Learning Objective

4.1.1 Distinguishbetween management’s and auditor’s

responsibility

4.1.2 Explain the auditor’s responsibility for discovering

material misstatements due to fraud or error.

4.1.3 Discuss the three categories of management assertions

about financial information

4.1.4 Describe the need to maintain professional skepticism

when conducting an audit.

4.1.5 Identify the benefits of a cycle approach to segmenting

the audit.

4.1.6 Describe how audit objectives (transaction related

balance related) relate to management assertions

4.1.6 Explain the relationship between audit objectives and

the accumulation of audit evidence.

3.

Audit Responsibility &Objective

The objective of an audit of the financial statements- is an expression

of an opinion on the fairness of the financial statements in all

material respects.

• How auditor’s achieve this objective?

• Auditors accumulate evidence in order to reach conclusions

about whether the financial statements are fairly stated and to

determine the effectiveness of internal control, after which they

issue the appropriate audit report.

• If the auditor believes that the statements are not fairly

presented or is unable to reach a conclusion because of

insufficient evidence, the auditor has the responsibility of

notifying users through the auditor’s report.

Subsequent to their issuance, if facts indicate that the

statements were not fairly presented, the auditor will probably

have to demonstrate/experess to the courts or regulatory agencies

that the audit was conducted in a proper manner and the

auditor reached reasonable conclusions.

.

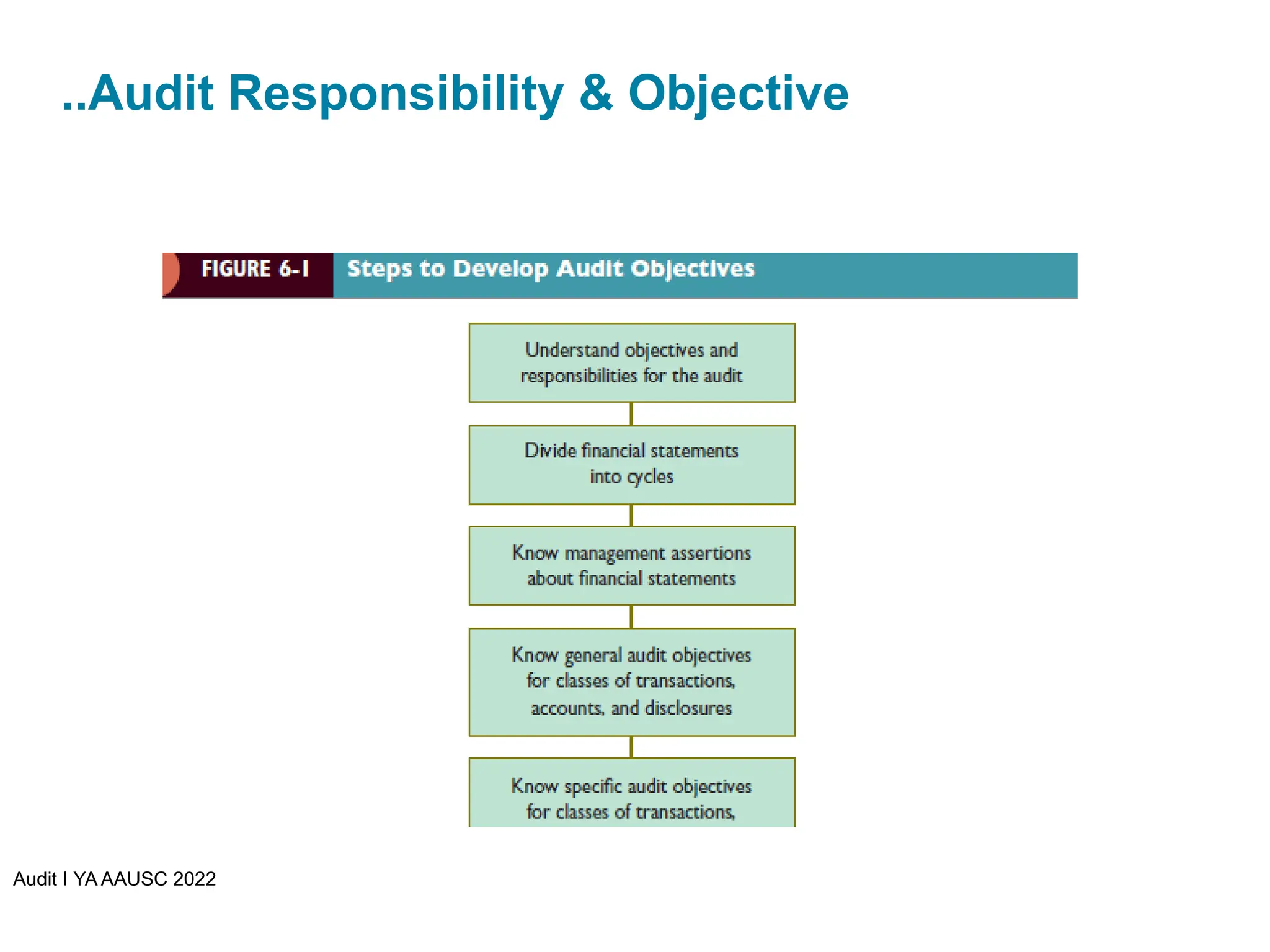

Steps to developan audit Objective

Step 1: Understand objectives and responsibilities for

the audit

Management’s Responsibilities: Management of a

company is responsible for

Designing and implementing internal control systems

effectively,

Adopting sound accounting policies, and

Making fair representations in the financial statements

(preparing financial statements of the entity genuinely)

-A company’s management knows more about the company’s

transactions and related assets, liabilities, and equity more

than the auditor since they operate the business daily

•

-The auditor’s knowledge of these matters and internal control

is limited to that acquired during the audit.

- The management responsibility report is usually attached in

the annual reports of public companies

6.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for

the audit

Auditor’s Responsibilities:

– As per ISA 200 the independent auditor is responsible:

(a)To obtain reasonable assurance -about whether the

financial statements as a whole are free from

material misstatement ( whether due to fraud or

error), thereby enabling the auditor to express an

opinion on whether the financial statements are

prepared, in all material respects, in accordance with an

applicable financial reporting framework; and

(b) To report on the financial statements, and

communicate as required by the ISAs, in accordance

with the auditor's findings

7.

…Steps to developan audit Objective

…Step 1: Understand objectives and responsibilities for the

audit

….Auditor’s Responsibilities:

•

Major points emphasized in the auditors responsibilities are:

Detecting material misstatements in the financial

statement

Identifying material weaknesses in internal control

over financial reporting.

Providing reasonable assurance on the fairness of

financial statements and about control systems ( For

larger public companies, the auditor also issues a report

on internal control over financial reporting as required

by Section 404 of the Sarbanes–Oxley Act.)

8.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for

the audit

•

Material Versus Immaterial Misstatements

– Misstatements are usually considered material –

-if the combined uncorrected errors and fraud

in the FSs would likely have changed or influenced

the decisions of a reasonable person using the

statements.

– Although it is difficult to quantify a measure of

materiality, auditors are responsible for obtaining

reasonable assurance that this materiality

threshold has been satisfied.

– It would be extremely costly (and probably

impossible) for auditors to have responsibility for

finding all immaterial errors and fraud.

9.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

•

Reasonable Assurance

– Assurance - is a measure of the level of certainty

that the auditor has obtained at the completion of

the audit.

Auditing standards indicate reasonable assurance-

is a high level of assurance, but not absolute level

of assurance that indicates financial statements are

free of material misstatements.

The concept of reasonable, but not absolute,

assurance indicates that the auditor is not an

insurer or guarantor of the correctness of the FSs.

– Thus, an audit that is conducted in accordance with

auditing standards may fail to detect a material

misstatement.

10.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

….Auditor’s Responsibilities:

•

Why the auditor is responsible for reasonable but

not absolute assurance?

1. Audits are usually conducted on test basis

(sampling)

Sampling inevitably includes some risk

of not detecting a material

misstatement.

Auditors may also make mistake in

making judgments about the area to be

tested, the type, extent, and timing of

the tests and also evaluation of the

evidences.

11.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

2. In accounting complex estimates are used, which

inherently involve uncertainty and can be affected by

future events.

Because of the uncertainties involved in the estimates,

an audit can not give absolute assurance

3. Fraudulently prepared financial statements are

often extremely difficult, if not impossible, for the

auditor to detect, especially when there is collusion

among management.

.

12.

Audit I YAAAUSC 2022

To conclude:

It is evident that looking at each and every

document is costly and will not be

economical;

So the auditor’s best defense, when material

misstatements are not uncovered- is to have

conducted the audit in accordance with

auditing standards

13.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the

audit

Errors Versus Fraud

- Auditing standards distinguish between two types of

misstatements:

a. errors and

b. fraud.

-Either type of misstatement can be material or

immaterial.

-An error is an unintentional misstatement of the

financial statements,

-whereas fraud is intentional .

14.

Audit I YAAAUSC 2022

Fraud has been classified in to two:

1.Misappropriation(taking) of assets,- often called

defalca`tion ( employee fraud)

- eg. a clerk taking cash at the time a sale is made and

not entering the sale in the cash register

2. Fraudulent financial reporting,- often called

management fraud.

-eg. intentional overstatement of sales near the

balance sheet date to increase reported earnings.

15.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

. Auditor’s Responsibilities for Detecting Material

Errors

•

-Auditors spend a great portion of their time in

planning and performing audits to detect errors in

financial statements.

-Auditors find a variety of errors resulting from such

things as :

mistakes in calculations,

omissions,

misunderstanding and misapplication of

accounting standards, and

incorrect summarizations and descriptions.

16.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

Auditor’s Responsibilities for Detecting Material Frauds

Auditing standards make no distinction between

the auditor’s responsibilities for searching for

errors and fraud.

In either case, the auditor must obtain

reasonable assurance about whether the

statements are free of material misstatements.

The standards also recognize that fraud is often

more difficult to detect because management

or the employees perpetrating/commit the

fraud attempt to conceal the fraud.

17.

Audit I YAAAUSC 2022

Still, the difficulty of detection does not

change the auditor’s responsibility to

properly plan and perform the audit to

detect material misstatements, whether

caused by error or fraud, so proper planning

is essential

18.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

Fraud Resulting from Fraudulent Financial

Reporting

Versus

Misappropriation of Assets

Both fraudulent financial reporting and

misappropriation of assets are potentially

harmful to FS users, but there is an important

difference between them.

