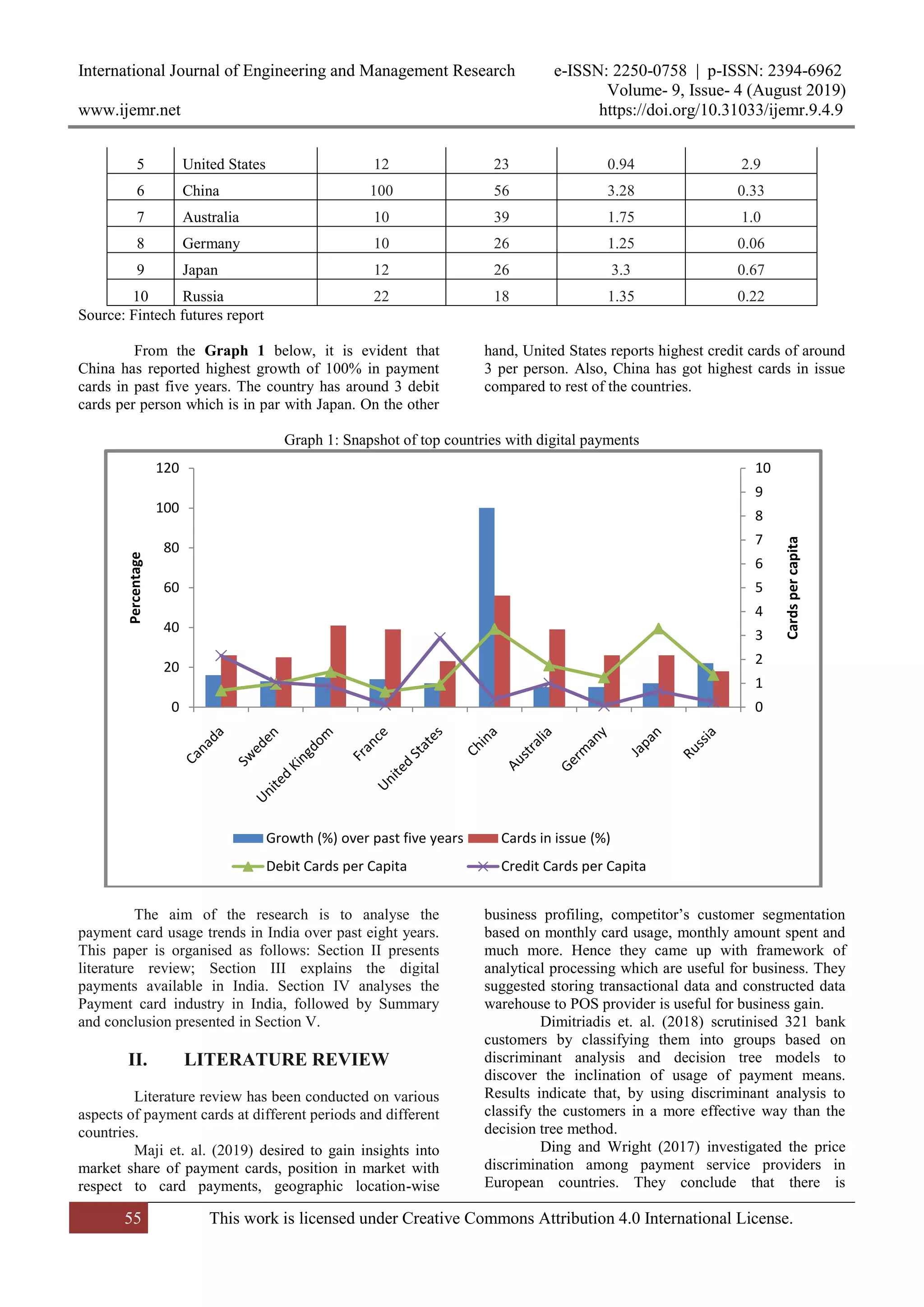

This paper provides an empirical analysis of payment card usage in India from 2011 to 2019, highlighting significant growth in the number of credit and debit cards. The research indicates a threefold increase in credit card penetration and a more than threefold increase in debit card usage, although disparities exist between the two. This trend suggests potential for future expansion in India's payment card market, given its historically cash-dominated economy.

