIABILITIES:

Current Liabilities:

Sundry creditors 20,000

Bills payable 9,000

Total Current Liabilities 29,000

Fixed Liabilities:

Habib's capital 78,200

Net income for the year 15,800

94,000

Less: Drawings 1,000

93,000

Total Liabilities and Capital 122,000

………………………………………………………………………………………………………………………………………………………………

6. Preparing Profit and Loss Account From Trial

Balance

Preparation of Profit and Loss Account

Profit and loss account or income statement is prepared from the trial balance.

To keep things as simple as possible initially a very simple version of profit and loss account

is shown and the more complex issues and more elegant formatting of the report are not

covered in this article.

We start with the following trial balance

Trial Balance of Narayana Rao & Co, on 31.12.2007

Account Debit Credit

Rs. Rs.

Purchases 100,000

Wages 6,000

Rent 2,400

Travelling expenses 4,800

Interest 1,200

Returns inward 4,000

Bank 10,000

Cash 34,000

Machinery 14,000

Furniture 1,000

Loan 45,800

Miscellaneous expenses 200

8. Travelling expenses 4,800

Interest 1,200

Returns inward 4,000

Salaries 12,000

Insurance 800

Discount 900

Miscellaneous 200

expenses

Advertisements 2,400

Net Profit 8,200

152,900 152,900

Procedure of Preparing Profit and Loss Account From Trial Balance

From trial balance all amounts nominal accounts (accounts related to revenues and

expenses) are shown in the debit and credit sides of the profit and loss account. This

account is similar to the other accounts in the ledger. All credit amounts in the trial balance

are shown in the credit side of the P&L account and all debit amounts are shown on the

debit side. When totals of these two sides are compared, if credit side is more than the debit

side, the firm has made a profit. In the example the credit side is more than the debit side by

Rs. 8,200. This amount is shown at the end in the debit side as net profit. Then similar to

the ledger accounts, the total of both sides are shown at the both sides in the same line at

the same level.

If you notice an additional entry which was not there in the trial balance was included in the

credit side of P&L account. This item is stock on 31-12-2007. The closing stocks in the store,

shop floor and finished goods store are ascertained and are valued by accountants. This

figure is to be included in the profit and loss account to determine the profit made in a

period.

After the profit and loss account is prepared, balance sheet of the firm, that shows its assets

and liabilities as on the day can be prepared. All real accounts with debit balances are assets.

All personal accounts with credit balances are liabilities. All personal accounts with debits

balances are assets. All customers' account balances are summed up and the total amount is

9. shown as sundry debtors in the balance sheet. All suppliers' account balances are summed

and the total amount is shown as sundry creditors in the balance sheet.

Liabilities Rs. Assets Rs.

Sundry 50,000 Buildings 10,000

creditors

Loan 45,800 Machinery 14,000

Capital 110,000 Furniture 1,000

Net Profit 8,200 Sundry 80,000

debtors Balance

Sheet as on 31.12.2007

Drawings 15,000

Stock (31- 50,000

12-2007)

Bank 10,000

Cash 34,000

214,000 214,000

As mentioned at the beginning many complex adjustments that are done to prepare profit

and loss account and balance sheet as well as certain formatting conventions are ignored to

provide a simple treatment in this article. The objective of the article is to show the basic

logic of determining profit and then preparing a balance sheet.

………………………………………………………………………………………………………………………………………………………………….

10. How to Prepare a Trading Account?

FOLLOW

How to prepare a Trading Account? Let us now consider the individual items recorded in the Trading

Account. (i) Opening Stock : This means the closing stock of the previous year. In the first year of

business there will be no opening stock. In a trading concern the opening stock consists of finished goods

only. But in a manufacturing concern, it comprises raw materials, work in progress, and finished goods.

Opening stock is the first item on the debit side of the Trading account.

How to prepare a Trading Account?

Let us now consider the individual items recorded in the Trading Account.

(i) Opening Stock : This means the closing stock of the previous year. In the first year of business there

will be no opening stock. In a trading concern the opening stock consists of finished goods only. But in a

manufacturing concern, it comprises raw materials, work in progress, and finished goods. Opening stock

is the first item on the debit side of the Trading account.

(ii) Purchases and Purchase Return: Purchases include cash and credit purchase of goods. Purchases

are recorded on the debit side of the Trading Account after deducting the Returns outward or Purchase

return. Care should be taken to ensure that purchases do not include the amount of goods taken or

purchased by the proprietor for his own use, the cost of goods received on consignment, goods in transit,

goods purchased on hire purchase basis, goods distributed as free samples. ,

(iii) Direct Expenses: These include manufacturing wages, carriage inward, power and fuel, factory

lighting and heating, factory rent and rates, factory insurance, freight, octroi, customs duty on imported

materials, royalty on production, etc. These expenses are recorded on the debit side of the Trading

Account.