Fraudulent financial reporting -harms users by

providing them incorrect FS information for

their decision making.

When assets are misappropriated, -

stockholders, creditors, and others are harmed

because assets are no longer available to their

19.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

….Auditor’s Responsibilities:

•

Auditor’s responsibility to Consider non-compliance of

Laws and regulations/ illegal acts (ISA 250)- :

– In obtaining reasonable assurance -that the

financial statements are free of material

misstatement, the auditor takes into account

applicable legal and regulatory frameworks

relevant to the -client.

-For example, when auditing the FSs of a

bank, the auditor would need to consider

requirements of banking regulators such

as reserve requirement and others.

20.

The auditor’sresponsibilities regarding

noncompliance with laws and regulations

(called-illegal acts) depend on whether the

laws or regulations are expected to have a

direct effect on the amounts and

disclosures in the financial statements.

illegal acts: are violations of laws or

government regulations other than fraud.

-Examples of illegal acts include:

-violation of tax laws

-violation of the environmental

protection laws.

Audit I YA AAUSC 2022

21.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

Direct-Effect of Illegal Acts:

Certain violations of laws and regulations have

a direct financial effect on specific account

balances in the FS.

Eg. a violation of tax laws directly affects income

tax expense and income taxes payable.

The auditor’s responsibility for direct-effect

illegal acts is the same as for errors and

fraud.

On each audit, the auditor should evaluate

whether or not there is evidence indicating

material violations of tax laws.

22.

Audit I YAAAUSC 2022

Discussions with client personnel and

examining reports issued by auditors from

Internal Revenue Service (after the completion

of an examination of the client’s tax return) are

helpful for the auditor to see if there is material

violation of tax laws

23.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

•

Indirect-Effect illegal Acts:

•

-These are illegal acts that affect the financial

statements only indirectly.

EX. if a company violates environmental protection

laws, financial statements are affected only if there is a

fine or sanction.

- Potential material fines and sanctions indirectly

affect FSs by creating the need to disclose a contingent

liability for the potential amount that might ultimately be

paid.

- This is called an indirect-effect illegal act.

- Civil rights laws and employee safety requirements can

24.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

… Auditor’s responsibility to Consider Laws and regulations

ISA 250 - state that the auditor provides no

assurance that indirect-effect illegal acts will

be detected, due to the following reasons:

1. Auditors lack legal expertise,

2. The frequent indirect relationship

between illegal acts and the financial

statements

•

So it is it impractical for auditors to assume

responsibility for discovering indirect-effect

illegal acts.

25.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

•

- When the auditor believes that an illegal act may have

occurred,

•

-several actions are necessary to determine whether

the suspected illegal act actually exists:

1. The auditor should first inquire of management

at a level above those likely to be involved in the

potential illegal act.

2. The auditor should consult with the client’s legal

counsel or other specialist who is knowledgeable

about the potential illegal act.

3. The auditor should consider accumulating

additional evidence to determine whether there actually

26.

…Steps to developan audit Objective

..Step 1: Understand objectives and responsibilities for the audit

Actions When the Auditor Knows of an illegal Act

1. The first action is to consider the effects on

the FSs, including the adequacy of

disclosures. Effects may be complex and

difficult to resolve

eg. effect of violation of civil rights laws could be

significant fines, loss of customers or key

employees, which could materially affect future

revenues and expenses.

or

-If the auditor concludes that the disclosures relative

to an illegal act are inadequate, the auditor should

modify the audit report accordingly.

27.

Audit I YAAAUSC 2022

In deciding whether to modify/not to modify the

report, the auditor should analyze the implication of

the illegal act on important issues like –

- the audit firm’s relationship with management, i.e

- if management knew of the illegal act and failed to

inform the auditor, it is questionable whether

management can be believed in other discussions.

28.

…Steps to developan audit Objective

2. The auditor should communicate (oral or written) with the

audit committee or others of equivalent authority to make

sure that they know of the illegal act.

- If it is oral, the nature of the communication and discussion

should be documented in the audit files.

-If the client either refuses to accept the auditor’s modified report

or fails to take appropriate remedial action concerning the illegal

act, the auditor may find it necessary to withdraw from the

engagement.

- If the client is publicly held, the auditor must also report the

matter directly to the SEC.

- Such decisions are complex and normally involve consultation by

the auditor with the auditor’s legal counsel

29.

…Steps to developan audit Objective

…..Auditor’s Responsibilities:

Professional skepticism

Auditor’s responsibility includes performing an audit with an

attitude of professional skepticism

Assignment 2-on professional judgment and skepticism

–Submission date: end of discussion on Ch 4

1. Explain the concept of professional skepticism and identify its

two elements

2. Describe the key elements of an effective professional judgment

process.

3. List and describe the six elements of professional skepticism?

4. What are the five elements of an effective professional judgment

process?

5. Describe two of the more common judgment traps and biases.

30.

…Steps to developan audit Objective

•

Step 2: Divide Financial Statements in to Cycles

Audits - are performed by dividing the financial statements

into smaller segments or components.

– The division is needed:

To make the audit more manageable and

To facilitate the assignment of tasks to different

members of the audit team.

Eg: The audit of fixed assets and notes payable

– These two items may be audited in different segment

separately but not on a completely independent basis.

-(eg. the audit of fixed assets may reveal an unrecorded note

payable.)

– After the audit of each segment is completed, the results are

combined.

A conclusion can then be reached about the financial

statements taken as a whole.

31.

…Steps to developan audit Objective

•

…Step 2: Divide Financial Statements in to Cycles

•

There are different ways of segmenting an audit.

1. To treat every account balance on the statements

as a separate segment.

Segmenting in this way is usually inefficient.

It would result in the independent audit of such

closely related accounts -as inventory and cost

of goods sold.

2. To use Cycle Approach to Segment an Audit

It is a common way to divide an audit

It involves keeping closely related types (or

classes) of transactions and account balances

in the same segment

32.