![International Journal of Engineering and Management Research e-ISSN: 2250-0758 | p-ISSN: 2394-6962

Volume- 9, Issue- 4 (August 2019)

www.ijemr.net https://doi.org/10.31033/ijemr.9.4.9

60 This work is licensed under Creative Commons Attribution 4.0 International License.

V. SUMMARY AND CONCLUSION

The study is aimed to analyse the trends of

payment card usage in India. The data was collected from

RBI website for period of eight years from 2011 to 2019.

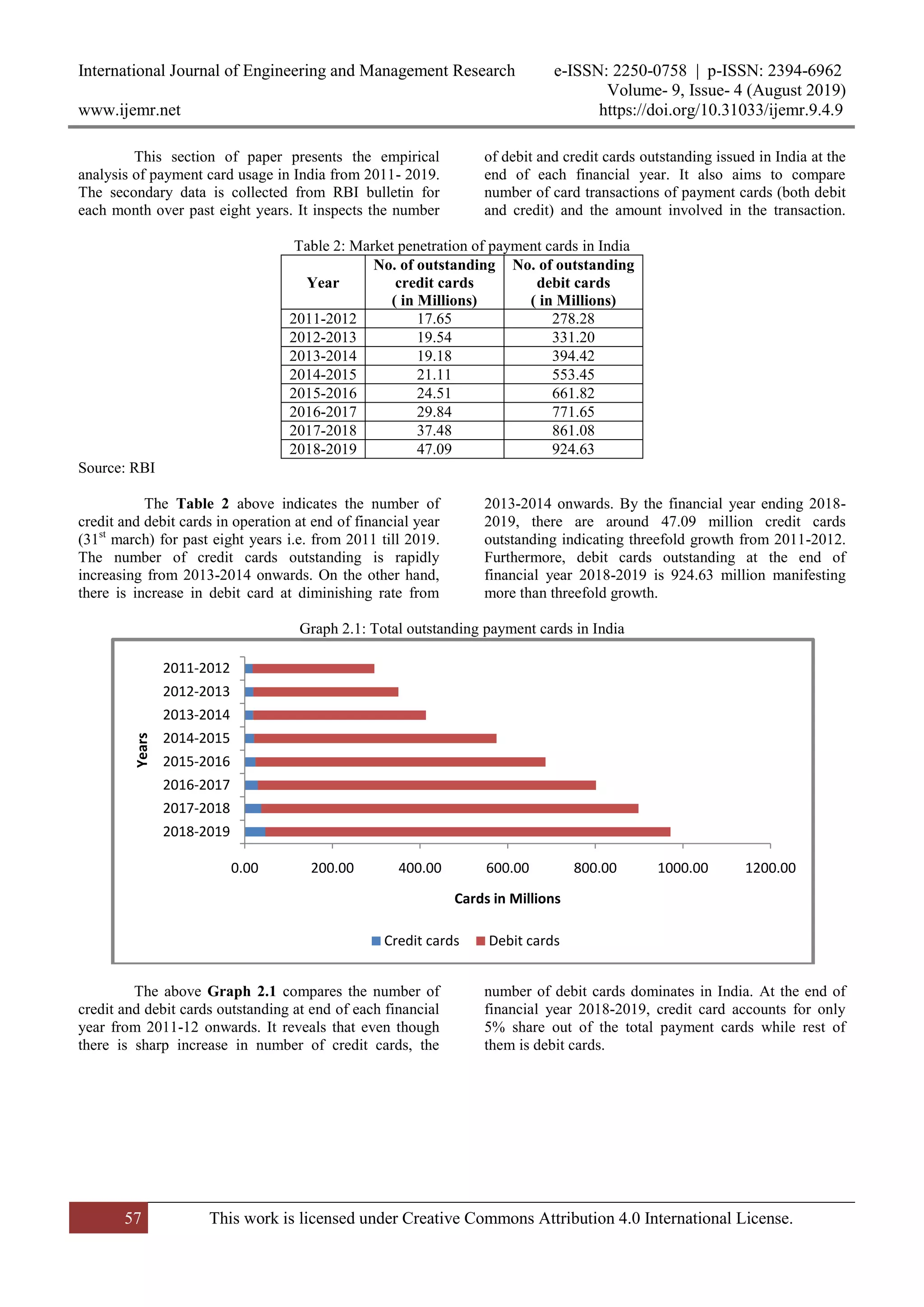

By the financial year ending 2018-2019, there are around

47.09 million credit cards outstanding indicating

threefold growth and debit cards outstanding is 924.63

million manifesting more than threefold growth.

