Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to Almaden Minerals Limited - Cormark Securities

Similar to Almaden Minerals Limited - Cormark Securities (20)

Recently uploaded

Recently uploaded (20)

Almaden Minerals Limited - Cormark Securities

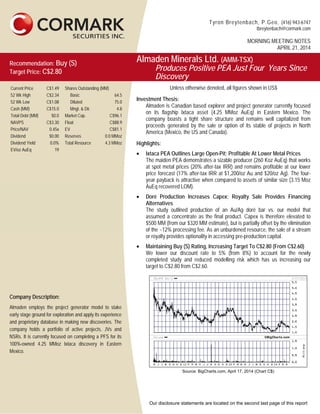

- 1. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014 Our disclosure statements are located on the second last page of this report Recommendation: Buy (S) Target Price: C$2.80 Almaden Minerals Ltd. (AMM-TSX) Produces Positive PEA Just Four Years Since Discovery Current Price C$1.49 Shares Outstanding (MM) 52 Wk High C$2.34 Basic 52 Wk Low C$1.08 Diluted Cash (MM) C$15.0 Mngt. & Dir. Total Debt (MM) $0.0 Market Cap. NAVPS C$3.30 Float Price/NAV 0.45x EV Dividend $0.00 Reserves Dividend Yield 0.0% Total Resource EV/oz AuEq 19 C$96.1 4.3 MMoz C$81.1 0.0 MMoz 64.5 75.0 4.8 C$88.9 Unless otherwise denoted, all figures shown in US$ Investment Thesis: Almaden is Canadian based explorer and project generator currently focused on its flagship Ixtaca asset (4.25 MMoz AuEq) in Eastern Mexico. The company boasts a tight share structure and remains well capitalized from proceeds generated by the sale or option of its stable of projects in North America (Mexico, the US and Canada). Highlights: • Ixtaca PEA Outlines Large Open-Pit; Profitable At Lower Metal Prices The maiden PEA demonstrates a sizable producer (260 Koz AuEq) that works at spot metal prices (20% after-tax IRR) and remains profitable at our lower price forecast (17% after-tax IRR at $1,200/oz Au and $20/oz Ag). The four- year payback is attractive when compared to assets of similar size (3.15 Moz AuEq recovered LOM). • Doré Production Increases Capex; Royalty Sale Provides Financing Alternatives The study outlined production of an Au/Ag doré bar vs. our model that assumed a concentrate as the final product. Capex is therefore elevated to $500 MM (from our $320 MM estimate), but is partially offset by the elimination of the ~12% processing fee. As an unburdened resource, the sale of a stream or royalty provides optionality in accessing pre-production capital. • Maintaining Buy (S) Rating, Increasing Target To C$2.80 (From C$2.60) We lower our discount rate to 5% (from 8%) to account for the newly completed study and reduced modelling risk which has us increasing our target to C$2.80 from C$2.60. Company Description: Almaden employs the project generator model to stake early stage ground for exploration and apply its experience and proprietary database in making new discoveries. The company holds a portfolio of active projects, JVs and NSRs. It is currently focused on completing a PFS for its 100%-owned 4.25 MMoz Ixtaca discovery in Eastern Mexico. Source: BigCharts.com, April 17, 2014 (Chart C$)

- 2. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014 Our disclosure statements are located on the second last page of this report Maiden PEA Confirms Large, Royalty Free Asset With Robust Economics: The most significant change from our original assumption is the decision to produce a doré bar vs. concentrate and use a larger throughput rate. These changes have increased our pre-production capital estimate to $500 MM (from $320 MM) but also allow Almaden to recapture the smelting charge. The project generates a robust return at even our lower metal price assumptions (17% after-tax IRR at $1,200/oz Au & $20/oz Ag) and a solid ~20% after-tax IRR at spot gold prices. Key economic drivers are: Low Strip Ratio: The waste rock (volcanic ash/tuff) has a much lower density than the host rock and combined with the favorable geometry of the ore body translates into strip ratios of just 2:1. Low Cost Jurisdiction: Mexico is well established as a mining-friendly jurisdiction with producers in the region able to demonstrate some of the lowest unit-mining costs in the industry. A decent pool of experienced labor and suppliers is also available. The PEA contractor mining rate of $1.81/t matches other producers in the region (e.g. Timmins Gold, TMM-T, Market Perform rating, C$1.85 target, covered by Kyle McPhee). Robust Recovery: The metallurgy of Ixtaca suggests a clean concentrate without the Lb-Zn values typical seen in most Mexican Ag ores. The company reports that even lower grade silver samples (~15 g/t Ag) recover well. The PEA has defined an improved (90%) recovery rate for both metals following ongoing testing as part of the design work. No Third-Party Line Royalty: As an in-house and “organic” discovery, Ixtaca is unburdened by any third- party top-line royalties, drastically improving economics. Our full list of assumptions is detailed below and we have updated our model following the PEA release. Figure 1: PEA Results & Assumptions CSI old PEA CSI new Long Term Gold Price ($) $1,200 $1,320 $1,200 Long Term Silver Price ($) $20 $21 $20 Tonnes Milled (MMt) 115.8 129 129 AuEq Grade (g/t) 1.14 0.80 0.84 Au Grade (g/t) 0.54 0.42 0.42 Ag Grade (g/t) 30.9 25.27 25.27 Total Mine Life (years) 13 12 12 Average Annual Throughput (tpd) 25,000 30,000 30,000 Average Ag Recovery (%) 80% 90% 90% Average Ag Recovery (%) 78% 90% 90% O/P Mining Costs ($/t of rock) $1.80 1.81 1.81 Strip Ratio W:O 2.00:1 2.00:1 2.00:1 Processing Costs ($/t of ore) $6.20 $9.00 $9.00 G&A Costs ($/t of ore) $2.00 $2.10 $2.10 Refinery Charge (Including Transport) (% of revenue) 12% 0 0 Average Cash Costs ($/oz AuEq) $651 N/A 717 Average All-in Sustaining Costs ($/oz AuEq) $736 N/A 750 Average Gold Equivalent Production (Koz/yr) 239 260 260 Initial Capital ($ MM) $320 $496 $500 Sustaining Capital ($ MM) $90 $106 $106 Total Captial ($ MM) $410 $602 $606 After-tax NPV5% ($ MM) $414 $437 $307 After-tax IRR (%) 27% 22% 17% Sources: Company Reports/Cormark Securities