…Steps to developan audit Objective

•

…Step 2: Divide Financial Statements in to Cycles

The cycle approach combines transactions recorded in

different journals with the general ledger balances that

result from those transactions

The cycle approach divides financial statement items in

to five cycles

•

1. Sales and collection cycle (S)

•

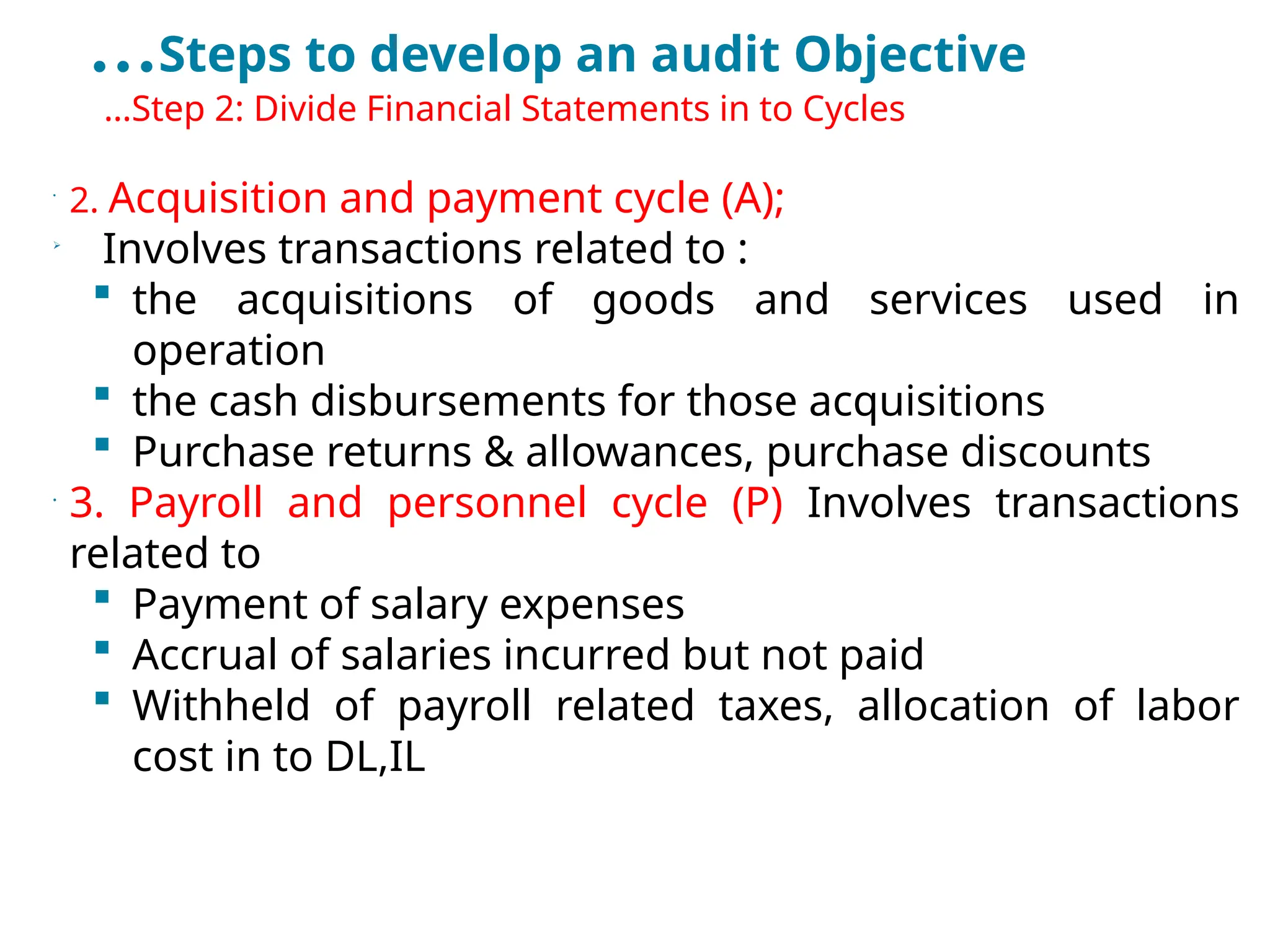

2. Acquisition and payment cycle (A)

•

3. Payroll and personnel cycle (P)

•

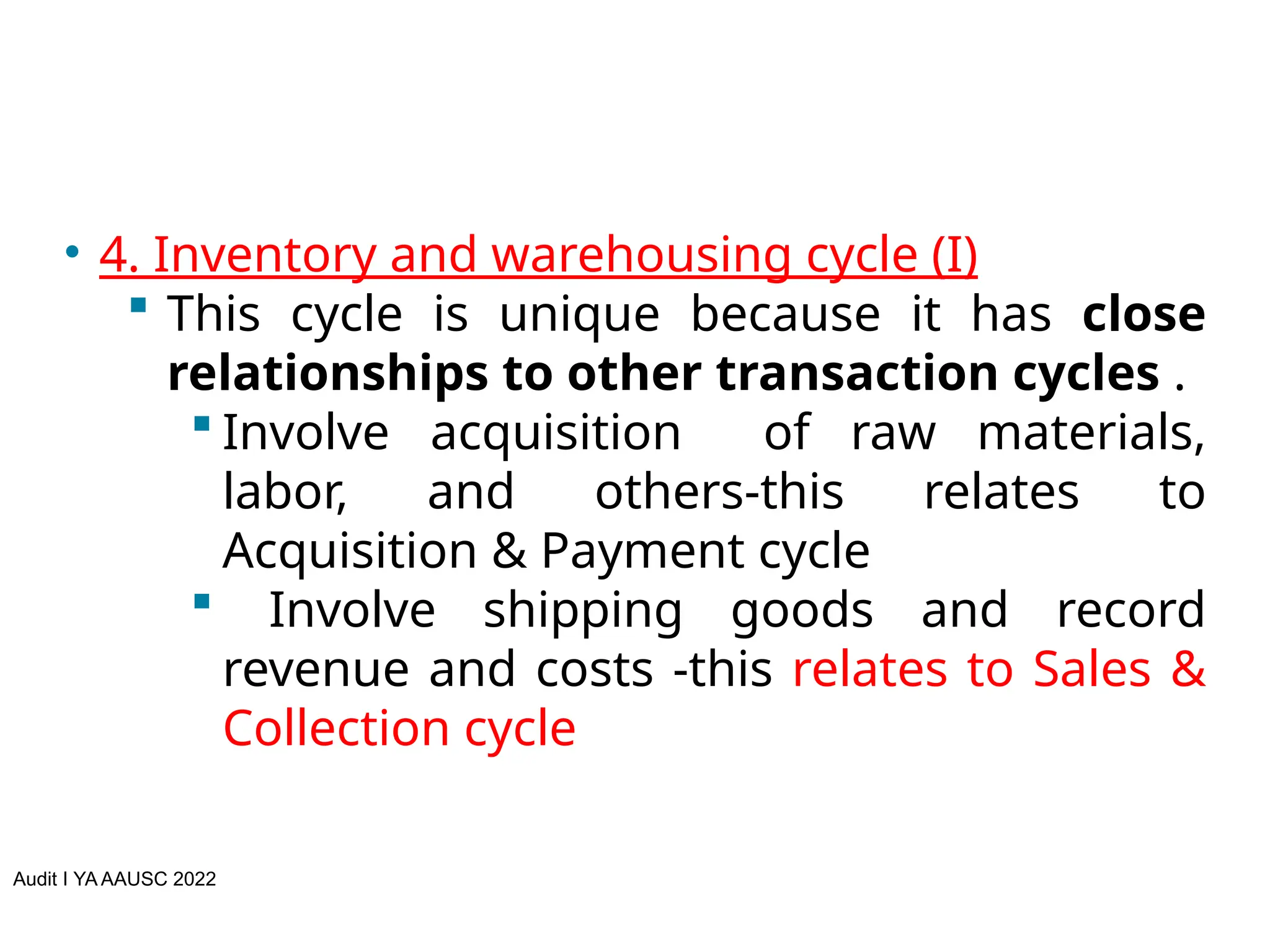

4. Inventory and warehousing cycle (I)

•

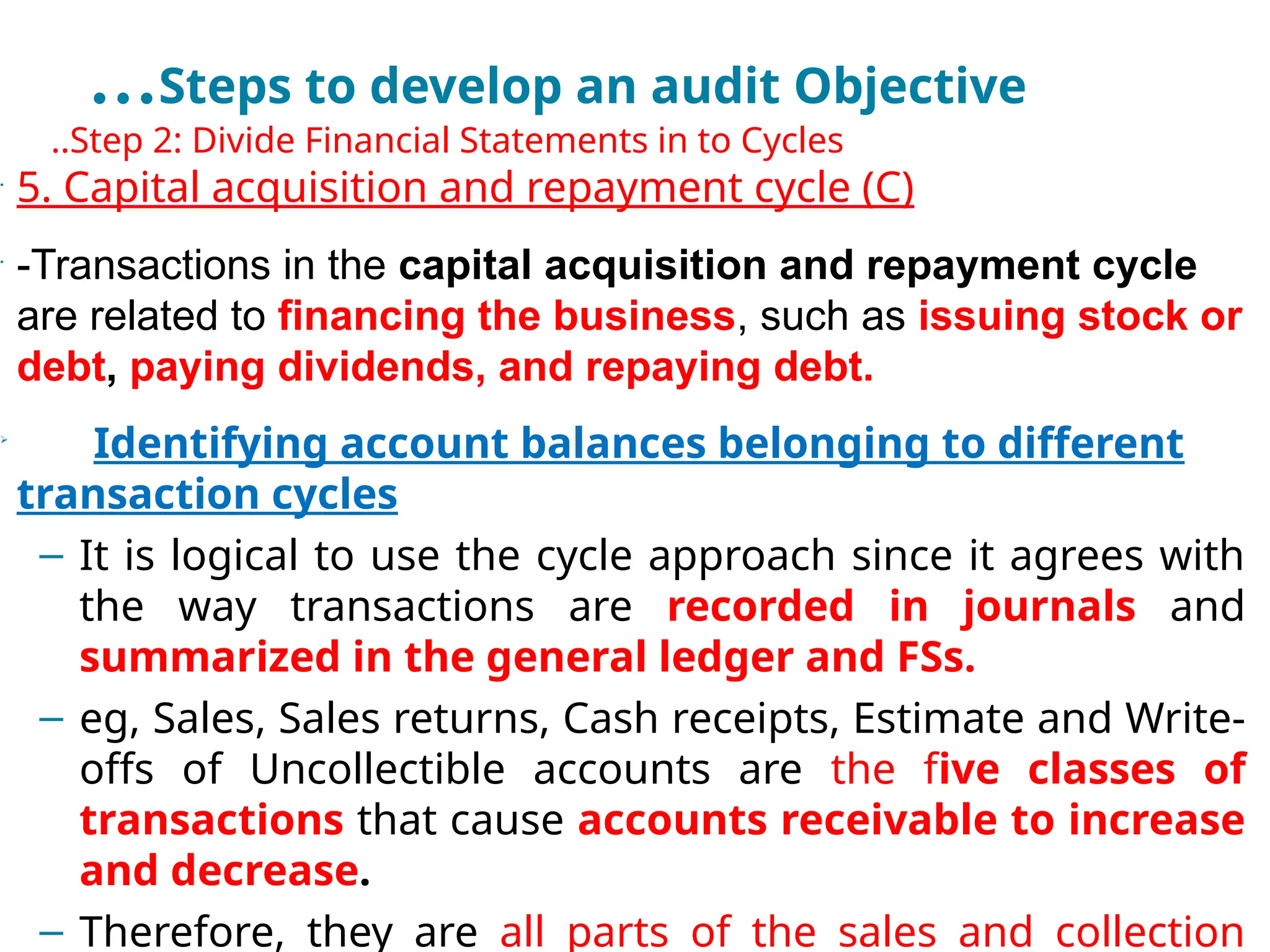

5. Capital acquisition and repayment cycle (C)

•

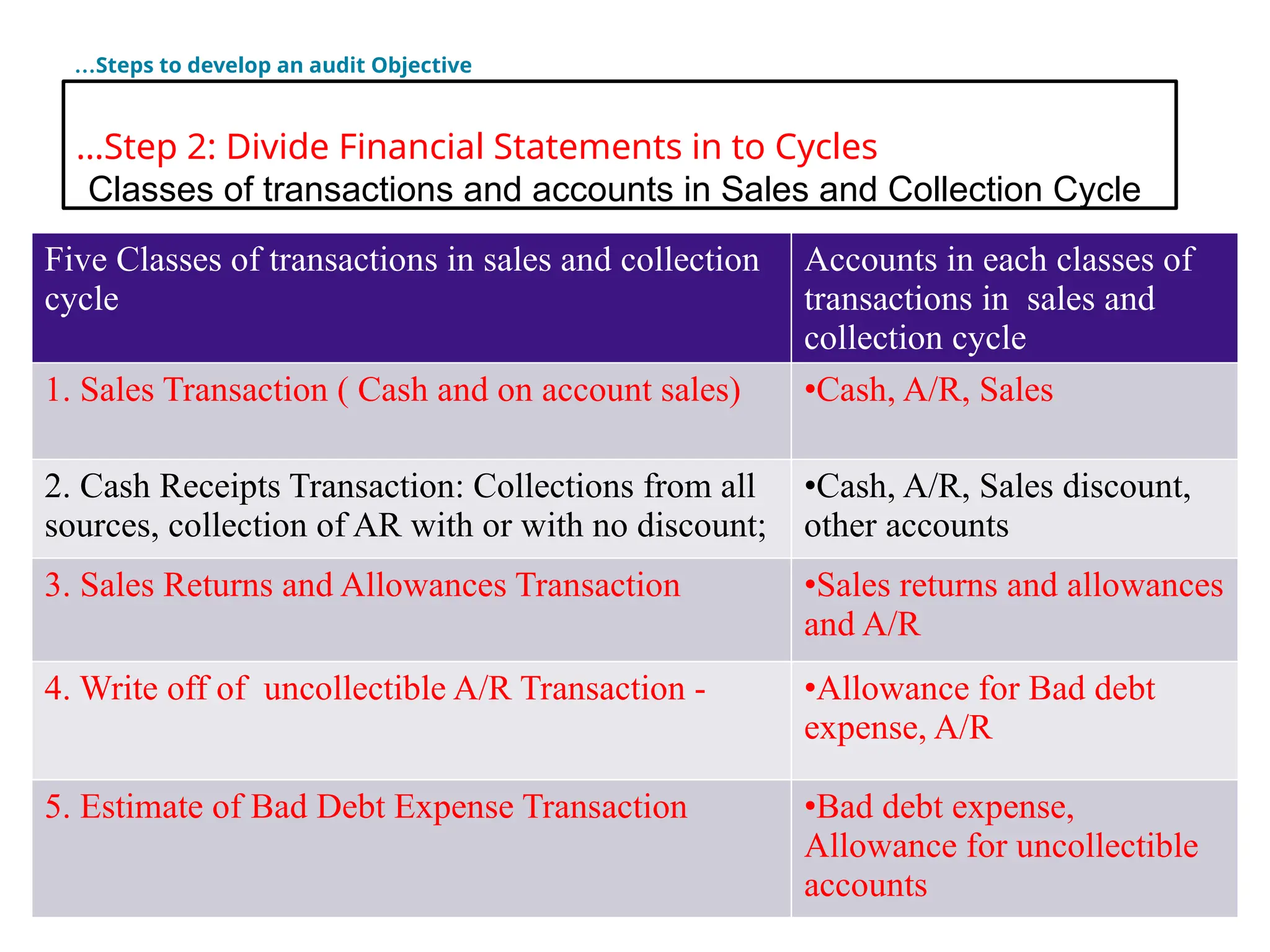

1. Sales and collection cycle (S)

-The sales and collection cycle is the first cycle listed and is a

primary focus on most audits.

