1. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

All information remains proprietary to the Kenneth Woods Portfolio Management Program and it’s authors

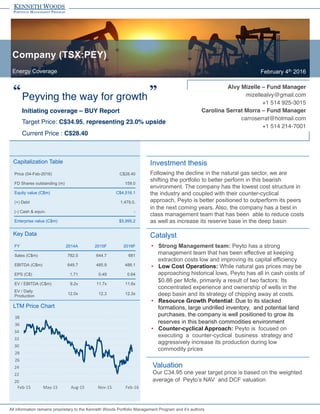

Company (TSX:PEY)

Energy Coverage February 4th 2016

Peyving the way for growth!“ ”

Initiating coverage – BUY Report!

Target Price: C$34.95, representing 23.0% upside!

Current Price : C$28.40!

Investment thesis

Following the decline in the natural gas sector, we are

shifting the portfolio to better perform in this bearish

environment. The company has the lowest cost structure in

the industry and coupled with their counter-cyclical

approach, Peyto is better positioned to outperform its peers

in the next coming years. Also, the company has a best in

class management team that has been able to reduce costs

as well as increase its reserve base in the deep basin

Catalyst

• Strong Management team: Peyto has a strong

management team that has been effective at keeping

extraction costs low and improving its capital efficiency

• Low Cost Operations: While natural gas prices may be

approaching historical lows, Peyto has all in cash costs of

$0.86 per Mcfe, primarily a result of two factors: Its

concentrated experience and ownership of wells in the

deep basin and its strategy of chipping away at costs.

• Resource Growth Potential: Due to its stacked

formations, large undrilled inventory, and potential land

purchases, the company is well positioned to grow its

reserves in this bearish commodities environment

• Counter-cyclical Approach: Peyto is focused on

executing a counter-cyclical business strategy and

aggressively increase its production during low

commodity prices

Valuation

Our C34.95 one year target price is based on the weighted

average of Peyto’s NAV and DCF valuation

LTM Price Chart

Capitalization Table

Key Data

Price (04-Feb-2016) C$28.40

FD Shares outstanding (m) 159.0

Equity value (C$m) C$4,516.1

(+) Debt 1,479.0.

(-) Cash & equiv. -

Enterprise value (C$m) $5,995.2

FY 2014A 2015F 2016F

Sales (C$m) 782.5 644.7 681

EBITDA (C$m) 649.7 485.9 488.1

EPS (C$) 1.71 0.49 0.64

EV / EBITDA (C$m) 9.2x 11.7x 11.6x

EV / Daily

Production

12.0x 12.3 12.3x

Alvy Mizelle – Fund Manager!

mizellealvy@gmail.com!

+1 514 925-3015!

Carolina Serrat Morra – Fund Manager!

carroserrat@hotmail.com!

+1 514 214-7001!

!

20

22

24

26

28

30

32

34

36

38

Feb-‐15

May-‐15

Aug-‐15

Nov-‐15

Feb-‐16

2. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Table of contents

Company History 3

Reserves and Operating Areas 7

Production and Reserve Growth 11

Drilling Locations and Gas Processing 12

Investment Catalyst – Strong Management Team 14

Investment Catalyst – Low Cost Operations 17

Investment Catalyst – Resource Growth Potential 21

Investment Catalyst – Counter-cyclical Approach 23

Valuation – Operating Model 25

Valuation – DCF 28

Valuation – NAV 30

Risks 32

Appendix – Comparable Companies 34

Appendix – Management Team 35

Appendix – Sources 36

3. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

1998-2004

In 1998, Peyto was founded as a growth company focusing on the Cardium

liquids present at Sundance. The company developed a simple but effective

strategy of being a low cost producer in order to generate sustainable returns for

investors regardless of commodity prices. The company decided to focus on the

Sundance region due to the presence of many fundamentals. The Cardium

liquids in this region was very tight, offering a large resource base and a longer

resource life due to its low decline rates. Furthermore, the Sundance region was

also composed of additional resource opportunities composed of multi-stacked

areas that offered Peyto economies of scale. At the time, investors did not fully

believe Peyto regarding their reserve potential (number of wells) mainly since the

technology to extract the oil was not present at the time (only vertical drilling was

available). Despite investor concerns, from 1998 to 2003, the company

successfully grew from a micro-chip to the lowest cost producer in Western

Canada, producing 15,000 boe/d in 2003, with the Sundance region being their

primary growth driver.

In the fourth quarter of 2003, Peyto converted from a corporation to a Trust for

tax advantages and to provide a balanced approach for investors between

growth and income. This move was favourable for the company since the lower

cost of capital complimented its low cost structure and long reserve life (a small

change in cost of capital has a disproportionate change in full life value). The

second reason for adopting a Trust structure was that their drilling program was

becoming less capital efficient as well densities heightened and since they

experienced lower than average drilling results.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Jan-‐1998

Jan-‐1999

Jan-‐2000

Jan-‐2001

Jan-‐2002

Jan-‐2003

Jan-‐2004

Stock

Price

(C$)

Exhibit 1

1998-2004 Stock Price Performance

Company Overview

History

4. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

The Cardium area still had a large amount of resources and reserves but the

pace at which it could be pulled out of the ground was slower as Peyto was

forced to target areas and layers with tighter and tighter permeability. This

caused them to experience lower returns on invested capital and coupled with

the large inflation of services costs; their capital efficiency was deteriorating

quickly. Therefore adopting a Trust structure was due to a combination of cost of

capital advantage combined with management intent to reduce the focus on

growth at a time where marginal rates of return on invested capital had

increased.

2005-2009

The year 2004 remained one where Peyto posted outstanding growth but

2005-2008 really constituted its “dark period” where the more modest capital

efficiencies/modest returns on invested capital became more obvious.

Following 2004, Peyto’s share price performance was a function of the erosion

that was quietly occurring. The company was biding time, awaiting either an

upward shift in natural gas prices to improve returns on invested capital, a new

layer of development big enough and with better returns or a new technical

innovation to drive a fundamental improvement on capital returns. Out of the

three elements, the latter of these became the driver of Peyto’s growth after

2008.

22,245

22,250

21,134

20,191

19,133

42,100

40,300

26,500

33,100

-‐

7,500

15,000

22,500

30,000

37,500

45,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

2005A

2006A

2007A

2008A

2009A

Capital

efficiency

($/boe/d)

ProducMon

(boe/d)

ProducMon

Capital

Efficiency

Exhibit 2

2005-2009 Production and Capital Efficiency

Company Overview

History

5. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

2009-2015

In 2009 Peyto introduced multi-stage development drilling in order to expand its

resource base. The impact of this new technology was almost immediate and

reflected that Peyto’s resource potential was still large but that they needed to

find higher capital returns from higher commodity prices or better capital

efficiency. Horizontal multi-stage fracking delivered significantly better capital

efficiencies and enabled them to grow their production faster as shown by the

graph below:

39,399

49,754

67,296

83,251

85,620

17,500

17,600

15,100

16,800

12,000

-‐

4,000

8,000

12,000

16,000

20,000

-‐

20,000

40,000

60,000

80,000

100,000

2011A

2012A

2013A

2014A

2015F

Capital

efficiency

($/boe/d)

ProducMon

(boe/d)

ProducMon

Capital

Efficiency

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Jan-‐2004

Jan-‐2005

Jan-‐2006

Jan-‐2007

Jan-‐2008

Jan-‐2009

Jan-‐2010

Jan-‐2011

Stock

Price

(C$)

Exhibit 4

20011-2015 Production and Capital Efficiency

Company Overview

History

2004-2011 Stock Price Performance

Exhibit 3

6. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Jan-‐2009

Jan-‐2010

Jan-‐2011

Jan-‐2012

Jan-‐2013

Jan-‐2014

Jan-‐2015

Jan-‐2016

Stock

Price

(C$)

This global improvement in capital efficiency was a positive to all producers in

the beginning but too much of a good thing can also become a bad thing. The

potential for horizontal multistage fracking to improve marginal economics in

virtually all pre-existing resource developments, at the same time fracking

liberated previously trapped resources, created too much resource potential.

