Download to read offline

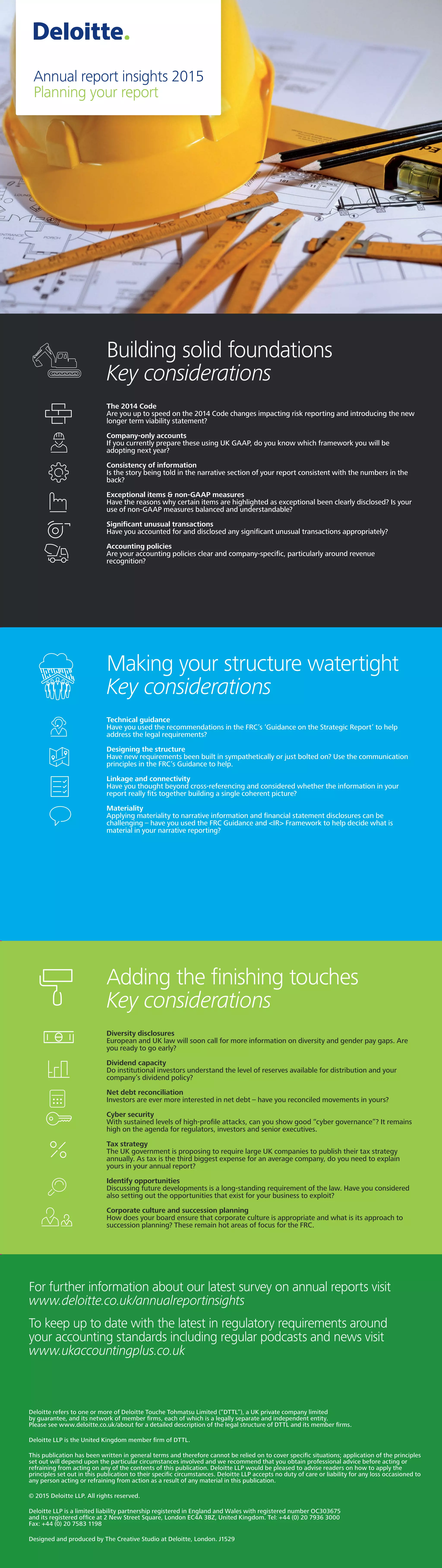

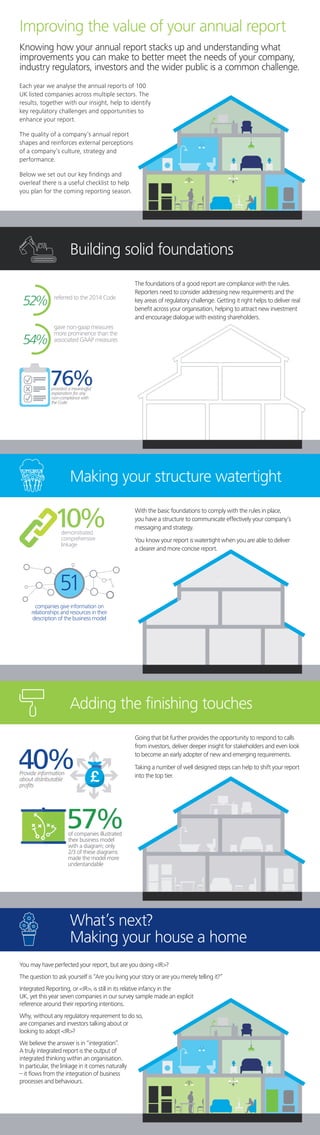

The document outlines best practices and key considerations for creating effective annual reports in compliance with UK regulations, emphasizing the importance of integrated reporting. It highlights specific areas such as materiality, consistency of information, and the need for clear disclosures on matters like diversity and tax strategy. The publication serves as a guide for companies to improve the value of their reports by addressing regulatory challenges and enhancing communication with stakeholders.