- Collections on trade accounts receivable in the cash receipts

journal is the primary operating inflow to cash in the bank.

33.

33

…Steps to developan audit Objective

Five Classes of transactions in sales and collection

cycle

Accounts in each classes of

transactions in sales and

collection cycle

1. Sales Transaction ( Cash and on account sales) •Cash, A/R, Sales

2. Cash Receipts Transaction: Collections from all

sources, collection of AR with or with no discount;

•Cash, A/R, Sales discount,

other accounts

3. Sales Returns and Allowances Transaction •Sales returns and allowances

and A/R

4. Write off of uncollectible A/R Transaction - •Allowance for Bad debt

expense, A/R

5. Estimate of Bad Debt Expense Transaction •Bad debt expense,

Allowance for uncollectible

accounts

…Step 2: Divide Financial Statements in to Cycles

Classes of transactions and accounts in Sales and Collection Cycle

34.

…Steps to developan audit Objective

•

…Step 2: Divide Financial Statements in to Cycles

•

2. Acquisition and payment cycle (A);

Involves transactions related to :

the acquisitions of goods and services used in

operation

the cash disbursements for those acquisitions

Purchase returns & allowances, purchase discounts

•

3. Payroll and personnel cycle (P) Involves transactions

related to

Payment of salary expenses

Accrual of salaries incurred but not paid

Withheld of payroll related taxes, allocation of labor

cost in to DL,IL

35.

Audit I YAAAUSC 2022

• 4. Inventory and warehousing cycle (I)

This cycle is unique because it has close

relationships to other transaction cycles .

Involve acquisition of raw materials,

labor, and others-this relates to

Acquisition & Payment cycle

Involve shipping goods and record

revenue and costs -this relates to Sales &

Collection cycle

36.

…Steps to developan audit Objective

•

..Step 2: Divide Financial Statements in to Cycles

•

5. Capital acquisition and repayment cycle (C)

•

-Transactions in the capital acquisition and repayment cycle

are related to financing the business, such as issuing stock or

debt, paying dividends, and repaying debt.

Identifying account balances belonging to different

transaction cycles

– It is logical to use the cycle approach since it agrees with

the way transactions are recorded in journals and

summarized in the general ledger and FSs.

– eg, Sales, Sales returns, Cash receipts, Estimate and Write-

offs of Uncollectible accounts are the five classes of

transactions that cause accounts receivable to increase

and decrease.

– Therefore, they are all parts of the sales and collection

37.

…Steps to developan audit Objective

•

..Step 2: Divide Financial Statements in to Cycles

Identifying account balances belonging to different

transaction cycles

– Trial balance - is a primary focus of every audit as it is

the starting point to prepare financial statements.

– The letter representing a cycle is shown for each account

in the left column beside the account name.

Note:

-Each account has at least one cycle associated with it, and

only cash and inventory are a part of two or more

cycles.

– Some journals and general ledger accounts are included in

more than one cycle; which shows the journal is used to

record transactions from more than one cycle and indicates a

tie-in between the cycles.

38.

Audit I YAAAUSC 2022

The most important general ledger account included in

and affecting several cycles is general cash (cash in

bank).

– General cash connects most cycles.

Although auditors need to consider the

interrelationships between cycles, they typically treat

cycles independently to the extent practical to manage

complex audits effectively.

39.

…Steps to developan audit Objective

•

..Step 2: Divide Financial Statements in to Cycles

•

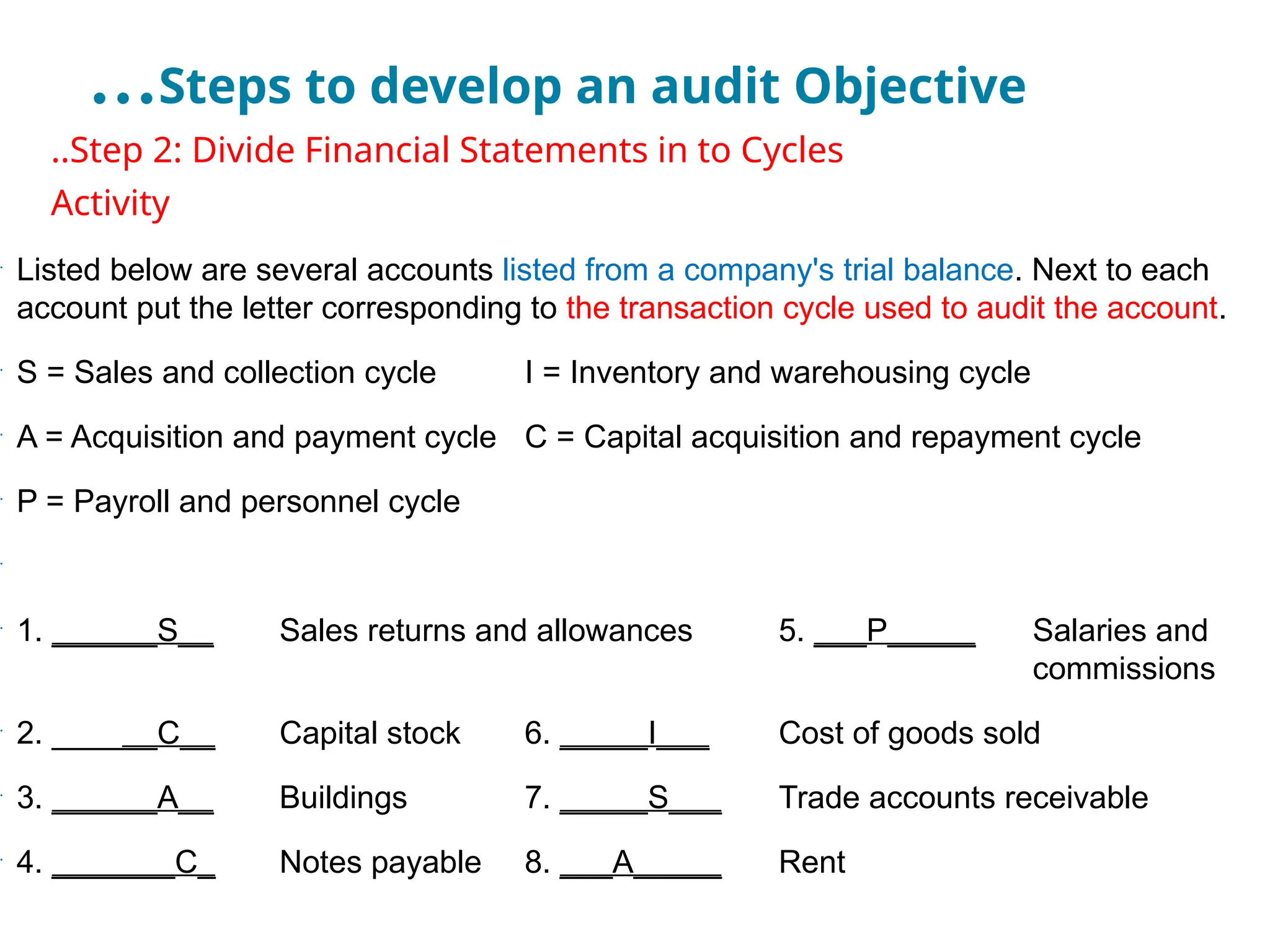

Activity

•

Listed below are several accounts listed from a company's trial balance. Next to each

account put the letter corresponding to the transaction cycle used to audit the account.

•

S = Sales and collection cycle I = Inventory and warehousing cycle

•

A = Acquisition and payment cycle C = Capital acquisition and repayment cycle

•

P = Payroll and personnel cycle

•

•

1. ______S__ Sales returns and allowances 5. ___P_____ Salaries and

commissions

•

2. ______C__ Capital stock 6. _____I___ Cost of goods sold

•

3. ______A__ Buildings 7. _____S___ Trade accounts receivable

•

4. _______C_ Notes payable 8. ___A_____ Rent

40.

Steps to developan audit Objective

•

Step 3: Setting Audit Objectives

Since the objective of an audit is to express opinion

that financial statements are fairly stated, they

develop audit objectives that test each management

assertions

•

Management assertions

– Management is responsible for the preparation of

financial statements that give a true and fair view.

– Assertions are implied or expressed representations

made by the client’s management about classes of

transactions, account balances and disclosures in the

financial statements

– Assertions are tested by the auditor to check the

different types of potential misstatements that may

occur

41.

Audit I YAAAUSC 2022

– Financial statements represent -management's

assertions

– Management assertions are directly related to the

financial reporting framework used by the company

(usually U.S. GAAP or IFRS)

Why Assertions matter for the Auditor?

– The auditor’s responsibility is to determine whether

management assertions - about financial statements

are justified.

42.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

= In order to provide opinion on financial

statements, it is necessary to test transactions, balances

and disclosures.

•

-Management assertions are classified in to three

categories:

1. Transaction –related assertions- Assertions about

transactions and events

2. Balance –related assertions- Assertions about

account balances

3. Disclosure –related assertions- Assertions about

Disclosures

43.