This caused the North American market to be flooded with natural gas, causing

natural gas prices to collapse. Now the company is using its proven counter-

cyclical approach to grow reserves aggressively in a depressed natural gas price

environment to generate superior shareholder returns.

Exhibit 5

2009-2016 Stock Price Performance

Company Overview

History

7. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Peyto’s land base covers 400,000 net acres of land located in the heart of the

Deep Basin of west central Alberta. The company has two core areas of

operations: The Sundance and Brazeau region. In terms of specific operating

areas, Peyto is focused on the Spirit River group including the Wilrich, Notikewin

and Falher, with the Bluesky emerging as the next area of growth. As of

FY2014, approximately 36% of total corporate production comes from the

Wilrich, with 24% from the Falher, 14% coming from the Notikewin and 13% from

the Cardium. Peyto is one of the most active drillers in the Deep Basin and has

amassed an inventory of greater than 1,300 locations. The Deep Basin is known

for its high heat content natural gas and as a result, the company receives a

premium for the natural gas it produces.

Reserves and

Operating Areas

Peyto Lands

Exhibit 6

2014 Total

Production of

76,372 boe/d

8. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Greater Sundance Overview

The Greater Sundance area, which includes Sundance, Oldman, Wildhay,

Nosehill and Ansell, is Peyto’s largest producing area focused on the stacked

multi-zone potential including the Cardium, Viking, Notikewin, Falher, Wilrich,

Bluesky, and Cadomin formations. The Company currently owns five facilities

in the area with total processing capacity of ~545 Mmcf/d.

Brazeau River Overview

Peyto’s relatively new core area resides at Brazeau River where the

Company has assembled ~116 gross sections (114 net) of land with current

operations focused on the Wilrich formation. Peyto now has over 40 Mmcf/d of

sweet gas processing capacity at Brazeau and, as of October 2014, completed a

23 km gathering line linking Peyto’s Brazeau gas plant to its south acreage.

Highlighted in the map below, Peyto has realized significant drilling results from

the Wilrich with peak IP30 rates averaging 642 boe/d.

Reserves and

Operating Areas

Great Sundance Area Overview

2014

Production of

~70,000 boe/d

Exhibit 7

9. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Reserves and

Operating Areas

Brazeau River Overview

Exhibit 8

2014

Production

of ~2,000

boe/d

Exhibit 9

Returns and IRR per Region

Sub-Operating Areas

In terms of operating areas, the company classifies tem as the Cardium,

Notikewin, Upper Falher, Middle Falher, Wilrich, Bluesky, Brazeau Falher and

Brazeau Wilrich. As shown in the table below, the company generates a high

lRR for all of its operating areas, with the Bluesky and Upper-Falher

representing the highest IRR’s areas with 43% and 48% IRR respectively

Upper Middle

Brazeau

Brazeau

Cardium Notikewin Falher Falher Wilrich Bluesky Falher

Wilrich

All

Costs (in

C$

mm) 4,650 5,450 5,250 5,350 5,450 5,350 5,750 5,950

IRR (in

%) 22% 28% 48% 22% 23% 43% 32% 20%

NPV10 (in

C$

mm) 1,861 2,930 4,810 2,275 2,676 4,407 3,543 2,168

Peyto

Internal

Full

Cycle

Economics

10. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Advantage of drilling in the deep basin

The deep basin is known for producing high heat content gas from multiple

producing horizons. Also, the lack of water in the formations is another draw for

producers as it eliminates the need for handling or disposal of water, which

again, helps in reducing operating costs. As gas prices started to rise in the late

1990s and early 2000s, interest in the Deep Basin started to grow. Historically

the play was drilled using vertical wellbores and often targeting more than one

formation; however, many formations were viewed as being too tight to actually

produce. As technology evolved over the past six years, producers started to drill

horizontal wells and applied multi-stage fracture completions. This technology

has been further refined and since 2010, Peyto has moved to the point that all its

wells are now drilled horizontally with multiple fracture stimulations.

Activity levels in the Deep Basin have been relatively high since the late 1990s,

but the evolution of drilling technology has further increased interest in the area.

Where some formations were previously viewed as too tight to be a stand-alone

producer, these are now among the most prolific wells in the area due to the

formations’ relative thickness and the ability to tap incremental gas through

fracture stimulation of horizontal wellbores. Peyto has moved to pad drilling in

the Deep Basin with four formations off of a single pad. The company’s main

focus for 2016 is on the Spirit River. The Spirit River also has less variation in

rates between wells. A typical Peyto well in the Deep Basin will have a 1,200m

long horizontal leg with 150m frac spacing and an 80 ton frac. Average well costs

are between C$4.05 – 4.5 million including facility expenditures, full cycle costs

are C$4.6 – 5.1 million/well.

Reserves and

Operating Areas

Exhibit 10

Deep Basin Geological Overview

11. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Reserve Growth by Region

As shown in the graph below, since horizontal drilling was introduced, Peyto has

consistently increased its daily production. From 2010 to Q3 2015, the company

increased daily production from ~20,000 Boe/d to ~90,000 Boe/d. The main

areas of growth has been the Wilrich and Falher regions which have shown 38%

and 22% 5 year CAGR growth respectively.

Acreage Growth

Furthermore, the company has also been increasing its acreage in the deep

basin to take advantage of land sales in Alberta. From 2010 to 2014, the

company has successfully increased its net acreage from 200K to 438K acreage.

With potential land expiries in the next years, the company will have further

opportunities to increase its acreage position in the Deep Basin.

820

11,500

13,500

8,000

18,800

33,000

-‐

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2005A

2006A

2007A

2008A

2009A

2010A

2011A

2012A

2013A

2014A

2015F

ProducMon

(boe/d

Wilrich

Noitkiwen

Falher

Cardium

Bluesky

Other

Production and

Reserve Growth

Exhibit 11

Reserve Growth by Region

12. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Drilling Locations and

Gas Processing

Drilling Areas

In 2014, Peyto completed a C$690 million capital program that included

drilling 125 horizontal wells and expanding corporate processing capacity to

over 100 Mmcf/d. On an annual basis, Peyto targets ~15% of its budget to be

invested on facilities. As highlighted in the table below, Peyto has booked 628

future horizontal drilling locations as of December 31, 2014, and identified over

1,700 total future horizontal drilling locations

Drilling Areas and Expected Completions

Exhibit 13

10.0

20.0

40.0

80.0

140.0

180.0

200.0

210.0

220.0

205.0

225.0

260.0

280.0

370.0

410.0

438.0

--

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

1999A 2000A 2001A 2002A 2003A 2004A 2005A 2006A 2007A 2008A 2009A 2010A 2011A 2012A 2013A 2014A

NetLands(in000'sacres)

Exhibit 12

Peyto 1999-2014 Acreage Growth

Asset VT

Wells HZ

Wells

HZ

Locations

Booked

HZ

Locations

Unbooked

Badheart -‐ -‐ -‐ 56.0

Cardium 432.0 63.0 200.0 356.0

Dunvegan 5.0 1.0 5.0 -‐

Peace

River 1.0 -‐ -‐ 14.0

Notikewin 90.0 56.0 87.0 43.0

Falher 7.0 27.0 37.0 23.0

Falher -‐ 27.0 56.0 254.0

Wilrich 14.0 136.0 179.0 192.0

Bluesky 4.0 14.0 47.0 48.0

Gething 12.0 2.0 -‐ -‐

Cadomin 87.0 2.0 16.0 177.0

Total 652.0 328.0 628.0 1,163.0

Completed Remaining

13. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Drilling Locations and

Gas Processing

Fully Owned Gas Plants

Infrastructure has played a significant role in Peyto’s strategy from the beginning.