11. (iv) Sales and Sales Return: Sales include both cash and credit sales. Sales return or Return outward is

deducted from total sales and net sales are credited to the Trading Account. Care should be taken to

ensure that sales do not include sale of any fixed assets, goods sent on consignment and goods sold on

approval.

(v) Closing Stock: It means the goods which remain unsold at the end of the accounting year. Closing

stock is valued on the principle of cost or market price whichever is lower. It is exposed on the credit side

of the Trading Account. Closing stock is also shown, as an asset in the Balance Sheet.

While preparing the Trading Account, adjustment entries are made for expenses outstanding and

expenses paid in advance, if any. For example, a part of the direct wages or factory rent may be

outstanding. Similarly, factory insurance might have been paid in advance for some months of the next

year. Expenses outstanding are added to while expenses paid in advance are deducted from the

expenses shown on the debit side of the Trading Account.

Note : Carriage outwards, packing charges for goods sold, export duty, cash discount on sales pill appear

in Profit and Loss Account, because these are all selling expenses

…………………………………………………………………………………………………………………………

12. Prepare Trading and Profit and Loss Account and Balance Sheet

>> OCTOBER 14, 2010

In corporate accounting, you have to learn final accounts of company in which you have to

prepare trading and profit and loss account and balance sheet. These statements are advance

than final accounts of individual. You have to spend your brain to understand its adjustments. I

am taking one of following question and tell you how to solve it. This question came in my

M.Com.'s higher Accounts.

Problem

The alfa manufacturing company ltd. was registered with a nominal capital of Rs. 60,00,000 in

equity shares of Rs. 10 each. The following is the list of balances extracted from its books on

31st March , 2009.

Calls in arrears Rs 75,000

Premises Rs. 30,00,000

Plant and machinery Rs. 33,00,000

Interim Dividend paid on Ist Nov. , 2009 Rs. 3,92,500

Stock, 1st April, 1988 Rs. 7,50,000

Fixtures Rs. 72,000

Sundry Debtors Rs. 8,70,000

Goodwill Rs. 2,50,000

13. Cash in hand Rs. 7,500

Cash at Bank Rs. 3,99,000

Purchases Rs. 18,50,000

Preliminary Expenses Rs. 50,000

Wages Rs. 8,48,650

General Expenses Rs. 68,350

Freight and Carriage Rs. 1,31,150

Salaries Rs. 1,45,000

Directors' Fees Rs. 57,250

Bad Debts Rs. 21,100

Debenture Interest Paid Rs. 1,80,000

Share Capital Rs. 40,00,000

12% Debentures Rs. 30,00,000

Profit and loss account ( credit balance) Rs. 2,62,500

Bill Payable Rs. 3,70,000

Sundry Creditors Rs. 4,00,000

Sales Rs. 41,50,000

14. General Reserve Rs. 2,50,000

Bad Debts provision 1st April 2009 Rs. 35,000

Prepare trading and profit and loss account and balance sheet in proper form after making the

following adjustments

i) Depreciation plant and machinery by 15%

ii) Write off Rs. 5,000 from preliminary expenses

iii) Provide for half year's debenture interest due.

iv) Leave bad and doubtful debts provision at 5% on sundry debtors.

v) Provide for income tax @ 50%

vi) Stock on 31st march, 2010 was Rs. 9,50,000

Solution

Ist Step : Write Small sign in list of balances relating to

adjustment

In first step of solving this problem, you have to read the question and write small sign in list of

balances relating to adjustment. With this, you can treat correctly.

2st Step : Make Working Notes for Adjustments

Working Notes :-

1. ) Depreciation on plant and machinery by 15%

15. 33,00,000 X 15% = 4,95,000

2. Rs. 5,000 written off preliminary expenses will show in the debit side of profit and loss

account. And rest Rs. 45,000 will show in the asset side in balance sheet.

3.) Show half year debenture interest due as outstanding interest in the debit side of

profit and loss account.

4) Provision for Doubtful Debts Account

Credit Side :

Bad debts provision 1st April, 1988 Rs. 35,000

Transfer to Profit and loss account (Balancing figure) Rs 29,600

--------------------------------------------------------------------

Total = Rs. 64,600

--------------------------------------------------------------------

Debit Side

Bad Debts Rs. 21,100

New bad debts provision 5%

8,70,000 X 5% = Rs. 43,500

-------------------------------------------------------------------

Total Rs. 64,600

-------------------------------------------------------------------

16. Now, balancing figure of Rs. 29600 will go to debit side of profit and loss account and new

provision of Rs. 43500 will deduct from sundry debtors in balance sheet.