…Steps to developan audit Objective

•

Step 3: Setting Audit Objectives

•

…..Management Assertions

•

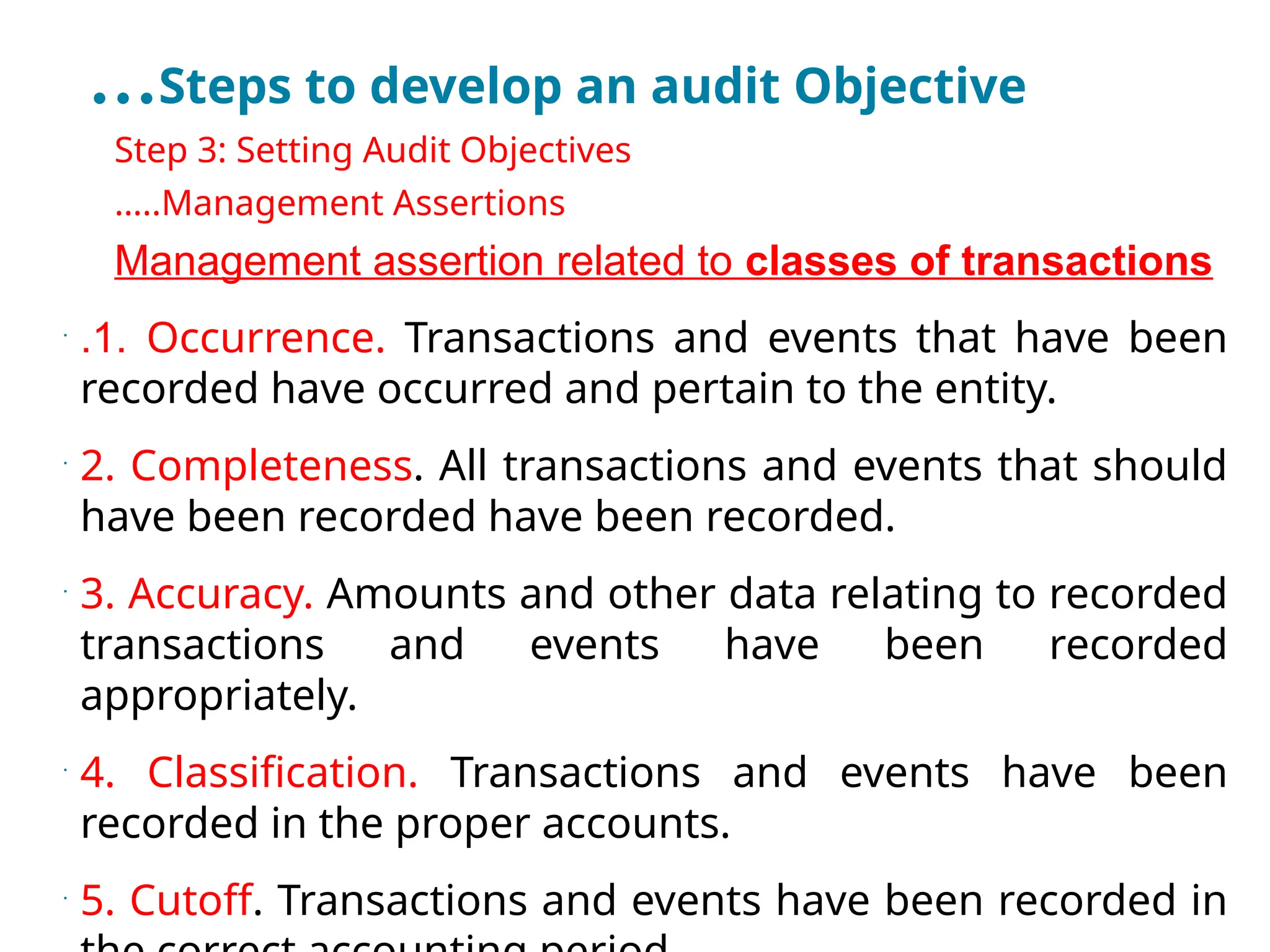

Management assertion related to classes of transactions

•

.1. Occurrence. Transactions and events that have been

recorded have occurred and pertain to the entity.

•

2. Completeness. All transactions and events that should

have been recorded have been recorded.

•

3. Accuracy. Amounts and other data relating to recorded

transactions and events have been recorded

appropriately.

•

4. Classification. Transactions and events have been

recorded in the proper accounts.

•

5. Cutoff. Transactions and events have been recorded in

44.

…Steps to developan audit Objective

•

Step 3: Setting Audit Objectives

•

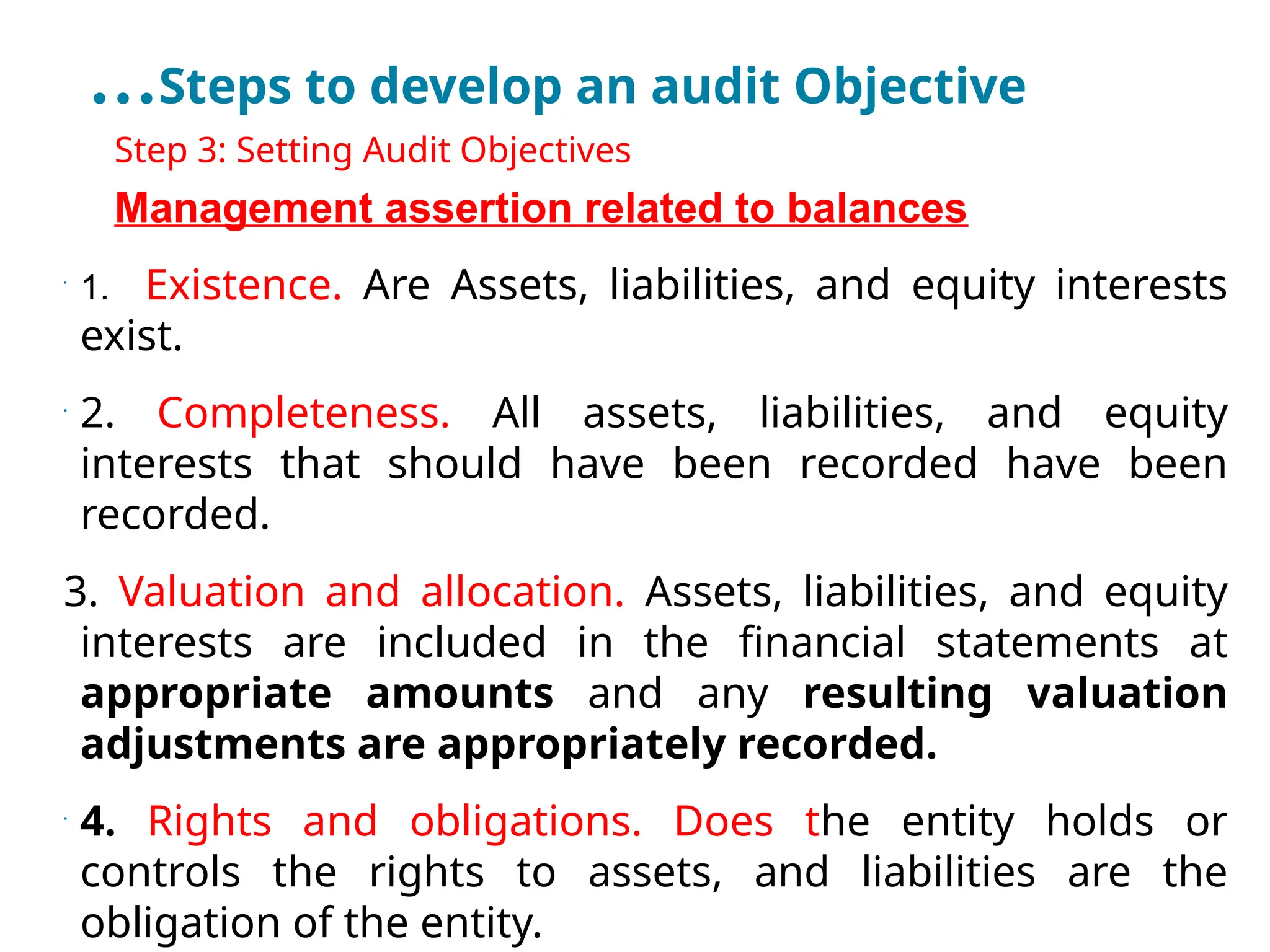

Management assertion related to balances

•

1. Existence. Are Assets, liabilities, and equity interests

exist.

•

2. Completeness. All assets, liabilities, and equity

interests that should have been recorded have been

recorded.

3. Valuation and allocation. Assets, liabilities, and equity

interests are included in the financial statements at

appropriate amounts and any resulting valuation

adjustments are appropriately recorded.

•

4. Rights and obligations. Does the entity holds or

controls the rights to assets, and liabilities are the

obligation of the entity.

45.