The company started with the ownership of its Sundance gas plant and today,

the company owns seven gas processing facilities with 730 Mmcf/d net capacity.

The company maintains operatorship of 98% of its production and processes

96% of those volumes. Early in the company’s history, there was a significant

amount of concern/criticism surrounding the concentration of the company’s land

base and its reliance on a sole gas plant at Sundance. By staying focused, the

company has been able to maintain best in class operating costs, enabling them

to generate superior netbacks. Through the construction of additional plants, the

company has not been reliant on a single processing facility for over a decade,

but has managed to maintain higher operatorship of its production and

processing as displayed below.

Gas Plants and Ownership

Exhibit 14

(in

mmcf/d) 2014

YE 2015

YE 2016

YE WI

Oldman 125.0 125.0 125.0 100%

Nosehill 125.0 125.0 125.0 100%

Wildhay 90.0 90.0 90.0 100%

Galloway 60.0 60.0 60.0 100%

Oldman

North 80.0 120.0 120.0 100%

Kakwa 35.0 45.0 35.0 100%

Swanson 65.0 120.0 150.0 100%

Brazeau 40.0 60.0 120.0 100%

Cubank 10.0 5.0 5.0 100%

Total 630 730 825 98%

Peyto

Gas

Plants

14. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Jan-‐1998

Jan-‐2001

Jan-‐2004

Jan-‐2007

Jan-‐2010

Jan-‐2013

Jan-‐2016

Stock

Price

(C$)

Investment Catalysts

Strong Management focused

on Shareholder growth

Strong Management focused on Shareholder growth

Peyto has a strong management team led by Darren Gee who has been the

CEO since January 2007. Over the years, management has been effective at

preserving the company’s capital by keeping extraction costs low, increasing its

capital efficiency as well as by applying a counter-cyclical approach. In the

industry, due to the depleting nature of an E&P company’s assets many

producers feel the pressure to pursue growth and add production and reserves

without focusing on costs and as a result generate lower returns. However,

Peyto’s management has a completely different approach to managing its E&P

assets as described by its CEO: "At Peyto, we have always relied on an estimate

of the IRR of a project to determine whether or not we proceed and also to look

back at the success of that decision. Our strategy has always been to focus on a

select type of investment that we feel yields the most predictable and repeatable

returns and is accompanied by the lowest cost structure so as to be the least

sensitive to commodity price variability. These opportunities also deliver the

production stream over a very long period of time so as not to expose the entire

resource to any one time price."

Therefore, the company develops and produces assets when service costs are

low, and is comfortable putting the brakes on growth when it's not profitable.

From 2006 to 2010 daily production was roughly static/declining slightly, which

was the result of a conscious decision to limit capex since they weren't seeing

the returns they wanted (capital efficiency was over $40,000 in 2005 and 2006,

comparatively was around $17,400 from 2010 onwards, with management

guidance set for $12,000 in 2015). This is expressed by CEO Darren Gee: "It

was diminishing returns and capital efficiency that caused us to curtail our capital

program which resulted in smaller production adds and declining corporate

production. In other words, exercising capital discipline was the real reason". The

company has stuck to this strategy since its creation and has enabled the

company to generate 95% Shareholder IRR and a 50% CAGR since inception

as displayed below

Peyto Share Performance since Inception

Exhibit 15

15. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Strong Management focused

on Shareholder growth

Contrary to industry practices of growing for the sake of growth, the company

has been able to grow its reserves and production. This has enabled the

company to increase its cash flow per share significantly from C$1.80/share in

2009 to a forecasted C$3.99 in 2015

Dividends

By applying its low cost strategy, the company has generated superior levels of

cash flow, allowing them to increase the amounts of dividends paid to

shareholders. Peyto currently distributes a monthly dividend of C$0.11/share

which equates to an annual cash commitment of ~C$203 million. In

November 2014, Peyto increased its monthly dividend by 10% to $0.11/

share which was the third dividend increase for Peyto in the last two

years. The company is also able to sustain its dividend payout by generating

superior cash flows during the depressed natural gas environments in the past

few years. As shown in the graph below the company has been able to

significantly increase its dividends paid as earnings increased.

Cash Flow Growth per Share

Exhibit 16

Dividend Growth

Exhibit 17

0.04

0.05

0.06

0.07

0.08

0.09

0.1

0.11

0.12

Mar-‐2011

Mar-‐2012

Mar-‐2013

Mar-‐2014

Mar-‐2015

Dividend

per

Share

1.80

1.85

2.18

2.02

2.74

4.19

3.99

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2009A

2010A

2011A

2012A

2013A

2014A

2015F

Cash

Flow

per

Share

16. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Strong Management focused

on Shareholder growth

Focus on ROE and ROCE

Management centers all its capital allocation decisions on the potential IRR the

company could generate. By keeping production and development costs at low/

decreasing levels, the company has been able to generate higher than industry

averages in terms of ROE and ROCE. As shown below, in every year, the

company has been able to generate higher than industry levels of ROE and

ROCE. Due to the depressed commodities environment, service costs are

expected to remain at all-time lows in the coming years, allowing the company to

further develop its reserves at low costs, and to maintain high levels of ROCE

and ROE

Peyto 2008-2014 ROE and ROCE Performance

2008A 2009A 2010A 2011A 2012A 2013A 2014A

Peyto

Comps

ROE -‐ 26% 28% 14% 8% 12% 19% 16% 4%

ROCE -‐ 14% 17% 10% 6% 8% 11% 10% 5%

Peyto

ROCE

&

ROE

vs.

Peers

5-‐Yr

Average

Exhibit 18

17. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Low cost operations

Stable/declining Low All in Cash Costs

While natural gas prices may be approaching historical lows, Peyto has healthy

margins and a strong balance sheet. Over the past five years, the company has

generated average EBITDA margins of 81% and 83% in 2013 and 2014

respectively. The company is able to generate higher margins and all in cash

costs of $0.86 per Mcfe, primarily a result of two factors: Its concentrated

experience and ownership of wells in the deep basin and its strategy of chipping

away at costs.

By concentrating its operations in the Deep Basin, the company has been able to

gain experience in developing wells at low costs. They have been operating in

this formation for over 15 years, and because they operate almost all of their

production (instead of sharing responsibilities with partner companies or

pursuing inorganic growth), the simple compounding of experience and trial and

error has allowed them to become very specialized operators in the region,

essentially developing a wealth of knowledge in drilling Deep Basin formations.

This gives Peyto a large advantage in the industry since understanding how to

drill a formation is a nuanced process; understanding the formation's

permeability, getting the right frac solution mix and understanding how to frac the

formation are some points where heavy experience in a specific set of layers

help.

