Download to read offline

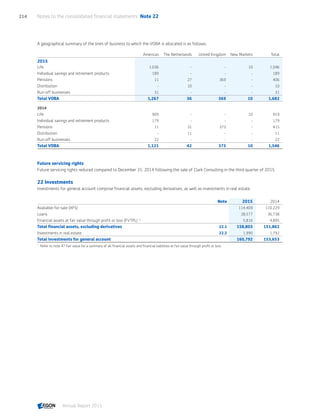

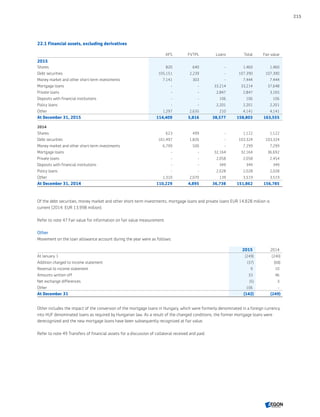

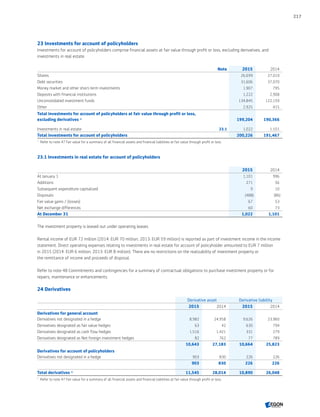

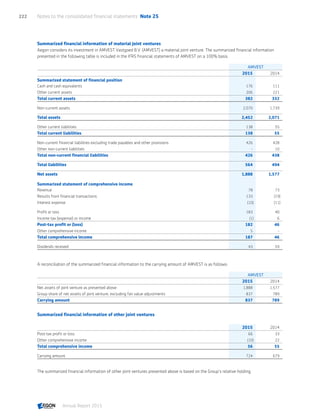

The 2015 annual report for Aegon outlines the company's operational and financial progress, highlighting a 24% increase in sales compared to the previous year while noting challenges in earnings, particularly in the US due to low interest rates and changes in customer behavior. Aegon's strategy focuses on enhancing customer connections and digital solutions, along with a commitment to reducing expenses by EUR 200 million over the next three years. The report also emphasizes the company's strong capital position, with plans for capital return and a growing dividend policy amidst a complex regulatory landscape.