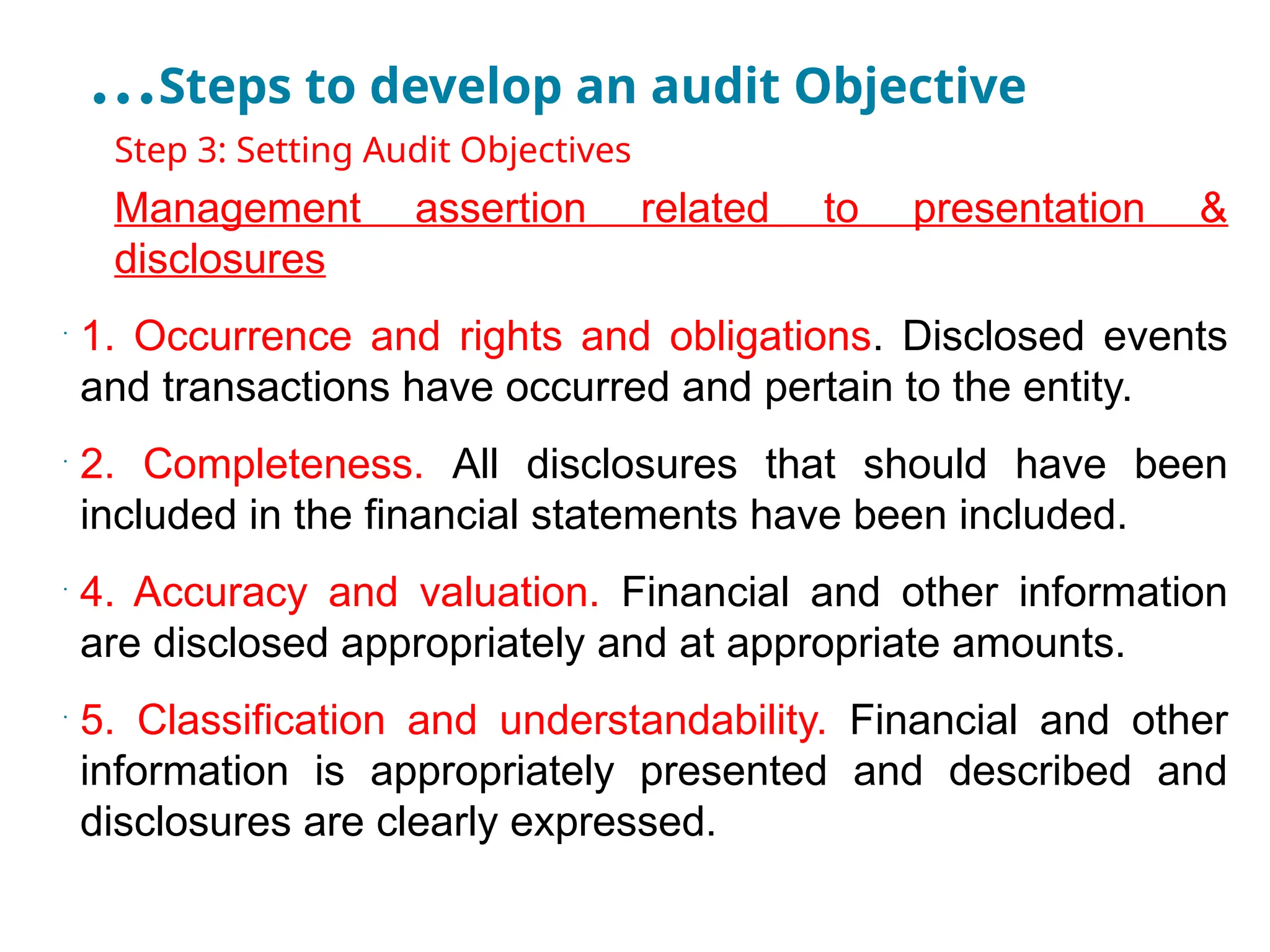

…Steps to developan audit Objective

•

Step 3: Setting Audit Objectives

•

Management assertion related to presentation &

disclosures

•

1. Occurrence and rights and obligations. Disclosed events

and transactions have occurred and pertain to the entity.

•

2. Completeness. All disclosures that should have been

included in the financial statements have been included.

•

4. Accuracy and valuation. Financial and other information

are disclosed appropriately and at appropriate amounts.

•

5. Classification and understandability. Financial and other

information is appropriately presented and described and

disclosures are clearly expressed.

46.

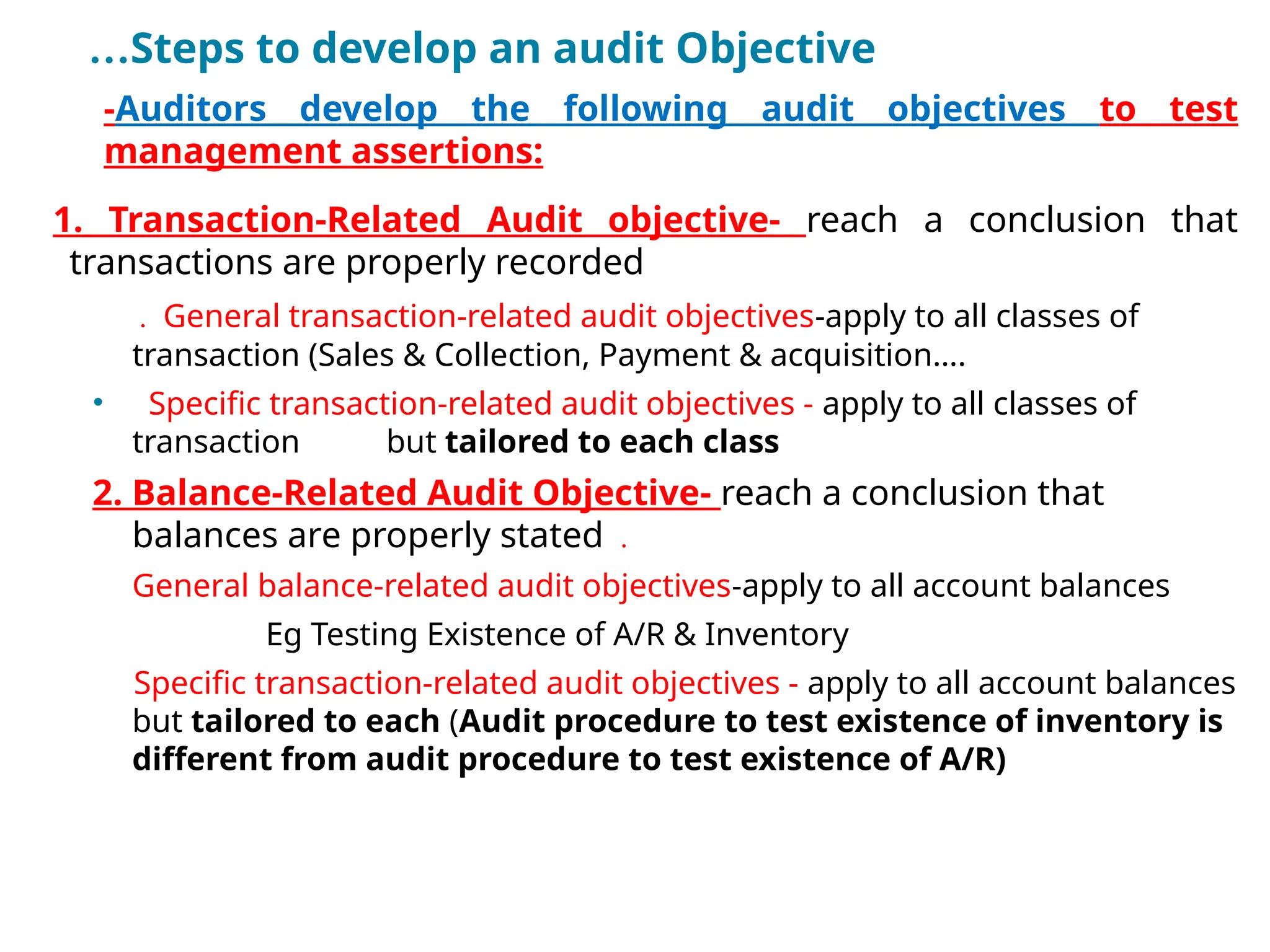

…Steps to developan audit Objective

•

-Auditors develop the following audit objectives to test

management assertions:

1. Transaction-Related Audit objective- reach a conclusion that

transactions are properly recorded

. General transaction-related audit objectives-apply to all classes of

transaction (Sales & Collection, Payment & acquisition….

• Specific transaction-related audit objectives - apply to all classes of

transaction but tailored to each class

2. Balance-Related Audit Objective- reach a conclusion that

balances are properly stated .

General balance-related audit objectives-apply to all account balances

Eg Testing Existence of A/R & Inventory

Specific transaction-related audit objectives - apply to all account balances

but tailored to each (Audit procedure to test existence of inventory is

different from audit procedure to test existence of A/R)

47.

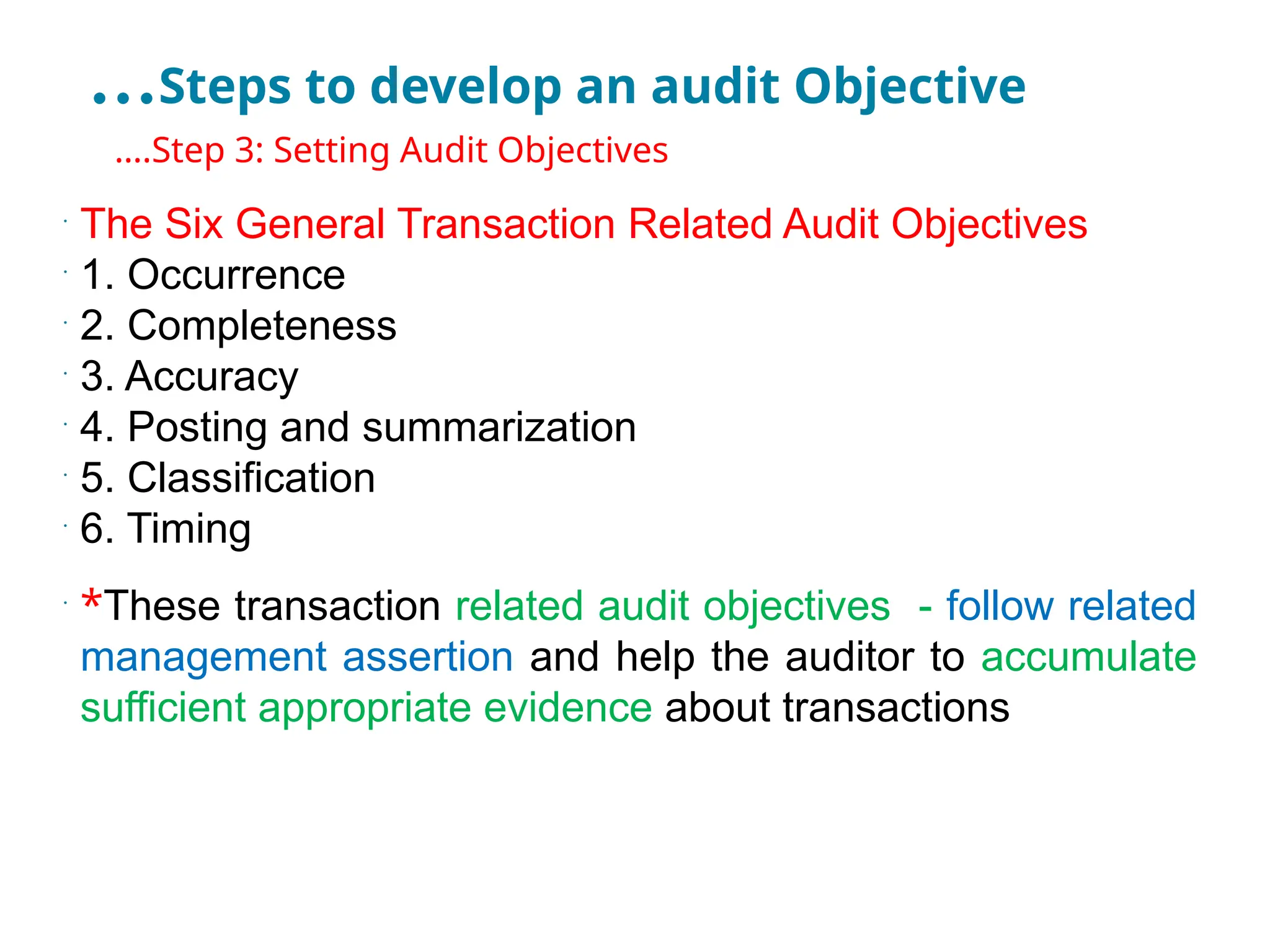

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

The Six General Transaction Related Audit Objectives

•

1. Occurrence

•

2. Completeness

•

3. Accuracy

•

4. Posting and summarization

•

5. Classification

•

6. Timing

•

*These transaction related audit objectives - follow related

management assertion and help the auditor to accumulate

sufficient appropriate evidence about transactions

48.