Also, over the years, the company has been “chipping away” at costs. Through

the President's Monthly Reports you can pick up on a culture of continuously

looking for and making marginal cost improvements that add up. The company is

willing to cut back production to capture better royalty rates, switching drilling rigs

and transport trucks from diesel to gas-based by providing filling stations,

developing drilling pads that save money and boost IRRs and the installation of

its own processing and deep-cut facilities are some of the initiatives CEO Darren

Gee discusses. They've also managed to control G&A costs pretty effectively by

keeping the management team surprisingly small for a company of their size (50

employees), producing 1,589 boe/d/employee for FY2014, five times more

efficient than the 309 boe/d/employee median for peers (does not include field

employees)

Peyto Operating Costs

Exhibit 19

(in

C$

mm) 2008A 2009A 2010A 2011A 2012A 2013A 2014A

Extraction

Costs

(royalties,

opex,

transport) 2.36 1.15 1.12 1.01 0.75 0.78 0.84

PDP

NPV-‐0

Recycle

Ratio 2.1x 5.4x 3.5x 2.4x 1.6x 1.5x 1.5x

Peyto's

Lean

Cost

Structure

18. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Low cost operations

For example, in one of their biggest operating areas, the company has been

slowly chipping away at costs. In the Sundance region, the company has been

able to reduce average drilling costs from ~C$3.1 million per well in 2009 to ~C

$2 million per well in Q3 2015. The company has been able to decrease average

drilling costs all the while increasing its number of wells from 2 in 2009 to 30 in

Q3 of 2015. Also, the company has also reduced its number of days to reserve

replacement from 34.5 days to 17.8 days.

Operating Costs vs. Industry

The company has done an excellent job of keeping all-in cash costs at low/

declining levels by accelerating production in a period where service costs are

low. The company’s drilling and completion (D&C) costs declined from C$4.5

million a few years ago to closer to C$3.0 million. The company maintains the

lowest operational expenses compared to its peers and is the only producer

below $2.00/boe. Given depressed natural gas prices, maintaining the lowest

operating cost structure in its peer group gives Peyto an advantage in delivering

economic returns. As previously mentioned, the low operating costs can be

attributed to its concentrated asset base and ownership of its facilities. As shown

in the graph below, Peyto was by far the lowest cost (operating + transportation)

natural gas producer in the WCSB, with only Advantage Oil & Gas currently

reaching a similar cost structure. What is also important to highlight is that Peyto

has executed its low operating cost structure business model for over 15 years

and was the lowest cost producer in all of those years.

2009-Q3 2015 Greater Sundance Region Drilling Costs

Exhibit 20

3,193

2,926

2,804

2,752

2,792

2,681

2,443

1,939

2,070

4,066

3,999

4,152

4,155

4,268

4,299

4,409

4,227

4,252

34.5

29.3

23.6

21.6

22.5

21.8

20.6

16.7

17.8

0

5

10

15

20

25

30

35

40

-‐-‐

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2009A

2010A

2011A

2012A

2013A

2014A

Q1

2015

Q2

2015

Q3

2015

Drill

&

Case

Cost

/

Depth

Avg

Drill

Cost

Avg

Days

to

RR

Avg

TD

19. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Low cost operations

By utilizing a low cost natural gas approach, the company has been able to

deliver a 1.8x recycle ratio (measured as netback/F&D costs) over the last three

years, which is impressive in the context of weak gas prices. This translates into

better‐than‐average returns on investment and should continue in the coming

years.

Exhibit 21

Industry Operating Costs

Exhibit 22

2006-2014 Peyto FD&A costs and Recycle Ratios

0

2

4

6

8

10

12

14

16

2000A

2001A

2002A

2003A

2004A

2005A

2006A

2007A

2008A

2009A

2010A

2011A

2012A

2013A

2014A

2015F

OperaMng

Costs

incl.

Transp.

($boe)

Trilogy

Perpetual

Paramount

Tourmaline

Bonavista

Advantage

Birhcliff

Average

Peyto

Flat for the past 8 years

17

9

23

8

13

11

11

10

9

25

18

22

20

22

23

24

23

23

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

4.5x

0

5

10

15

20

25

30

2006A

2007A

2008A

2009A

2010A

2011A

2012A

2013A

2014A

All-‐in

Recycle

RaMo

OperaMng

netback

(in

C$

/

boe)

All-‐in

FD&A

Cost

Peer

Group

Median

FD&A

costs

All-‐in

Recycle

RaMo

20. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Low cost operations

Even with growing Production, the company has been able to increase its

capital efficiency

From 2005-2008, high service costs and drilling less economical areas

significantly decreased the company’s capital efficiency. As previously

mentioned, Peyto established the company to control infrastructure and in turn

keep costs low; however, by 2005/2006, the model started to be tested. Although

operating costs were still best in class, its production addition costs were

escalating. The company’s drill bit production addition costs rose from C$24k/

Boe/d in 2004 to C$46k/Boe/d in 2005 and $48k/Boe/d in 2006. During this time,

Peyto recorded production addition costs that were higher than its Royalty Trust

peers on a both a drill bit and all-in basis. Following 2008, the company was able

to significantly decrease its capital costs with the introduction of horizontal

drilling. This enabled the company to drill more economical wells and coupled

with the decline in service costs, the company’s capital efficiency improved

significantly. Their capital efficiency improved significantly from 34k/Boe/d in

2008 to 18k/Boe/d in 2009 and is expected to be at 12k/Boe/d at the end of

2015. At the same time, the company has been able to increase its production

from 30,600 Boe/d in 2010 to a forecasted ~86,620 boe/d in 2015. Even with the

company expected to increase its production significantly as natural gas prices

remain low, the company is forecasted to maintain/increase its capital efficiency.

Exhibit 23

2010-2015 Capital Efficiency and Production

28,197

39,399

49,754

67,296

83,251

85,620

17,300

17,500

17,600

15,100

16,800

12,000

-‐

4,000

8,000

12,000

16,000

20,000

-‐

20,000

40,000

60,000

80,000

100,000

2010A

2011A

2012A

2013A

2014A

2015F

Capital

efficiency

($/boe/d)

ProducMon

(boe/d)

ProducMon

Capital

Efficiency

21. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Resource Potential

Large resources potential concentrated and stacked that can be developed

with modern horizontal MSF.

Peyto’s land base is one of the most concentrated for an intermediate company

of this size, the drilling inventory is much greater than the acreage position would

suggest due to the stacked potential in the Deep Basin. The multi-zone potential

is consistent throughout the majority of Peyto’s acreage with the potential to

increase the liquids yield, decrease cost further as well as drilling optimization. In

most instances, Peyto will produce both natural gas and liquids from a

combination of formations within a particular play. The multi-zone offers

management the ability to divert capital in an attempt to capitalize on commodity

trends/economics within different core areas. The company currently counts

more than 1,300 horizontal drill locations, of which two‐thirds are unbooked. To

put this into perspective, the company expects to drill ~100–115 net locations in

2014. Due to the company’s low‐cost asset base, the resulting capital

efficiencies are attractive at less than C$18,000/boe/d. .