5) Provide for Income Tax @ 50%

Calculate net profit before charging income tax in profit and loss account and then calculate its

50% and it will be shown as provision for income tax in the debit side of profit and loss account

and also it will be shown in the liability side in balance sheet.

6) Closing stock of Rs. 9,50,000 will go to the credit side of trading account. We will also show it

in asset side in balance sheet.

7) Interim dividend paid will go to the debit side of profit and loss appropriation account. 15%

dividend distribution tax and surcharge of 3% is paid by companies before distribution. It means

it will also be debited in profit and loss appropriation account. In balance sheet, dividend

distribution tax and surcharge will be shown in the liability side in balance sheet.

8.) Call in arrears will deduct from equity share capital in liability side of balance sheet.

After this, you have to make trading, profit and loss account, profit and loss appropriation

account and balance sheet.

………………………………………………………………………………………………………………………………………………………………

17. How to prepare balance sheet

Prepare balance sheet from trial balance in five easy steps. Format and elements of

classified balance sheet.

1. Reasons companies prepare balance sheet

A balance sheet is a picture of a company's financial position as of a point in time. A balance

sheet can be prepared as of any date, but it's usually prepared as of month, quarter or year-end.

A balance sheet is a very valuable statement that provides information about financial health of a

company. Things like cash, accounts receivable, accounts payable, net worth, etc. can be

determined by looking at a balance sheet.

There are multiple good reasons to prepare a balance sheet. First, you (as a business owner or a

business manager) will want to know where your company stands in terms of financial health at

a point in time. Second, anybody interested in your company will want to see your balance sheet.

Such interested parties may include the following:

Banks: Financial institutions want to know if your company will be able to repay a loan when you

apply for one.

Investors: At some point one source of capital (your savings in the business) may not be

sufficient to maintain a rapid growth. You may want to find investors who would like to invest in

your company. Before inventors give you their money, though, they might want to see a balance

sheet (and other financial statements) to ensure their investments won't go south in the future.

Authorities: Some authorities might like to see a balance sheet of your business. A good

example is the Internal Revenue Service (IRS).

Vendors: Sometimes vendors ask for a balance sheet (and other financial statements) to

understand if you will be able to settle your obligations. Note: Where possible, you should also

ask for the vendors' financial statements to understand if your vendors will stay in business long

enough to provide you with the products you buy from them.

Customers: Similar to vendors, customers may sometimes ask for a balance sheet (and other

financial statements) to understand if you will be able to stay in business to provide them with

products or services you sell. For instance, from customers' standpoint, changing vendors may

be time and resource-consuming; thus, customers want to analyze your balance sheet to make

sure you will not go bankrupt in the near future. Note: Where possible, you should also ask for

customers' financial statements to see if they will be able to pay for goods or services you

provide.

As you can see, there are a lot of parties that will be interested in a balance sheet of your

company, so it's a good idea to prepare one regularly.

18. How to prepare balance sheet

2. Classifications on balance sheet

All balance sheets are normally classified: that is, different financial elements on a balance sheet

are grouped into categories and presented under a common caption. This is a general practice

that helps to compare balance sheets of different companies. You can see an example below. For

instance, if there are two companies within different industries, they may have different items

(components) going into the Current Assets category. However, due to this classification rule, it

may sometimes not be as relevant to compare components of current assets. Instead, you may

just compare the total current assets of the two companies, and that may be all you need in your

analysis.

Illustration 1: Example of classifications on the balance sheet (horizontal)

Assets Liabilities

Current Assets Current liabilities

Investments Non-current liabilities

Fixed Assets

Intangible Assets Equity

Other Non-current Assets Common Stock

Retained Earnings

The example above shows a balance sheet in a horizontal format: Assets are on the left side, and

Liabilities and Equity are on the right side. It is also possible to present a balance sheet in a

single column format (vertically) as follows:

Illustration 2: Example of classifications on the balance sheet (vertical)

Assets

Current Assets

Investments

Fixed Assets

19. Intangible Assets

Other Non-current Assets

Liabilities

Current liabilities

Non-current liabilities

Equity

Common Stock

Retained Earnings

It is a matter of preference, but normally balance sheets are presented vertically as shown in

Illustration 2.