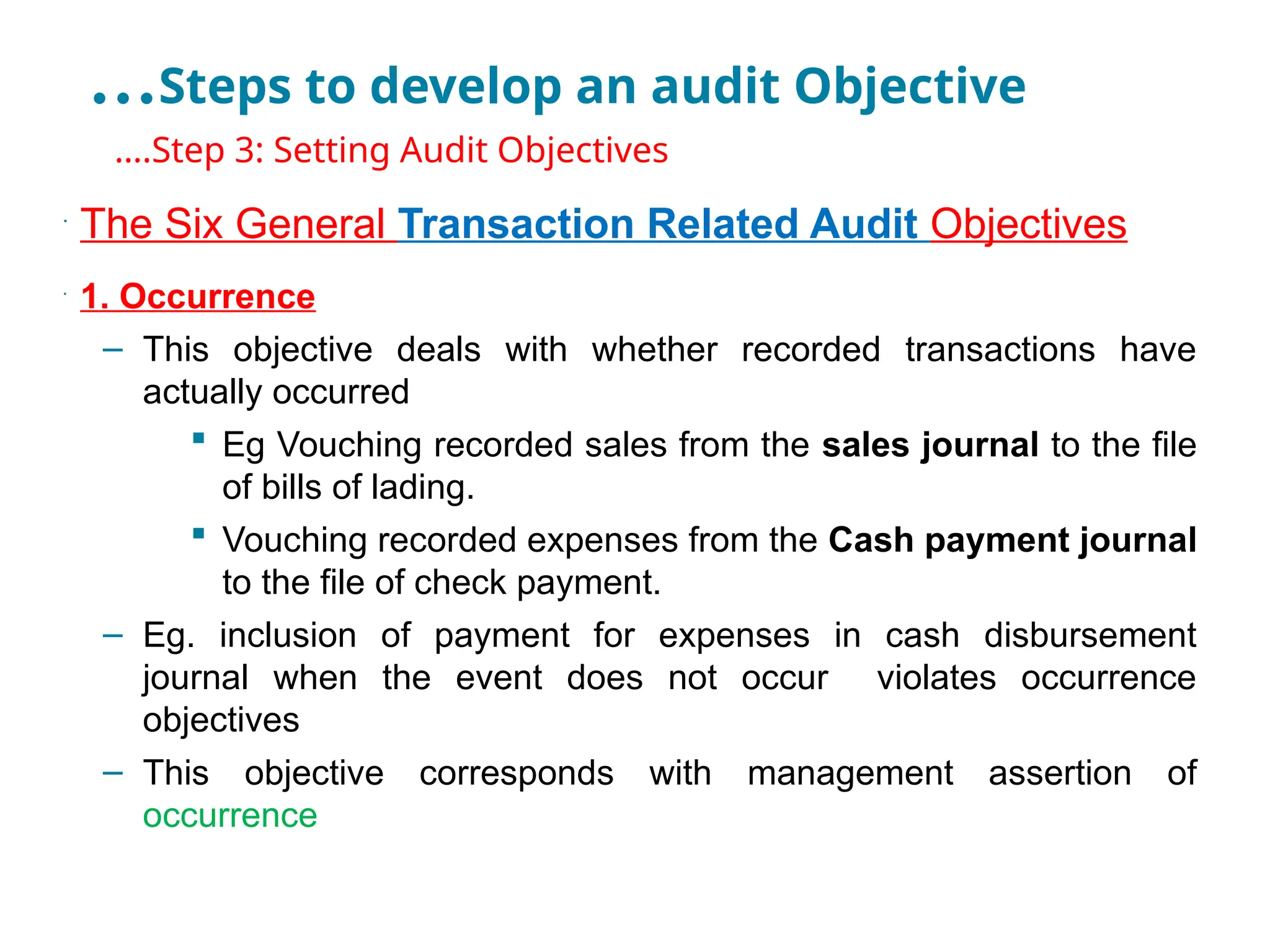

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

The Six General Transaction Related Audit Objectives

•

1. Occurrence

– This objective deals with whether recorded transactions have

actually occurred

Eg Vouching recorded sales from the sales journal to the file

of bills of lading.

Vouching recorded expenses from the Cash payment journal

to the file of check payment.

– Eg. inclusion of payment for expenses in cash disbursement

journal when the event does not occur violates occurrence

objectives

– This objective corresponds with management assertion of

occurrence

49.

…Steps to developan audit Objective

•

..The Six General Transaction Related Audit Objectives

•

2. Completeness

– This objective deals with whether all transactions that should be

included in the journals have actually been included

Auditors account for the sequence of pre-numbered sales

invoices to check completeness

– Eg. Failure to include a sales in a sales journal when a sale

occurred violates the completeness objectives

– This objective corresponds with management assertion of

completeness

Occurrence is checked to see if there is overstatement

Completeness is checked to see if there is understatement

due to unrecorded transactions

50.

…Steps to developan audit Objective

•

…The Six General Transaction Related Audit Objectives

•

3. Accuracy

– This objective deals with the accuracy of information

for accounting transactions

– Eg. in recording sales, if the quantity shipped is

different from what is billed, or

– if wrong selling price is used,

– if wrong amount is recorded in sales journal,

it is considered as a violation of the accuracy

objectives

– This objective tests management’s assertion of

valuation or allocation

51.

…Steps to developan audit Objective

•

…The Six General Transaction Related Audit Objectives

•

4. Posting and summarization

– This objective involves determining whether

transactions recorded in journals are transferred to

the appropriate general and subsidiary ledger

accounts

Eg.

- if a receivable from customer “A” is recorded in Customer “B”s

subsidiary ledger, or

- if the control ledger shows an amount different from the summary

of subsidiary ledgers, it is considered as violation of the posting

and summarization objectives

– This objective also tests management’s assertion of valuation or

allocation

– The use of computerized system usually reduce this problem

52.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

..The Six General Transaction Related Audit Objectives

•

5. Classification

– This objective involves determining whether transactions are

properly coded/classified

– Eg. error in classifying cash sales as credit sales,

– recording collections from sale of operating fixed assets as

revenue,

– Both are violation of the classification objectives

6. Timing

– This objective involves determining whether the transactions are

recorded in the correct date the transaction take place

– Eg. A sales transaction should be recorded at the time of

shipment (when title passes)