- 3. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014 During the past twenty-four months, Cormark Securities Inc., either on its own or as a syndicate member, participated in the underwriting of securities for these companies Our disclosure statements are located on the second last page of this report We Expect An Eventual Sale/Spin-out Of Ixtaca: Given the impressive production profile and safe jurisdiction, returns are adequate down to gold prices of $1,200/oz in our view. At our conservative metal price assumptions the after-tax IRR is a moderate 17% though we note that Ixtaca delivers the 4th highest production rate of the group and we exclude any potential tax rebates and rely solely on the new Mexican tax regime ($393 MM total tax burden at $1,200/oz Au & $20/oz Ag) Figure 2: Peer Comparables Sorted By Production Profile Annual Production Company Project NPV IRR NPV IRR ($MM) (%) ($MM) (%) (Koz) ♦ Pretium Resources Brucejack $2,309 54% $3,024 68% 426 Asanko Gold AGM $463 20% $842 31% 325 ♦ Sabina Gold & Silver Back River $152 13% $481 27% 300 Almaden Ixtaca $307 17% $658 28% 260 ♦ Guyana Goldfields Aurora $601 25% $886 33% 194 ♦ Victoria Gold Eagle $232 20% $443 31% 192 Lydian International Amulsar $431 24% $624 30% 186 ♦ Belo Sun Volta Grande $188 9% $561 17% 167 Newstrike Capital Ana Paula $166 20% $331 31% 162 ♦ Dalradian Curraghinalt $315 42% $45 54% 160 ♦ Romarco Haile $750 29% $1,051 36% 126 ♦ Probe Mines Borden $244 18% $434 28% 126 ♦ Kaminak Gold Corp Coffee $92 14% $236 24% 120 ♦ Castle Mountain Castle Mtn $245 26% $404 38% 120 ♦ True Gold Mining Karma $190 40% $300 56% 97 ♦ Sulliden Gold Shahuindo $219 30% $317 42% 85 Midway Gold Pan $90 25% $157 38% 80 Golden Queen Soledad $176 22% $249 28% 80 ♦ Roxgold 55-Zone $140 33% $217 46% 75 ♦ West Kirkland Hasbrouck $73 35% $116 50% 65 $1,200/oz Au & $20/oz Ag $1,400/oz Au & $25/oz Ag Sources: Company Reports/Cormark Securities We suggest the asset may be of interest to mid-tier producers experienced in Mexico and looking to grow production significantly. Obvious candidates include Alamos Gold (AGI-T, not rated) and Pan American (PAA-T, not rated) as both would benefit from a ~260 Koz production boost and have healthy cash balances (Alamos: $410 MM; Pan American: $423 MM) with minimal to no debt. We also note that the asset would likely appeal to producers of both gold and silver as revenue is split equally between the two metals.