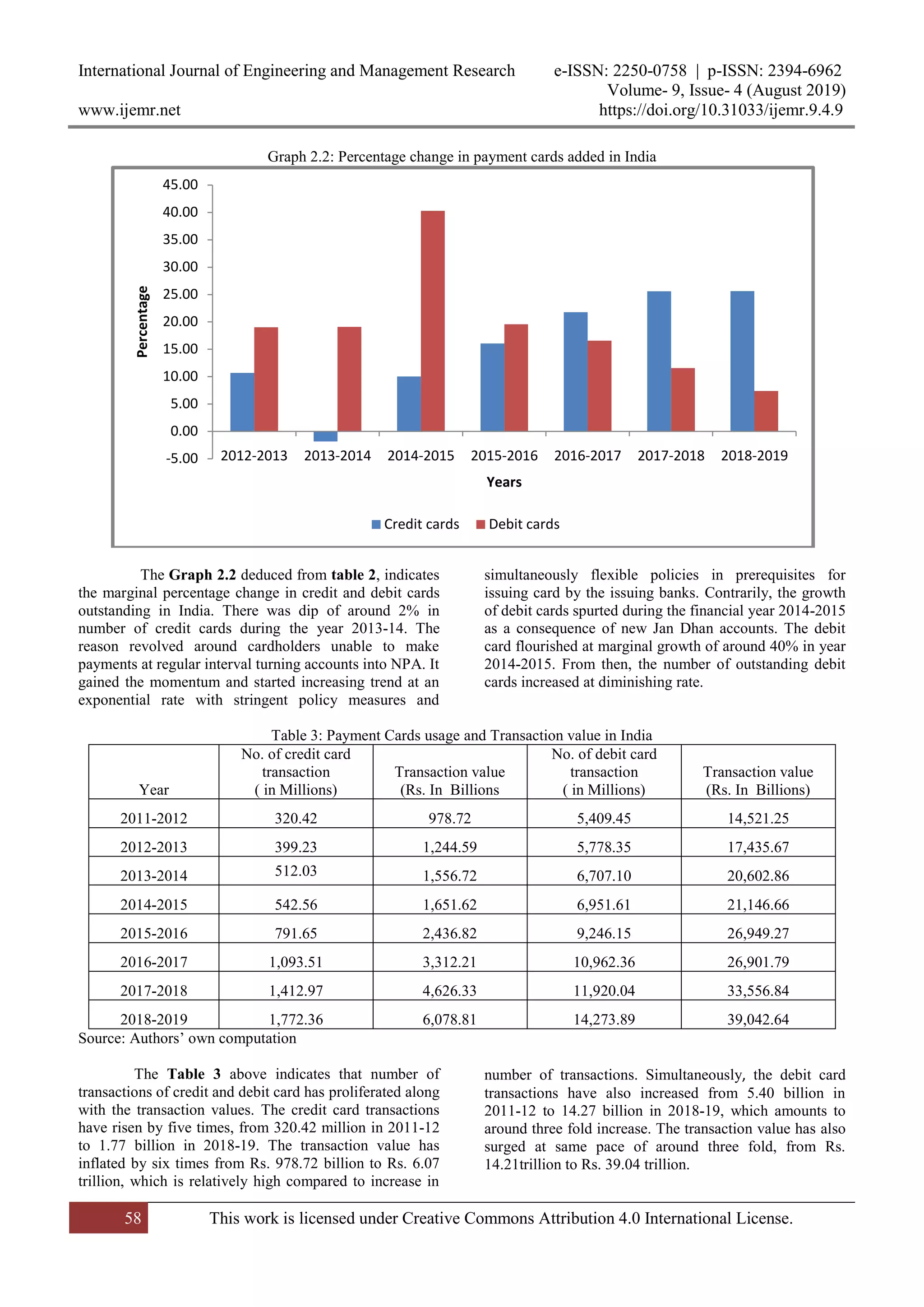

The number of outstanding credit cards is

expanding every year with liberal expansion of credit

limits and prerequisites by bank and stringent measures

by Government. CIBIL, a credit information company

operating in India, provides CIBIL score which is easily

accessible by citizens and credit card issuing institutions.