Important term to remember, as we discuss balance sheet classifications further, is a balance

sheet date. A balance sheet date is the date as of which the balance sheet is prepared. For

example, most businesses prepare their balance sheets at least once a year as of December 31.

However, the balance sheet date is not the date when a balance sheet is actually prepared and

becomes available.

As you may have noticed in Illustration 1, assets are on the left side, and liabilities and equity are

on the right side. There is a reason why they are presented liked that. Total assets equal the sum

of total liabilities and total equity. This is a fundamental accounting equation that results in this

equality:

Assets = Liabilities + Equity

This equation must hold true in any balance sheet, and if it doesn't, then it is due to an error

somewhere in the balance sheet. You can use this rule in situations where your assets don't equal

your liabilities and equity.

The reason the equation must hold true is because assets are economic resources of a business

used to accomplish its main goal, i.e. increase owners' wealth. Liabilities and equity are the

sources of such assets. In other words, liabilities and equity show where assets were obtained

20. from. Liabilities are claims of third parties for resources provided to the business (e.g. creditors).

Equity is claims of business owners for resources they invested in the business. Equity, therefore,

is an indicator of how many assets the owners can claim in the business after all liabilities are

settled. The difference between assets and liabilities (i.e. equity) is sometimes called net worth.

Any trial balance account (trial balances are a starting point in preparing a balance sheet – see

further) has a balance. An account may have a debit or credit balance. The normal account

balance also indicates whether the account is increased or decreased when it's debited or

credited. There are rules stating which account has a debit or credit balance. The illustration

below shows accepted conventions about such balances:

Illustration 3: Normal balances, increases and decreases for balance sheet accounts

Increase (Normal

Balance Sheet Category Decrease

Balance)

Assets Debit Credit

Contra Asset Accounts Credit Debit

Liabilities Credit Debit

Contra Liability Accounts Debit Credit

Equity Credit Debit

For example, an asset account called Cash increases when it's debited and decreases when it's

credited. The Cash account normally has a debit balance.

Note that there are "contra" accounts. Such accounts are opposite to their related accounts and

thus have a different normal balance. Contra accounts are presented as a reduction to their related

accounts on the balance sheet. An example of such accounts is Accumulated Depreciation. This

account has a credit balance and is related to the Fixed Assets account. On the balance sheet,

Accumulated Depreciation (credit balance) is shown under Fixed Assets (debit balance) and

reduces the balance of Fixed Assets creating Net Fixed Assets.

Going back to the accounting equation, note that assets normally have debit balances, and

liabilities and equity have credit balances:

Debit Balance Credit Balance Credit Balance

Assets = Liabilities + Equity

21. Let's review each balance sheet classification in more detail.

How to prepare balance sheet

2.1. Current assets on classified balance sheet

Current assets are cash and other assets that are expected to be converted to cash or sold or used up

usually within one year or the company's operating cycle, whichever is longer, through the normal

operations of the business.

An operating cycle, for a manufacturing company, represents time it takes to invest cash by buying raw

materials, produce a product, and receive cash back after selling the product. An operating cycle may be

more or less than a year depending on the industry.

Current assets are usually listed in the order of liquidity starting with cash and cash equivalents.

Examples of current assets are cash and cash equivalents, marketable securities, accounts

receivable, inventories, and prepaid expenses.

Cash and cash equivalents represent coins, currency, checks, money orders, money on deposit and

short-term, highly liquid investments that are usually reported with cash on the balance sheet. Normally,

highly liquid means that the investments can be converted to cash within 90 day and with a minimal loss

in their value due to changes in interest rates.

Marketable securities are short-term (temporary) investments in securities and other interest-generating

financial assets. Such investments are usually made to earn interest on excess cash which is currently

not used in the business.

Accounts receivable are amounts due from customers on credit sales (i.e. sales when customers agree

to pay you later).

Accounts receivable sometimes may have a related contra asset account called Allowance for

Doubtful Accounts. Such an account represents the amounts that you believe may not be

collectable (e.g. a customer is bankrupt). The net amount (Accounts Receivable – Allowance for

Doubtful Accounts) is shown on the balance sheet.

Inventories are raw materials, work-in-process (i.e. started but unfinished products), finished goods (i.e.

products ready for sale), and sometimes supplies (e.g. spare parts for your machinery and equipment).

Similar to accounts receivable, the Inventories Account may also have a related contra asset

account called Excess and Obsolete Reserve (E&O Reserve). This account represents the cost of

inventory that you do not anticipate to sell or use in your production any more due to technical

22. obsolescence, etc. The net amount (Inventories – E&O Reserve) is presented on the balance

sheet. Note that not all businesses will have an E&O reserve.