Exhibit 24

Stacked Formations

22. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Ability to purchase more land due to depressed prices and land expiries

In Alberta 2010 and 2011 were record land sales. However, successful bidders

have two–five years, depending on the region of the province, to satisfy

“License and Lease Continuation & Validation” requirements to evaluate or prove

productivity of hydrocarbons. If companies are not able to meet these

requirements, the land is surrendered and returned to the Crown land bank for

future sale. Due to the current depressed commodity price environment,

Peyto will have the opportunity to accumulate significant acreage additions

from Crown land sales over the next 24 months at attractive prices

Investment Catalysts

Resource Potential

Exhibit 25

Undrilled Locations

Exhibit 26

Asset VT

Wells HZ

Wells

HZ

Locations

Booked

HZ

Locations

Unbooked

Badheart -‐ -‐ -‐ 56.0

Cardium 432.0 63.0 200.0 356.0

Dunvegan 5.0 1.0 5.0 -‐

Peace

River 1.0 -‐ -‐ 14.0

Notikewin 90.0 56.0 87.0 43.0

Falher 7.0 27.0 37.0 23.0

Falher -‐ 27.0 56.0 254.0

Wilrich 14.0 136.0 179.0 192.0

Bluesky 4.0 14.0 47.0 48.0

Gething 12.0 2.0 -‐ -‐

Cadomin 87.0 2.0 16.0 177.0

Total 652.0 328.0 628.0 1,163.0

Completed Remaining

Potential Land Sales

23. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Counter-Cyclical Approach

Peyto is focused executing a counter-cyclical business strategy, which is

only executable due to its low operating cost structure as discussed in its

corporate presentation “history has shown us that when natural gas and oil

prices rise, so too do service costs and industry activity levels. This results in

much greater development costs and effectively the same rates of return being

generated for higher natural gas prices. The problem is that prices tend to be

cyclical and do not necessarily stay high to justify higher development costs.”

Part of the reason they're able to execute this strategy is because even in really

low gas price environments, Peyto is still making healthy IRRs and a good level

of operating cash flow to fund part of their capital program.

Peyto employs a counter-cyclical investment strategy and invests aggressively

when gas prices are low, ensuring costs are also at their lowest and returns are

at their highest. With its counter-cyclical strategy, Peyto drilled a record number

of wells in Q3 2015(40), leading the company to hit the 100,000 boe/d mark for

the first time in its history. With 104 net wells drilled in the first 9 months of 2015,

Peyto has already drilled more wells than in all of 2013 (99) and has done so at

an average D&C cost savings of 22%. This is expressed by Thomas Gee: "So

Peyto's low costs mean we're well insulated from commodity price volatility. What

does that really mean though? If we slow down and behave in a very defensive

manner during periods of low commodity prices, much like everyone else in the

industry, having that insulation doesn't really do much for us. Where it becomes a

significant advantage, however, is if it allows us to take the opposite tactic. If we

aggressively deploy capital in the low commodity environment, much like we've

being doing for the last few years, then we are levering off this low cost

advantage to improve the returns on that capital. Things will cost less, dollars will

go further, and the returns we generate on the same kind of well will be even

better at a lower capital cost.” As shown by the graph below, the company has

significantly increased its production as natural gas prices have been declining.

As natural gas prices declined by more than 20%, annual production went from

39,399 boe/d in 2010 to a forecasted 85,620 boe/d in 2015.

Exhibit 27

0

2

4

6

8

10

12

14

-‐

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2001A

2002A

2003A

2004A

2005A

2006A

2007A

2008A

2009A

2010A

2011A

2012A

2013A

2014A

2015F

AECO

Natural

Gas

Price

($/GJ)

ProducMon

(boe/d)

Natural

Gas

ProducMon

/boe/d)

Liquids

ProducMon

(boe/d)

Aeco

Price

($/GJ)

2001-2015 Production and Natural Gas Prices

24. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Investment Catalysts

Counter-Cyclical Approach

Peyto also distinguishes itself with a counter‐cyclical approach to the

development of its asset base to optimize the return on capital employed. As gas

prices rise, the company directs a higher proportion of the incremental cash flow

to dividends and debt repayment, opting to minimize the impact of the associated

increase in drilling and service costs as activity levels pick up across the basin.

The combination of low costs and premium pricing translates into better‐than‐

average netbacks for Peyto as a gas producer which, when combined with its

top‐quartile F&D costs, allows the company to achieve a benchmark recycle

ratio of 2.0x at current gas prices.

Profitable despite decline in prices

Even if natural gas prices have been severely depressed over the past couple of

years, Peyto has been able to generate healthy margins and netbacks. The

company has been able to generate netbacks of C$4.19/mcfe and C$3.65/mcfe

in the past in 2013 and 2014. This is a direct result of the company's low cost

structure as well as its counter cyclical approach which takes advantage of low

service costs. As commodity prices are expected to remain depressed in the

coming years, we see this trend continuing as well as increased investments to

increased production and reserves.

25. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Production Profile

In order to forecast the company’s production profile, an analysis was completed

based on the company’s projected capital expenditures, decline rates and

management expectations for future years production. The company currently

produces mainly natural gas and is expected to increase its daily production from

~500 Mmcfe/d in 2014to 853 Mmcfe/d at the end of 2020.

Commodity Price Projections

Commodity price projections were based on current strip forward prices for the

years 2016-2020. An important element to note is that Peyto sells its natural gas

at a 30% premium to AECO natural gas prices due to its higher heat content OF

gas

Valuation

Operating Model

Exhibit 28

2015-2020 Forecasted Production Profile

Exhibit 29

2015-2020 Forecasted Commodity Prices

Peyto Exploration - Production Profile

Projected Fiscal Years Ending December 31st

2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Days in Year 365 365 365 366 365 365 365 366

Average Daily Production

Gas (MMcf) 361.9 451.0 474.7 561.4 575.6 641.3 744.8 785.0

Oil and NGL's (MBbls) 7.0 8.1 6.5 7.9 9.0 10.1 10.6 11.4

Total Daily MMcfe 403.8 499.5 513.7 608.6 629.6 701.7 808.1 853.4

Total Annual Production

Gas (Bfce) 132.1 164.6 173.3 205.5 210.1 234.1 271.9 287.3

Oil and NGL's (MMBbls) 2.5 2.9 2.4 2.9 3.3 3.7 3.9 4.2

Total Bcfe 147.4 182.3 187.5 222.7 229.8 256.1 295.0 312.3

Reserves

Proved Producing 1,251.9 1,200.0

Total Proved 89.9 2,085.0

Probable Additional 77.9 1,104.0

Total Reserves (Bcfe) 167.8 3,189.0

Total Reserves (MMBOE) 376.5 3,389.0

Reserve Life Ratio (Years) 1.1 17.5

Proved Reserves % Oil 20.7% 32.6%

Peyto Exploration - Resource Price, Hedging and Revenue Profile

Projected Fiscal Years Ending December 31st

($ as Stated) 2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Average AECO Prices

Gas ($ Per Mcf) 3.25 3.50 2.5 2.5 3.0 3.8 3.8 3.8

Oil and NGL's ($ Per Bbl) 70.97 70.68 40.00 40.00 50.00 50.00 50.00 50.00

26. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Revenue Forecast

Overall, the company should see its revenue growing from ~C$783 million in

2014 to C$1.59 billion in 2020. Royalties paid will also increase proportionally

over the next years and grow from ~C$61 million in 2014 to ~C$109 million in

2020.

Expense Projections

Operating and production expense projections were calculated on a per Mcfe

basis and based on 5 year historical averages.