From the analysis it is evident that there are around 95%

debit cards holders and only 5% credit card holders in

India indicating it is still niche product.

Looking at the report, cardholders (credit and

debit card), transactions, and transaction value have

increased tremendously. The total transaction amount in

debit cards in 2018-19 is consolidated to Rs. 39.04 trillion

and credit cards are consolidated to Rs. 6.07 trillion. The

magnification of debit cards shot up by 40% in the year

2014-15 because of policy implication. The Government

of India undertook national mission of financial inclusion

by opening Jan Dhan accounts and issuing debit cards.

There was dip in transaction value to 0.18% in year 2016-

17, besides remarkable increase in number of operating

debit cards to 18.56%. This was the effect of policy of

restricting amount to be withdrawn and number of

transactions due to demonetization.

The Government of India reported the key

achievement of demonetisation as lower cash-to-GDP

ratio. The cash to GDP ratio is the ratio between the

public debts incurred by the government to its gross

domestic product. The ratio reduced from 12% to 8% due

to reduction of currency circulation to the extent of Rs

3.89 lakhs crore as claimed by Government of India.

According to Nasscom report, still less than 30% of

population in India are unbanked, and hence growth

opportunity is very high. Finally, the question boils down

whether to have cashless economy or less cash economy.

REFERENCES

[1] Agarwal, S., Chakravorti, S., & Lunn, A. (2010). Why

do banks reward their customers to use their credit

cards?. Available at:

https://www.aeaweb.org/conference/2011/retrieve.php?pd

fid=280.

[2] Amromin, G., & Chakravorti, S. (2009). Whither

loose change? The diminishing demand for small-

denomination currency. Journal of Money, Credit and

Banking, 41(2–3), 315–335.

[3] Arango, C. A., Hogg, D., & Lee, A. (2015). Why is

cash (still) so entrenched? Insights from Canadian

shopping diaries. Contemporary Economic Policy, 33(1),

141–158.

[4] Bagnall, J., Bounie, D., Huynh, K. P., Kosse, A.,

Schmidt, T., Schuh, S. D., & Stix, H. (2014). Consumer

cash usage: A cross-country comparison with payment

diary survey data. Available at:

https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1685.p

df.

[5] Borzekowski, R., Elizabeth, K. K., & Shaista, A.

(2008). Consumers’ use of debit cards: Patterns,

preferences, and price response. Journal of Money, Credit

and Banking, 40(1), 149–172.

[6] Carbó-Valverde, S. & Liñares-Zegarra, J. M. (2011).

How effective are rewards programs in promoting

payment card usage? Empirical evidence. Journal of

Banking & Finance, 35(12), 3275–3291.

[7] Chase, M. A. (1991). The credit card industry: A

history. Available at:

https://www.jstor.org/stable/23859431?seq=1#page_scan

_tab_contents.

[8] Dimitriadis, S., Kyrezis, N., & Chalaris, M. (2018). A

comparison of two multivariate analysis methods for

segmenting users of alternative payment means.

International Journal of Bank Marketing, 36(2), 322-335.

[9] Ding, R. & Wright, J. (2017). Payment card

interchange fees and price discrimination. The Journal of

Industrial Economics, 65(1), 39-72.

[10] Evans, D. S. & Schmalensee, R. (2005). Paying with

plastic: The digital revolution in buying and borrowing.

UK: Mit Press.

[11] Kosse, A. & Jansen, D.-J. (2013). Choosing how to

pay: The influence of foreign backgrounds. Journal of

Banking & Finance, 37(3), 989–998.

[12] Koulayev, S., Rysman, M., Schuh, S., & Stavins, J.

(2016). Explaining adoption and use of payment

instruments by US consumers. The RAND Journal of

Economics, 47(2), 293–325.

[13] Maji, G. Dutta, L., & Sen, S. (2019).Targeted

marketing and market share analysis on POS payment

data using DW and OLAP. Emerging Technologies in

Data Mining and Information Security, Springer. DOI:

10.1007/978-981-13-1498-8_17

[14] Rysman, M. (2007). An empirical analysis of

payment card usage. The Journal of Industrial

Economics, 55(1), 1–36.](https://image.slidesharecdn.com/ijemr2019090409-190819082415/75/An-Empirical-Analysis-of-Payment-Card-Usage-in-India-7-2048.jpg)