Prepaid assets are prepayments you've made that will benefit future periods.

For example, if you pay an insurance premium for your business, the coverage you obtain is for a

year. Thus, the benefits you will be getting from this asset are extended over a year. Normally,

prepaid assets shown in the current assets are the ones expected to be used (expected to expire)

within a year after the balance sheet date. If a prepaid asset is expected to provide benefits for

longer, then the portion of the prepaid asset related to benefits after one year is shown in the non-

current assets (i.e. Other Non-current Assets) on the balance sheet.

2.2. Non-current assets on classified balance sheet

All assets not included into current assets are non-current (long-term) assets. They are presented

on the balance sheet after the current assets and may include the following classifications: fixed

assets, intangible assets, investments, and other non-current assets. Let's review each

classification in greater detail.

Fixed assets may include land, buildings, machinery and equipment, vehicles, and leasehold

improvements.

Fixed assets are expected to be utilized by the company (i.e. provide benefits) over a period

longer than one year. Note that fixed assets are tangible assets (i.e. have physical substance).

Fixed assets, as they provide benefits, use up some of their cost.

The process of allocating this decrease in fixed assets' cost to multiple years is called depreciation.

A contra asset account called Accumulated Depreciation keeps information about how much of

the fixed assets' cost has been depreciated. The net amount (Fixed Assets – Accumulated

Depreciation) is shown on the balance sheet.

Intangible assets may include patents, goodwill, technology, customer lists, value of non-compete

agreements, among others.

Intangible assets are similar to fixed assets except that the major value of intangible assets comes

with the rights they bring to the owner and not their physical substance. Similar to fixed assets,

some intangible assets lose their value with time as they provide benefits (process is called

amortization), and this process is reflected in the Accumulated Amortization account. Note,

however, that some intangible assets (e.g. trademarks or goodwill) have indefinite lives, and

thus, they are not amortized.

23. Investments are long-term investments in securities of other companies. Such securities may be debt

securities (e.g. bonds, notes receivable) or equity securities (e.g. stock).

Other non-current assets may include other long-term assets not included into the investments, fixed, or

intangible assets categories. Such other assets may be portions of prepaid expenses that will start

expiring in more than a year after the balance sheet date, the cash surrender value of life insurance on

officers, and others.

How to prepare balance sheet

2.3. Current liabilities on classified balance sheet

Current liabilities are obligations due to be paid or settled within one year or the company's operating

cycle, whichever is longer.

Usually current liabilities are settled by using current assets. Therefore, sometimes it is useful to

compare current assets and current liabilities to understand if your business will be able to pay

your current obligations using your current assets (the difference between the two is called

working capital). Current liabilities may include accounts payable, accrued expenses, short-term

loans, current portion of long-term debt, and income taxes payable. Let's review current

liabilities in greater detail.

Accounts payable are liabilities (obligations) created by buying goods or services on account. In other

words, it is your company's promise (and obligation) to pay for purchased goods or service later.

For example, if you purchased merchandise inventory today, and the credit terms state that you

need to pay for the inventory next month, then you need to record this obligation as an account

payable in your books.

Accrued expenses represent costs incurred but unpaid as of the period end.

Accrued expenses are required under the accrual basis of accounting, which is used for financial

reporting purposes. An example of accrued expenses may be a cell phone bill with the billing

period running from the 16th of the current month to the 15th of the following month. You will

not receive the bill until the middle of the next month; however, you have used the cell phone for

15 days in the current month and, therefore, should recognize cell phone expense for 15 days of

the current month by posting an accrued expense.

Short-term loans are notes payable expected to be settled within one year after the balance sheet date.

24. For example, if your company purchased equipment and issued a note payable to be settled in six

months after the balance sheet date, then the amount of the note will be recorded under short-

term loans.

Current portion of long-term debt represents the amount of long-term debt that will be paid within one

year after the balance sheet date.

For example, some long-term debts (i.e. bank loans) are required to be paid in installments

quarterly or semiannually, and then, a balloon payment is made at the maturity date for the

remaining balance. The installment payments to be paid within one year after the balance sheet

date represent short-term obligations and thus are recorded in the current liabilities under the

caption "Current Portion of Long-term Debt" (may be shortened to Current Portion of LT Debt).

Income taxes payable are the amounts of income taxes that your company is obligated to pay to local,

state, or federal authorities. These obligations are presented in the current liabilities section because it is

usually expected that these balances will be paid within a year after the balance sheet date.