Valuation

Operating Model

Exhibit 30

2015-2020 Revenue Forecast

Exhibit 31

2015-2020 Expense Forecast

Peyto Exploration - Revenue Forecast

Projected Fiscal Years Ending December 31st

($ in Millions ) 2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Oil and Gas Sales 561.6 910.4 641.9 763.7 960.1 1,292.1 1,480.0 1,569.2

Realized gain on hedges (loss) 14.2 (66.6) 68.4 (4.8) 62.4 69.5 80.0 84.8

Royalties (40.5) (61.3) (65.6) (78.0) (80.4) (89.6) (103.2) (109.3)

Total Revenue 535.4 782.5 644.7 681.0 942.0 1,272.0 1,456.8 1,544.6

Revenue Grow th % 40.7% 46.1% (17.6%) 5.6% 38.3% 35.0% 14.5% 6.0%

Peyto Exploration - Expense Projections

Projected Fiscal Years Ending December 31st

($ in Millions or Per Mcfe) 2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Expenses Per MMcfe of Production

Operating 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3

Transportation 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1

G&A 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Market and reserves bonus 0.1 0.1 0.2 0.2 0.2 0.2 0.2 0.2

Accretion of decommissioning 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Depletion and depreciation 1.5 1.6 1.8 1.6 1.6 1.6 1.6 1.6

Royalties 0.3 0.3 0.4 0.4 0.4 0.4 0.4 0.4

Total Expenses Per MMcfe 2.1 2.2 2.5 2.7 2.7 2.7 2.7 2.7

Total Expenses Per Mmcfe excluding depreciation0.6 0.6 0.7 1.1 1.1 1.1 1.1 1.1

Total Production-Linked Expenses ($ in Millions)

Operating 45.2 57.6 54.6 72.0 74.3 82.8 95.3 100.9

Transportation 16.2 21.9 26.2 31.1 32.1 35.7 41.1 43.6

G&A 5.2 5.8 6.0 10.5 10.8 12.1 13.9 14.7

Market and reserves bonus 16.3 19.2 22.4 53.4 55.1 61.4 70.7 74.8

Accretion of decommissioning 1.5 1.9 2.3 2.4 2.5 2.8 3.2 3.4

Depletion and depreciation 225.0 291.7 317.1 356.3 367.6 409.7 471.9 499.7

Royalties 40.5 61.3 65.6 78.0 80.4 89.6 103.2 109.3

Total Production-Linked Exp 309.5 398.1 109.2 166.9 172.2 191.9 221.1 234.1

27. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Income Statement Forecast

Overall, the company should see its net income growing form ~C$262 million in

2014 to ~C$545 million in 2015.

EBITDA Projections

Since certain expenses on the income statement such as depletion and

depreciation are non-cash, EBITDA is a better proxy of how much cash the

company generates. As shown below, the company’s EBITDA should grow from

~C$ 650 million to 1,260 million in 2020.

Valuation

Operating Model

Exhibit 32

2015-2020 Income Statement Forecast

Peyto Exploration - Income Statement

Projected Fiscal Years Ending December 31st

($ in Millions Except Per Share Data) 2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Revenue

Oil and gas sales 561.6 910.4 641.9 763.7 960.1 1,292.1 1,480.0 1,569.2

Realized gain on hedges 14.2 (66.6) 68.4 (4.8) 62.4 69.5 80.0 84.8

Royalties (40.5) (61.3) (65.6) (78.0) (80.4) (89.6) (103.2) (109.3)

Total Revenue 535.4 782.5 644.7 681.0 942.0 1,272.0 1,456.8 1,544.6

Expenses

Operating 45.2 57.6 54.6 72.0 74.3 82.8 95.3 100.9

Transportation 16.2 21.9 26.2 31.1 32.1 35.7 41.1 43.6

G&A 5.2 5.8 6.0 10.5 10.8 12.1 13.9 14.7

Reserves based bonus 16.3 19.2 22.4 53.4 55.1 61.4 70.7 74.8

Performance based compensation 5.6 0.9 9.6 6.8 9.4 12.7 14.6 15.4

Interest 31.0 34.4 32.1 34.0 42.4 50.9 58.3 61.8

Accretion of decommissioning 1.5 1.9 2.3 2.4 2.5 2.8 3.2 3.4

Depletion and depreciation 225.0 291.7 317.1 356.3 367.6 409.7 471.9 499.7

Total Expenses 346.0 433.4 472.3 566.5 594.2 668.0 769.0 814.4

Operating Income 189.4 349.0 173.8 114.4 347.8 603.9 687.8 730.2

Income tax expense (benefit) 46.7 87.3 72.8 11.4 88.0 152.8 174.1 184.8

Net Income 142.6 261.8 101.0 103.0 259.8 451.1 513.7 545.4

Earnings Per Diluted Share 0.96 1.71 0.63 0.64 1.59 2.73 3.08 3.23

Average Diluted Shares 148.7 153.2 160.5 162.2 163.8 165.4 167.1 168.7

Exhibit 33

2015-2020 Income Statement Forecast

Peyto Exploration - Non-Cash and One-Time Expenses and EBITDA

Projected Fiscal Years Ending December 31st

($ in Millions) 2013A 2014A 2015E 2016F 2017F 2018F 2019F 2020F

Operating Income 189.4 349.0 173.8 114.4 347.8 603.9 687.8 730.2

Plus DD&A 225.0 291.7 317.1 356.3 367.6 409.7 471.9 499.7

Plus Asset Retirement Accr. 13.0 8.0 10.0 10.5 10.8 12.1 13.9 14.7

Plus Performance based comp. 5.6 0.9 9.6 6.8 9.4 12.7 14.6 15.4

EBITDA 432.9 649.7 511.1 488.1 735.7 1,038.5 1,188.2 1,260.1

28. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Unlevered Free Cash Flow Projections

Peyto’s projected unlevered free cash flows was based on the aforementioned

production, commodity price and expense projections. The company is expected

to generate ~C$591 million in unlevered free cash flow in 2020.

Terminal Value and Discount Rate

The standard 10% O&G discount rate was applied as well as an 8.0x (current

multiple is 11.7x) 2020 exit multiple was used.

Valuation

DCF

Exhibit 34

2015-2020 Unlevered Free Cash Flow Projections

Peyto Exploration - Unlevered Free Cash Flow Projections

Projected Fiscal Year Ending December 31st

2015E 2016F 2017F 2018F 2019F 2020F

Normal Discount Period 1.0 2.0 3.0 4.0 5.0 6.0

Mid-Year Discount 0.25 1.25 2.25 3.25 4.25 5.25

Annual Production 187.5 222.7 229.8 256.1 295.0 312.3

Revenue 644.7 681.0 942.0 1,272.0 1,456.8 1,544.6

EBITDA 485.9 488.1 735.7 1,038.5 1,188.2 1,260.1

Operating Income (EBIT) 149.2 114.4 347.8 603.9 687.8 730.2

( – ) Taxes (37.8) (11.4) (88.0) (152.8) (174.1) (184.8)

EBIAT 111.4 103.0 259.8 451.1 513.7 545.4

( + ) DD&A 317.1 356.3 367.6 409.7 471.9 499.7

( + ) Asset Retirement Accretion 0.5 2.3 2.4 2.5 2.8 3.2

( + ) Future performance based compensation 9.6 6.8 9.4 12.7 14.6 15.4

( + ) Deffered Income Tax 70.4 11.4 88.0 152.8 174.1 184.8

( – ) Change in Netw orking Capital (19.3) (20.4) (28.3) (38.2) (43.7) (46.3)

( – ) Capital Expenditures (600.0) (615.0) (650.0) (690.0) (710.0) (715.0)

Unlevered Free Cash Flow (71.6) (114.7) 105.6 377.0 510.8 579.9

Present Value of Free Cash Flow (69.9) (101.8) 85.2 276.6 340.7 351.6

29. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Implied Share Price Calculation

With a 8.0 terminal EBITDA multiple and by using a 10% discount rate, Peyto’s

implied equity value amounts to ~C$5.7 billion, implying a C$34.8 share price

and 22.4% upside.