- 4. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014 Our disclosure statements are located on the second last page of this report Figure 3: FCF Profile At Cormark Financing Assumptions (65% Equity/35% Debt) -1,200 -800 -400 0 400 800 1,200 -600.0 -400.0 -200.0 0.0 200.0 400.0 600.0 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 Cum.Cash($MM) ($MM) Capex Debt Issuance ($175 MM) Equity Issuance ($325 MM) Interest Payment Debt Repayments Operating Cash Flow (Base Case) Cash at $1,100/oz Au & $18/oz Ag Cash at $1,300/oz Au & $22/oz Ag Cash at $1,200/oz Au & $20/oz Ag Source: Cormark Securities Valuation: Our Ixtaca model now demonstrates an NPV5% of $307 MM after updating our project scope to match the higher throughput rates (30,000 tpd) and flow sheet as laid out in the PEA. We have also switched to a 5% discount rate (previously 8%) to reflect the reduced risk stemming from a published PEA and a resource that is largely (83%) within the higher confidence M&I categories. We maintain our 0.85x NAV multiple but update our dilution assumptions to assume the project is now financed at a 65/35% equity to debt split and that the equity is issued at the current share price. Figure 4: Valuation Summary $MM $/Share Assets Ixtaca NPV5% 306.55 4.09 Caballo Blanco NSR Present Value (7.5%) 8.72 0.12 Remaining Exploration Ground 10.00 0.13 Remaining NSR Portfolio 0.24 0 Corporate Adjustments Cash 15.00 0.20 Pro Forma Cash 325.00 Cash from Warrants/Options 13.13 0.18 Net Asset Value 678.62 3.14 Net Asset Value (C$) C$3.30 Basic S/O 64.49 Options and Warrants Outstanding 10.48 Fully Diluted S/O 74.97 Fully Diluted & Financed S/O 215.80 Current Almaden Share Price ($/sh) C$1.49 Price/NAV 0.45x Source: Cormark Securities

- 5. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014 Our disclosure statements are located on the second last page of this report Upcoming Catalysts: • Drill Results: With $15 MM in cash and equivalents, we expect continuous news flow from the large epithermal gold system at Tuligtic - Ongoing • Potential Asset Sale/Option: Almaden has a successful track record of monetizing its discoveries; we would not be surprised to see a deal that includes Ixtaca or any of the 12 other earlier stage projects. Almaden could then focus on leveraging its proprietary geological database to uncover further economic projects and repeat the success - Ongoing Maintain Buy (S) Recommendation, Increase Target To C$2.80: Almaden’s Ixtaca has evolved into a sizable and robust asset that we expect is monetized to allow the company to focus on what it does best, creating value with the drill bit. Our new valuation methodology has us increasing our target to C$2.80 (from C$2.60) and continues to be based on conservative metal pricing and 0.85x NAV multiple. I, Tyron Breytenbach, hereby certify that the views expressed in this research report accurately reflect my personal views about the subject company(ies) and its (their) securities. I also certify that I have not been, and will not be receiving direct or indirect compensation in exchange for expressing the specific recommendation(s) in this report.

- 6. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014

- 7. Tyron Breytenbach, P.Geo, (416) 943-6747 tbreytenbach@cormark.com MORNING MEETING NOTES APRIL 21, 2014

- 8. MORNING MEETING NOTES APRIL 21, 2014 RECOMMENDATION TERMINOLOGY Cormark’s recommendation terminology is as follows: Top Pick our best investment ideas, the greatest potential value appreciation Buy expected to outperform its peer group Market Perform expected to perform with its peer group Reduce expected to underperform its peer group Our ratings may be followed by "(S)" which denotes that the investment is speculative and has a higher degree of risk associated with it. Additionally, our target prices are set based on a 12-month investment horizon. For Canadian Residents: This report has been approved by Cormark Securities Inc. (“CSI”), member IIROC and CIPF, which takes responsibility for this report and its dissemination in Canada. Canadian clients wishing to effect transactions in any security discussed should do so through a qualified salesperson of CSI. For US Residents: Cormark Securities (USA) Limited (“CUSA”), member FINRA and SIPC, accepts responsibility for this report and its dissemination in the United States. This report is intended for distribution in the United States only to certain institutional investors. US clients wishing to effect transactions in any security discussed should do so through a qualified salesperson of CUSA. Every province in Canada, state in the US, and most countries throughout the world have their own laws regulating the types of securities and other investment products which may be offered to their residents, as well as the process for doing so. As a result, some of the securities discussed in this report may not be available to every interested investor. This report is not, and under no circumstances, should be construed as, a solicitation to act as securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction. This material is prepared for general circulation to all clients and does not have regard to the particular circumstances or needs of any specific person who may read it. This report is provided for information purposes only and does not constitute an offer or solicitation to buy or sell any securities discussed herein. The information and any statistical data contained herein have been obtained from sources believed to be reliable as of the date of publication, but the accuracy or completeness of the information is not guaranteed, nor in providing it does CSI or CUSA assume any responsibility or liability. All opinions expressed and data provided herein are subject to change without notice. The inventories of CSI or CUSA, its affiliated companies and the holdings of their respective directors, officers and companies with which they are associated may have a long or short position or deal as principal in the securities discussed herein. A CSI or CUSA company may have acted as underwriter or initial purchaser or placement agent for a private placement of any of the securities of any company mentioned in this report, may from time to time solicit from or perform financial advisory, or other services for such company. The securities mentioned in this report may not be suitable for all types of investors; their prices, value and/or the income they produce may fluctuate and/or be adversely affected by exchange rates. No part of any report may be reproduced in any manner without prior written permission of CSI or CUSA. A full list of our disclosure statements as well as our research dissemination policies and procedures can be found on our web-site at: www.cormark.com