2.4. Non-current liabilities on classified balance sheet

Non-current (long-term) liabilities are other liabilities that are not included into the current

liabilities section. Therefore, non-current liabilities are obligations that are not expected to be

due (paid) within one year after the balance sheet date. Examples of non-current liabilities are

long-term lines of credit and term loans.

A line of credit is an agreement, under which a bank provides your business with loans of money (i.e. up

to an approved limit) during a predefined period.

You can take out the amount you need (e.g. via check, ATM, etc.), repay it, and then borrow

again. At a point in time you can only have an outstanding balance up to a certain limit. This

kind of loans is sometimes called revolving loans. If an outstanding amount is to be repaid within

more than a year after the balance sheet date, then the amount is shown under the non-current

liabilities on the balance sheet date.

Term loans are loans that are to be paid on a certain date (i.e. maturity date). Again, if the payment date

is not within one year after the balance sheet date, then the loan is presented under the non-current

liabilities.

As mentioned above, when we talked about current liabilities, any portion of long-term debts

(whether it's a line of credit or term loan), which is to be paid within one year after the balance

sheet date, must be presented under the current liabilities

25. How to prepare balance sheet

2.5. Equity on classified balance sheet

Equity is the owners' claim on assets. Equity, as noted above, is also the difference between

assets and liabilities. Equity may include multiple financial elements. The most common equity

elements are capital (common stock), current year earnings, and retained earnings. Let's review

them in more detail.

Capital (common stock for corporations) represents the amounts contributed by owners to the business.

Depending on the legal form of a business, capital can be named differently.

Current year earnings are the net income or loss of the business for the current year. This amount is the

difference between all revenues and all expenses on the income statement. Current year earnings are

presented on the balance sheet only until they are transferred to retained earnings.

Retained earnings are net income (loss) retained (accumulated) by your company.

For a company with relatively simple operations, retaining earnings are cumulative net incomes

(losses) less dividends paid out since the company's origination. Note that when dividends are

paid out, they reduce retaining earnings. Also note that retained earnings may be a negative

amount in situations when the company is not profitable (i.e. more losses than net incomes).

3. Balance sheet format

A balance sheet is a financial statement that has a certain commonly used format.

First of all, a balance sheet has a header. The header needs to include your company name, the

title of the financial statement (i.e. balance sheet), and period(s) presented in the financial

statement. Note that some balance sheets are presented for one year, while others are presented

for two years in a comparable format (e.g. comparable balance sheets of public companies). An

example of the header for a single-year balance sheet is presented below:

Your Company Name

Balance Sheet

December 31, 2010

Next, the balance sheet with related captions is presented. Major captions (Assets, Liabilities,

Equity) are presented first. Then, the next level captions are shown. The next level captions are

the categories (classifications) we reviewed earlier (current assets, investments, etc.). Under each

caption, components of the caption are presented. An example of the current assets caption is

presented below:

26. ASSETS

Current Assets

Cash

Marketable Securities

Accounts Receivable

Inventories

Prepaid Expenses

Note how the components of current assets are intended to the right so it's easier to read the

balance sheet.

Finally, let's recall that assets can be shown on the left side while liabilities and equity are shown

on the right side (horizontal presentation). Alternatively, assets can be shown first with liabilities

and equity presented underneath the assets. If a balance sheet for a single period is shown, it

seems to be more readable to show assets on the left and liabilities and equity on the right side.

However, if comparable balance sheets (i.e. a balance sheet for two or more periods) are

prepared, then it makes more sense to show liabilities and equity under assets.

How to prepare balance sheet

4. Example of preparing balance sheet

There are several steps in preparing a balance sheet. These steps are not prescribed procedures,

so there may be variations based on your company’s needs and situation. Let’s review each step

in detail.

4.1. Step 1: Prepare balance sheet template

A balance sheet template is a blank format with header, date, categories, and components of

categories. The template can be prepared on paper, or better off, it can be prepared in a

spreadsheet software (e.g. MS Excel).

For our illustration, we prepared a balance sheet template in MS Excel and presented it below.

The template is in the vertical format due to width limitations on our website:

27. Illustration 4: Balance sheet template

Your Company Name

Trial Balance

December 31, 20X0

ASSETS

Current Assets:

Cash & Cash Equivalents

Marketable Securities

Accounts Receivable

Inventories

Prepaid Expenses

Total Current Assets

Fixed Assets

Intangible Assets

Investments

Other Non-current Assets

TOTAL ASSETS

LIABILITIES

Current Liabilities:

Accounts Payable

28. Your Company Name

Trial Balance

December 31, 20X0

Accrued Expenses

Short-term Loans

Current Portion of LT Debt

Income Taxes Payable

Total Current Liabilities

Non-current Liabilities:

Line of Credit

Term Loan

Total Non-current Liabilities

TOTAL LIABILITIES

EQUITY

Capital

Current Year Earnings

Retained Earnings

TOTAL EQUITY

TOTAL LIABILITIES & EQUITY

29. The spaces highlighted in light green are the ones where we will enter amounts taken from the

trial balance.

