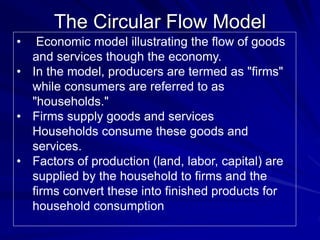

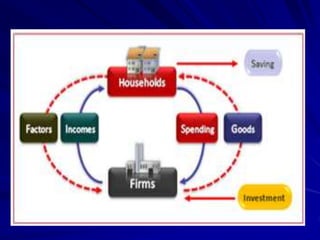

This document provides an introduction to economics concepts. It defines economics as the study of how individuals and societies make decisions about using scarce resources to fulfill wants and needs. It discusses key microeconomics and macroeconomics concepts including factors of production, costs, revenues, different types of economies and the principles of capitalism. The document seeks to explain fundamental economic reasoning and tradeoffs individuals and societies face.

![pabalat ng noli [short]](https://cdn.slidesharecdn.com/ss_thumbnails/nolimetangerepinaikli-120113215245-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)