Valuation

DCF

Exhibit 36

Terminal EBITDA Multiples and Discount Rate Sensitivity Analysis

Exhibit 35

DCF Share Price Calculation

DCF Implied Share Price

Present Value of Terminal Value 5,690.4

Sum of PV of Free Cash Flows 882.36

Enterprise Value 6,572.7

( – ) Net Debt 1,047.0

Implied Equity Value 5,525.7

Diluted Shares Outstanding 159.0

Implied Share Price 34.8

% premium / (discount) over market share price 22.4%

Peyto Exploration - Net Present Value Sensitivity - Terminal EBITDA Multiples

34.76$ 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0%

10.0 x 52.6 49.4 46.5 43.7 41.1 38.7 36.4

9.0 x 47.3 44.4 41.8 39.2 36.9 34.6 32.6

8.0 x 42.0 39.4 37.0 34.8 32.6 30.6 28.7

7.0 x 36.7 34.4 32.3 30.3 28.4 26.6 24.9

6.0 x 31.4 29.4 27.6 25.8 24.2 22.6 21.1

5.0 x 26.2 24.5 22.8 21.3 19.9 18.6 17.3

Discount Rate

TerminalEBITDAX

Multiples

30. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Assumptions

Decline rates of 35% was used for the company’s natural gas and liquids

production and the aforementioned production forecast was used as well as the

companies reserve information. Operating expenses were forecasted for the first

five years and maintained constant thereafter. Also, development expenses of C

$1.2 billion over 10 years was subtract from each years' cash flow calculations

and cash taxes of 1of 15% was also applied.

NAV Build-up

In order to calculate the company’s NAV, its proven and drilled risked

undeveloped reserves was added . In terms of risked drilled undrilled reserves,

the four main regions was the Notikewin, Wilrich, Falher and Bluesky region was

accounted for and their respective Net Asset Value was risked by 75% in order to

find the value of undeveloped reserves.

By applying a 10% discount rate, the discounted cash flows from the company’s

proven reserves amounted to ~C$3.9 billion and the undeveloped reserves

amounted to ~C$2.7 billion. The Enterprise Value amounted to ~C$ 6.5, implying

a share price of C$35.1 and 23.5% upside.

Valuation

NAV

Exhibit 37

Peyto Exploration Risked Valuation

Unrisked $/Share Probality Risked $/Share

Notikwen 405 2.5 75% 304 1.9

Wilrich 1,239 7.8 75% 929 5.8

Falher 1,493 9.4 75% 1,120 7.0

Bluesky 426 2.7 75% 320 2.0

Total 3,563 22.4 2,672 16.8

Undeveloped Reserves

Exhibit 38

NAV Implied Share Price Calculation

NAV Buildup

Price Assumptions 2015 Gas Price LT Nat Gas price LT Oil Price

3.2$ 4.50$ 50.00$

Probability Risked Value ($M) $/Share

PDPReserves Cash Flow Undiscounted 6,199 39.0

PV-10 PDPCash Flow 100% 3,767 23.7

Land Value 100% 97 0.6

Total Proved Reserves 3,864 24.3

Undeveloped Reserves 2,672 16.8

Net Asset Value (Enterprise Value) 6,536 41.1

Net Debt 960 6.0

Implied Equity Value 5,576 35.1

Diluted Shares Outstanding 159.0

Value/ Share 35.1

%premium / (discount) over market share price 23.5%

31. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Valuation Summary

The weighted average of the DFC and NAV valuation was used in order to

determine target share price. Based on the implied shared price of C$34.8 for

the DCF and C$35.1 for the NAV, the implied one year target price of C$34.95

Valuation

NAV

Exhibit 39

Natural Gas Prices and Discount Rate

Peyto Exploration - Net Present Value Sensitivity - Natural Gas Prices

35.08$ 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0%

5.75 41.5 40.1 38.7 37.5 36.4 35.3 34.3

5.00 39.7 38.4 37.2 36.1 35.0 34.0 33.1

4.25 38.0 36.8 35.6 34.6 33.6 32.7 31.8

3.50 36.2 35.1 34.1 33.1 32.2 31.4 30.6

2.75 34.4 33.4 32.5 31.7 30.8 30.1 29.4

2.00 32.7 31.8 31.0 30.2 29.5 28.8 28.2

NaturalGasPrices

($/Mcfe)

Discount Rate

Exhibit 40

Natural Gas Prices and Discount Rate

Peyto Exploration - Valuation Upside

0.23$ 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0%

5.75 46% 41% 36% 32% 28% 24% 21%

5.00 40% 35% 31% 27% 23% 20% 16%

4.25 34% 29% 25% 22% 18% 15% 12%

3.50 27% 24% 20% 17% 13% 10% 8%

2.75 21% 18% 14% 11% 9% 6% 3%

2.00 15% 12% 9% 6% 4% 1% -1%

OilPrices

Discount Rate

32. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Reliance on Natural Gas

Peyto's production is predominately skewed toward natural gas. As such, the

company's cash flow and profitability are highly exposed to the price of natural

gas. While the company is doing a good job of protecting cash flows with its

hedging strategy, continued low gas prices will limit Peyto's upside potential.

Need to reduce CO2 emissions

The newly elected government in Alberta is eliciting strong opinions in terms of

tax and emissions policies. While tax discussions are still under way, Peyto said

the new regime has tasked it to reduce CO2 emissions per unit of gas

processed. As an example, Peyto's Oldman gas processing plant needs to

reduce emissions by 15% by 2015 and 20% by 2017 or else it will be paying

penalties of $20 and $30 a ton for 2016 and 2017 and thereafter. However, Peyto

says it sees an "extremely strong alignment" between CO2 emissions and

business costs performance. For example: at the Oldman plant, Peyto expects to

reduce fuel gas consumption by over 20% by way of process modifications that

are currently maintained so that the facility falls back to or below the 100,000 ton

emissions level. The result is that Peyto is going to save about $1 million in fuel

gas cost per year. So not only is Peyto producing a fuel that is cleaner and

cheaper than either coal or oil sands crude, it is able to reduce fuel costs in order

to meet the tougher emission standards coming down the road. As a matter of

fact, increased awareness of CO2 emissions will likely lead to a reduction in coal

consumption and an increase in demand for the natural gas Peyto produces.

Natural gas burned for electrical power generation releases 30% less CO2 than

does coal, and 100% less of the toxic particulate emissions that coal leaves

behind.

Third-Party Pipeline Constraints – TransCanada

Like most gas operators in the region, Peyto's Production for the quarter (81,208

boe/d) was negatively impacted by capacity constraints on the TransCanada

Nova Gas Transmission Network (NGTL). The NGTL system has been

undergoing maintenance and expansion work throughout the year. Peyto

reported that service interruptions and curtailments on the NGTL system

deferred an average of 65 MMcfe/d (10,750 boe/d) in Q3. This is significant, as

the deferred production was some 13% of Q3's reported total production. After

the end of the quarter, Peyto said production had reached ~104,000 boe/d.

NGTL is forecasting that the capability of their system should not only return to

previous levels, but increase to over 9 BCF/d by November 2015 when all of

these issues have been resolved and work completed. With only a few producers

drilling and adding new production in this part of the province (PEY, TOU,

Progress, etc.) it is unlikely that total throughput will be back to where it was last

winter at just over 8 BCF/d. This means there should be ample room for all

volumes plus some additional growth, assuming there isn’t a large amount of

contracted but unused capacity. Recently, TransCanada announced an

additional $570 million expansion to the NGTL system, supported by 2.7 Bcfe/d

of new firm natural gas transportation service contracts. Commenting on the new

contracts, Russ Girdling, TRP's President & CEO, said: "Our NGTL System is

sitting on top of extensive natural gas supplies, making it well-positioned to

unlock the resource and reliably and efficiently link it to growing markets.