How to prepare balance sheet

4.2. Step 2: Obtain trial balance for your company

A trial balance is the collection of all accounts that exist in the company's chart of accounts with

balances as of a particular date. Each account has either a debit or credit balance. The total of all

debits equals the total of all credits (i.e. double-entry accounting system).

Most businesses, nowadays, use accounting software that is capable of generating a trial balance.

Therefore, for your purposes, you can extract such a trial balance from your software. If you

don't use such software, then you can prepare a trial balance from your records using, for

example, MS Excel.

For our illustration, we obtained the trial balance from our accounting software as shown below:

Illustration 5: A trial balance extracted from accounting software

Your Company Name

Trial Balance

December 31, 20X0

Account Account Name Debit Credit

1000 Petty Cash $ 500

1010 Chase Checking 42,000

1020 PayPal Checking 23,500

1030 Savings 300,000

1040 Money Market 25,000

1200 Marketable Securities 0

1300 Accounts Receivable 389,000

1350 Allowance for Doubtful Accounts 25,500

1400 Raw Materials 87,000

30. Your Company Name

Trial Balance

December 31, 20X0

1410 Work-in-process 12,000

1420 Finished Goods 132,000

1430 Spare Parts 58,000

1500 Prepaid Insurance 5,400

1510 Prepaid Rent 3,000

1600 Land 570,000

1610 Buildings 430,000

1620 Leasehold Improvements 100,000

1630 Office Equipment 44,000

1650 A/D-Buildings 240,000

1660 A/D-Leasehold Improvements 51,000

1670 A/D-Office Equipment 25,000

1700 Patens 170,000

1710 Trademark 60,000

1750 Accum Amort-Parents 90,000

1800 Investments in Debt Securities 0

1810 Investments in Equity Securities 75,000

1900 Cash Surrender Value Life Insr 54,000

2000 Accounts Payable 285,000

2100 Accrued Payroll 205,000

31. Your Company Name

Trial Balance

December 31, 20X0

2110 Accrued Property Taxes 42,000

2120 Accrued Vacation 323,000

2200 Short-term Bank Loan 245,000

2300 Current Portion of Line of Credit 100,000

2400 State Income Tax Payable 30,000

2410 Federal Income Tax Payable 60,000

2500 Line of Credit (Revolver) 53,000

2510 Term Loan 250,000

3000 Capital 50,000

3010 Current Year Earnings 159,000

3020 Retained Earnings 346,900

Total $ 2,580,400 $ 2,580,400

Note that the total in the Debit column equals the total in the Credit column.

How to prepare balance sheet

4.3. Step 3: Group trial balance accounts by classification

There are more trial balance accounts in Illustration 5 than there are balance sheet classifications

(groups) in Illustration 4. That is because some classifications (groups) may include multiple

trial balance accounts. For example, Cash and Cash Equivalents on the balance sheet template

will include the following trial balance accounts since they have the same nature: Petty Cash,

Chase Checking, PayPal Checking, Savings, and Money Market. Therefore, the next step is to

group all accounts on the trial balance by their respective balance sheet classifications.

32. Here we have added another column to the trial balance where we entered the balance sheet

classification for the accounts. Refer to Illustration 6 below.

4.4. Step 4: Subtotal account balances by classification

The following step is to subtotal the balances in the accounts for each classification. Note that

when subtotals are prepared, all asset balances are calculated as Debit – Credit, while all liability

and equity balances are calculated as Credit – Debit. For example, the subtotal for the balance

sheet classification "Accounts Receivable" is equal to the debit amount in the account 1300,

Accounts Receivable, less the credit balance in the account 1350, Allowance for Doubtful

Accounts (that is, $389,000 - $25,500 = $363,500). Even though the calculations seem to be

complicated, if you use spreadsheet software, it is pretty easy:

Illustration 6: Trial balance with subtotals for balance sheet classifications (groups)

Your Company Name

Trial Balance

December 31, 20X0

Balance Sheet

Acct # Account Name Debit Credit Subtotal

Classification

1000 Petty Cash $ 500

1010 Chase Checking 42,000

Cash & Cash

1020 PayPal Checking 23,500 391,000

Equivalents

1030 Savings 300,000

1040 Money Market 25,000

1200 Marketable Securities 0 Marketable

0

Securities

1300 Accounts Receivable 389,000

Accounts

363,500

Receivable

1350 Allowance for Doubtful Accts 25,500

1400 Raw Materials 87,000

1410 Work-in-process 12,000 Inventories 289,000

1420 Finished Goods 132,000

33. Your Company Name

Trial Balance

December 31, 20X0

1430 Spare Parts 58,000

1500 Prepaid Insurance 5,400

Prepaid

8,400

Expenses

1510 Prepaid Rent 3,000

1600 Land 570,000

1610 Buildings 430,000

1620 Leasehold Improvements 100,000

Fixed

1630 Office Equipment 44,000 828,000

Asset

1650 A/D-Buildings 240,000

1660 A/D-Leasehold Improvements 51,000

1670 A/D-Office Equipment 25,000

1700 Patens 170,000

Intangible

1710 Trademark 60,000 140,000

Asset

1750 Accum Amort-Parents 90,000

1800 Investments in Debt Secs 0

Investments 75,000

1810 Investments in Equity Secs 75,000

1900 Cash Surrender Value Life Insr 54,000 Other Non-current

54,000

Assets

2000 Accounts Payable 285,000 Accounts

285,000

Payable

2100 Accrued Payroll 205,000

Accrued

570,000

Expenses

2110 Accrued Property Taxes 42,000

34. Your Company Name

Trial Balance

December 31, 20X0

2120 Accrued Vacation 323,000

2200 Short-term Bank Loan 245,000 Short-term Loans 245,000

2300 Current Portion of Line of Credit 100,000 Current Portion

100,000

of Long-term Debt

2400 State Income Tax Payable 30,000

Income Taxes

90,000

Payable

2410 Federal Income Tax Payable 60,000

2500 Line of Credit (Revolver) 53,000 Line of Credit 53,000

2510 Term Loan 250,000 Term Loan 250,000

3000 Capital 50,000 Capital 50,000

3010 Current Year Earnings 159,000 Current Year

159,000

Earnings

3020 Retained Earnings 346,900 Retained

346,900

Earnings

Total $ 2,580,400 $ 2,580,400

The final step is to transfer the classification subtotals from the trial balance (Illustration 6) to the balance

sheet template (Illustration 4). For example, we transfer the $391,000 subtotal from the trial balance for

Cash & Cash Equivalents to the identical line on the balance sheet template. The result will be a

completed balance sheet:

35. sIllustration 7: Completed balance sheet template

Your Company Name

Trial Balance

December 31, 20X0

ASSETS

Current Assets:

Cash & Cash Equivalents $ 391,000

Marketable Securities 0

Accounts Receivable 363,500

Inventories 289,000

Prepaid Expenses 8,400

Total Current Assets 1,051,900

Fixed Assets 828,000

Intangible Assets 140,000

Investments 75,000

Other Non-current Assets 54,000

TOTAL ASSETS $ 2,148,900

LIABILITIES

Current Liabilities:

Accounts Payable 285,000

Accrued Expenses 570,000

Short-term Loans 245,000

Current Portion of LT Debt 100,000

Income Taxes Payable 90,000

Total Current Liabilities 1,290,000

Non-current Liabilities:

Line of Credit 53,000

Term Loan 250,000

Total Non-current Liabilities 303,000

TOTAL LIABILITIES 1,593,000

36. Your Company Name

Trial Balance

December 31, 20X0

EQUITY

Capital 50,000

Current Year Earnings 159,000

Retained Earnings 346,900

TOTAL EQUITY 555,900

TOTAL LIABILITIES & EQUITY $ 2,148,900

A few notes about the completed balance sheet:

The subtotals and totals on the balance sheet (i.e. the $1,051,900 for current assets) were

directly determined when all subtotals from the trial balance were transferred to the balance

sheet template.

The total assets of $2,148,900 equal the total liabilities and equity of $2,148,900. However, these

totals don't match the trial balance totals for debits and credits of $2,580,400 (Illustration 6).

The reason these totals don't match is because in the trial balance the totals are calculated for

the debit and credit balances separately. In the balance sheet, though, some credit balances

are subtracted from debit balances and vice versa (i.e. due to contra asset and contra liability

accounts). Therefore, the totals on the trial balance and the balance sheet may not match.

Normally, if a particular balance sheet classification has a zero balance (i.e. Marketable

Securities in Illustration 7), the classification line is not shown. We left Marketable Securities in

there so it is consistent with the balance sheet template (Illustration 4) we prepared earlier.

The line for Marketable Securities can be taken out without any "harm" to the balance sheet.