Risks

33. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

The system has been operating at capacity, and more capacity is needed in

these key areas that support the growth of the prolific gas resource in the

Western Sedimentary Basin." And, of course, Peyto is lowest-cost gas producer

in the prolific Deep Basin and one of the largest producers in the region. As a

result, there is a good chance Peyto was one of the companies signing new

transportation service contracts with TransCanada for additional NGTL pipeline

capacity.

While service restrictions continued into October, Peyto was able to secure

temporary service for the last 11 days of the month for all previously restricted

production. As a result, Peyto said it increased production from the start of

October (83,500 boe/d) to an estimated average of 102,000 boe/d by the end of

the month. TRP is currently forecasting additional constraints for the first 3

weeks of November prior to increasing system capacity which should alleviate

restrictions in Peyto's production toward the end of the year and into 2016.

Risks

34. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Appendix

Comparable Companies Analysis

Exhibit 41

Comparable Company Production Metrics

Capitalization EBITDAX Proved Reserves Daily Production Proved Developed Gas

Company Name Mkt. Cap ($M) EV ($M) 2015 2016 (Bcfe) (Mcfe) / Proved Mix %

Antero Resources 6,632 10,535 1,239 2,667 10,535 1,494 31.2% 81.0%

Cabot Oil and Gas 8,123 10,230 897 790 7,082 1,644 61.3% 94.0%

Chesapeake 2,712 15,123 2,479 2,853 10,692 3,600 80.6% 72.0%

EQT 8,903 10,536 1,484 2,509 9,776 1,662 43.5% 91.0%

Memorial Resources 3,063 5,726 418 93 1,740 348 44.4% 77.0%

Rice Energy 1,369 2,726 440 779 1,307 534 49.3% 99%

Soutw estern 3,456 8,239 1,681 1,873 9,809 2,682 57.9% 92%

Tourmaline 5,890 8,613 1,002 1,595 2,417 930 43.0% 87%

Maximum 8,903 15,123 2,479 2,853 10,692 3,600 80.6% 99.0%

75th Percentile 7,005 10,535 1,533 2,548 9,991 1,917 58.7% 92.5%

Median 4,673 9,422 1,120 1,734 8,429 1,569 46.9% 89.0%

25th Percentile 2,975 7,611 783 787 2,248 831 43.4% 80.0%

Minimum 1,369 2,726 418 93 1,307 348 31.2% 72.0%

Peyto Exploration 4,516 5,995 486 488 3,189 514 0.0% 90%

Exhibit 42

Comparable Company Trading Multiples

Capitalization EV/ EBITDA EV/ EV/ D/CF

Company Name Mkt. Cap ($M) EV ($M) 31/12/2015 31/12/2016 Proved Reserves Daily Production 2016E

Antero Resources 6,632 10,535 8.5 x 7.9 x 1.0x 7.1x 3.7

Cabot Oil and Gas 8,123 10,230 11.4 x 25.9 x 1.4x 6.2x 9.4

Chesapeake 2,712 15,123 6.1 x 10.6 x 1.4x 4.2x 11.1

EQT 8,903 10,536 7.1 x 8.4 x 1.1x 6.3x 1.5

Memorial Resources 3,063 5,726 13.7 x 122.7 x 3.3x 16.5x 7.5

Rice Energy 1,369 2,726 6.2 x 7.0 x 2.1x 5.1x 4.1

Soutw estern 3,456 8,239 4.9 8.8 0.8x 3.1x 8.7

Tourmaline 5,890 8,613 8.6 10.8 3.6x 9.3x 13.2

Maximum 8,903 15,123 13.7 x 122.7 x 3.6x 16.5x 13.2

75th Percentile 7,005 10,535 9.3 x 14.6 x 2.4x 7.6x 9.8

Median 4,673 9,422 7.8 x 9.7 x 1.4x 6.3x 8.1

25th Percentile 2,975 7,611 6.2 x 8.3 x 1.1x 4.9x 4.0

Minimum 1,369 2,726 4.9 x 7.0 x 0.8x 3.1x 1.5

Peyto Exploration 4,516 5,995 12.3 x 12.3 x 1.9x 11.7x 2.5

35. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Appendix

Management

Management and Ownership

Institutions hold approximately 40% of the outstanding shares of PEY while

insiders represent 5.4% of the total shares.

Management:

• Darren Gee, Director, President and CEO: Mr. Gee has over 23 years of

experience working in the oil and gas industry. Mr. Gee joined Peyto in 2001

as the VP Engineering before entering his current position as President and

CEO.

• Scott Robinson, Director, Executive VP and COO: Mr. Robinson brings

with him over 30 years of experience in the oil and gas industry, he has been

with Peyto since 2004 when he first joined as VP Operations. In 2006 Mr.

Robinson became Executive Vice President and COO at Peyto.

• Kathy Turgeon, VP Finance and CFO: Ms. Turgeon joined Peyto as the

Controller in 2004. Since then Ms. Turgeon held the role of VP Finance before

becoming the VP Finance and CFO in 2007.

• Timothy Louie, VP Land: Mr. Louie has over 25 years of experience in the oil

and gas industry. Prior to joining Peyto, Mr. Louie was a Land Manager at

Daylight Energy Ltd.

• David Thomas, VP Exploration: Mr. Thomas brings 21 years of experience

in the oil and gas industry. Mr. Thomas first joined Peyto as a Senior Geologist

before entering his current position as VP Exploration

• Jean-Paul Lachance, VP Exploitation: Mr. Lachance has over 21 years of

experience working in the oil and gas industry. Previously, Mr. Lachance was

VP Engineering at ProspEx Resources, a company that explores, develops

and produces oil and natural gas in western Canada.

• Stephen Chetner, Director, Corporate Secretary: Mr. Chetner has been the

Corporate Secretary at Peyto since 2000. Mr. Chetner is a partner at Burnet,

Duckworth & Palmer LLP, a legal services firm.

Directors

• Donald Gray, Chairman: Mr. Gray co-founded Peyto in 1998 and held the

position of CEO for 8 years. Currently, Mr. Gray is Chairman of the Board a

Peyto

• Rick Braund, Director: Mr. Braund is a co-founder of Peyto and has been

Director since 1998. Mr. Braund is a Director at Gear Energy Corporation and

Petrus Resources Ltd, private oil and gas companies

• Brian Davis, Director: Mr. Davis brings with him over 17 years of oil and gas

industry experience. Mr. Davis has been a director at Peyto since 2006 and is

currently a Managing Partner at an oil and gas engineering consultancy firm.

• Michael MacBean, Director: Mr. MacBean has been a director at Peyto since

2003 and brings over 13 years of experience in the oil and gas industry. Mr.

MacBean is currently a Managing Director of TriWest Capital Partners and

previously held the position of CEO at Diamond Energy Services LP.

• Gregory Fletcher, Director: Mr. Fletcher brings with him over 14 years of

experience working in the oil and gas industry. Mr. Fletcher has been a

Director at Peyto since 2007 and is currently the President of Sierra Energy

Inc, a private oil and gas company.

36. KENNETH WOODS

PORTFOLIO MANAGEMENT PROGRAM

Sources

1. Company Reports

2. GeoScout

3. Canada International Energy Agency

4. Altacorp Equity Research – Q3 2015

5. BMO Equity Research – Q2 2015

6. CIBC Equity Research – Q2 2015

7. Haywood Equity Research – Q1 2015

8. Barclays Equity Research – Q1 2015

9. RBC Equity Research – Q1 2015

10. GMP Equity Research – Q4 2014

11. UBS Equity Research – 2014 Initiating Coverage