– This objective is also tests management’s assertion of valuation or

allocation

53.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

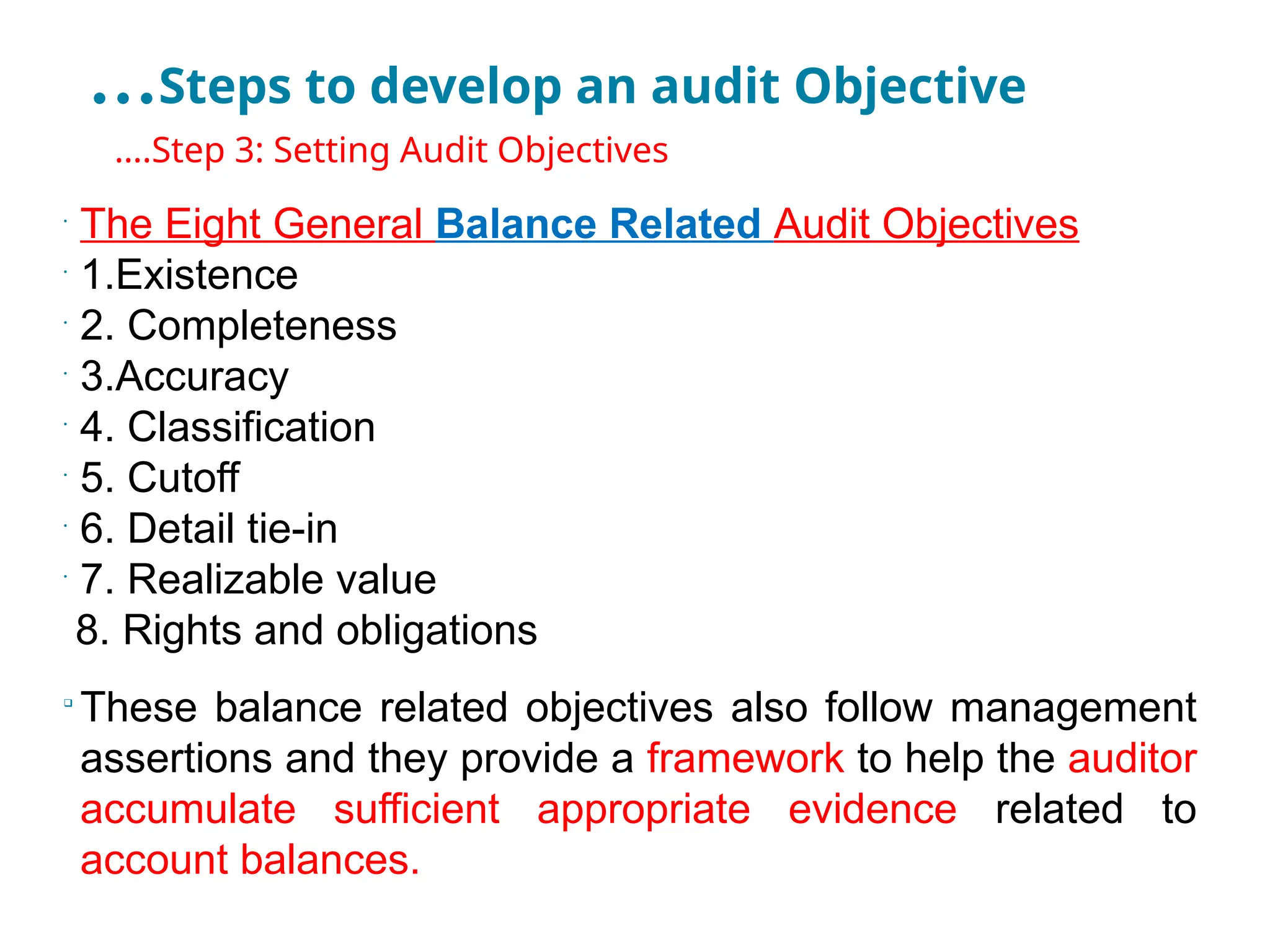

The Eight General Balance Related Audit Objectives

•

1.Existence

•

2. Completeness

•

3.Accuracy

•

4. Classification

•

5. Cutoff

•

6. Detail tie-in

•

7. Realizable value

8. Rights and obligations

These balance related objectives also follow management

assertions and they provide a framework to help the auditor

accumulate sufficient appropriate evidence related to

account balances.

54.

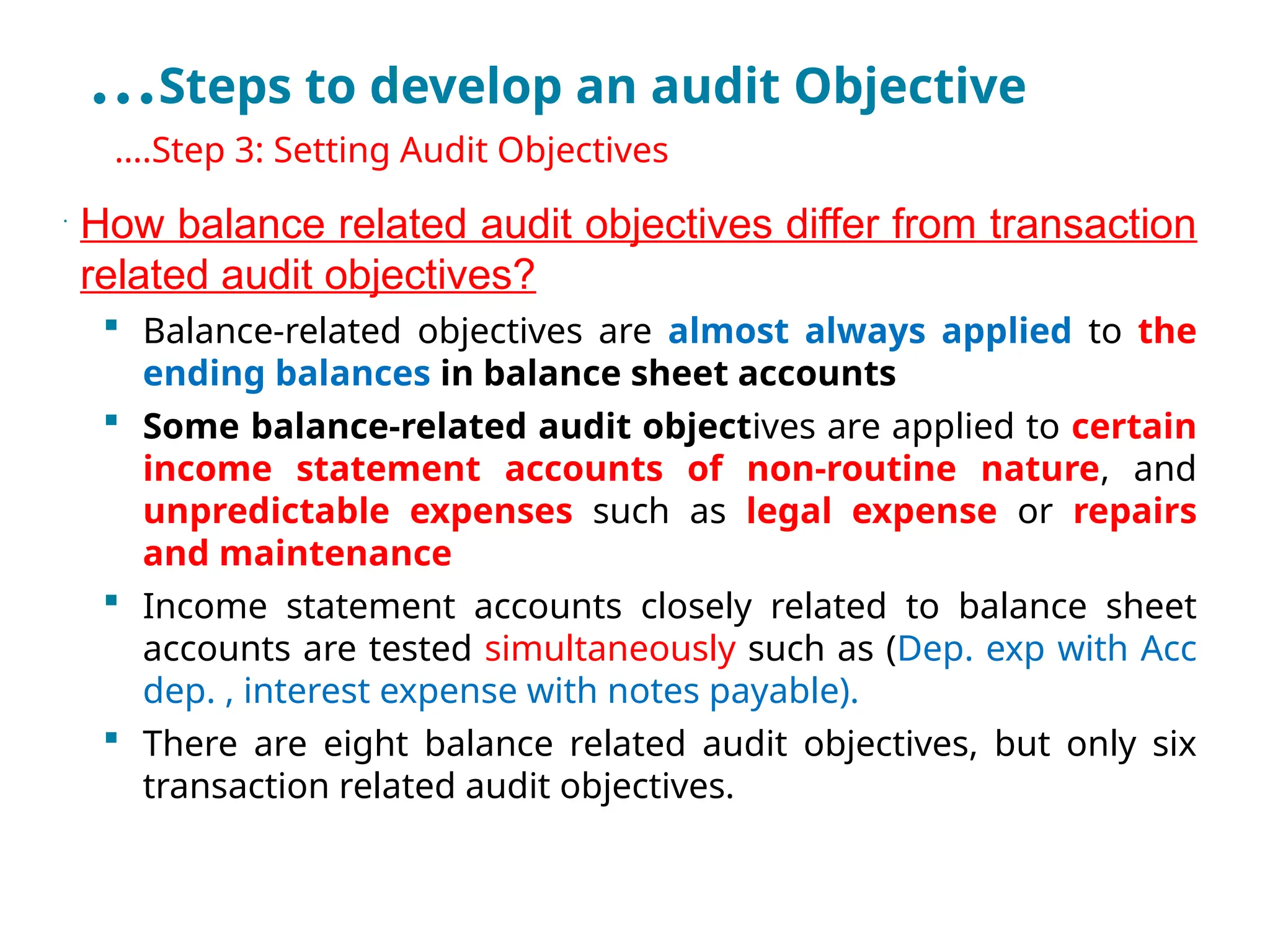

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

How balance related audit objectives differ from transaction

related audit objectives?

Balance-related objectives are almost always applied to the

ending balances in balance sheet accounts

Some balance-related audit objectives are applied to certain

income statement accounts of non-routine nature, and

unpredictable expenses such as legal expense or repairs

and maintenance

Income statement accounts closely related to balance sheet

accounts are tested simultaneously such as (Dep. exp with Acc

dep. , interest expense with notes payable).

There are eight balance related audit objectives, but only six

transaction related audit objectives.

55.

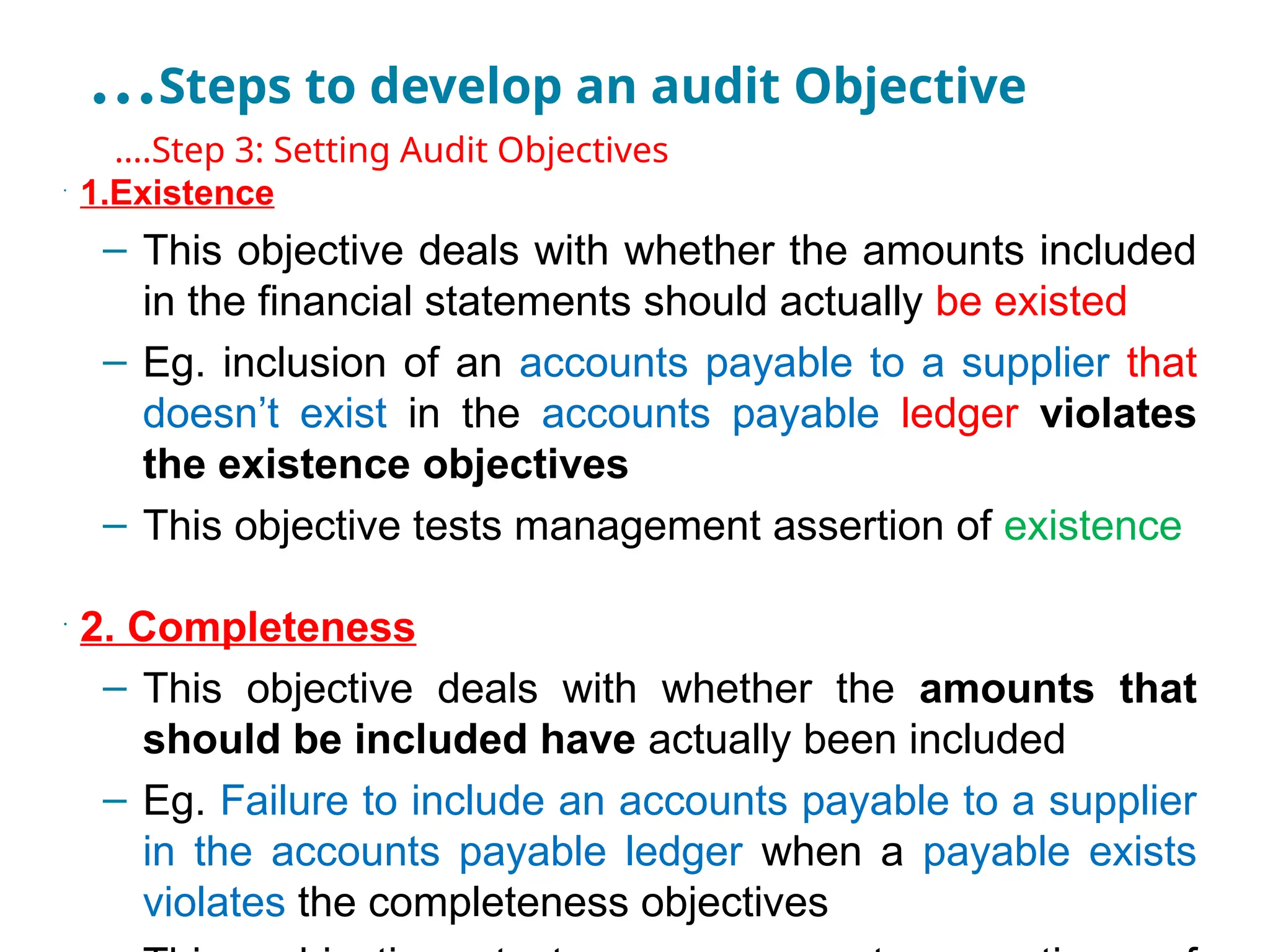

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

1.Existence

– This objective deals with whether the amounts included

in the financial statements should actually be existed

– Eg. inclusion of an accounts payable to a supplier that

doesn’t exist in the accounts payable ledger violates

the existence objectives

– This objective tests management assertion of existence

•

2. Completeness

– This objective deals with whether the amounts that

should be included have actually been included

– Eg. Failure to include an accounts payable to a supplier

in the accounts payable ledger when a payable exists

violates the completeness objectives

56.

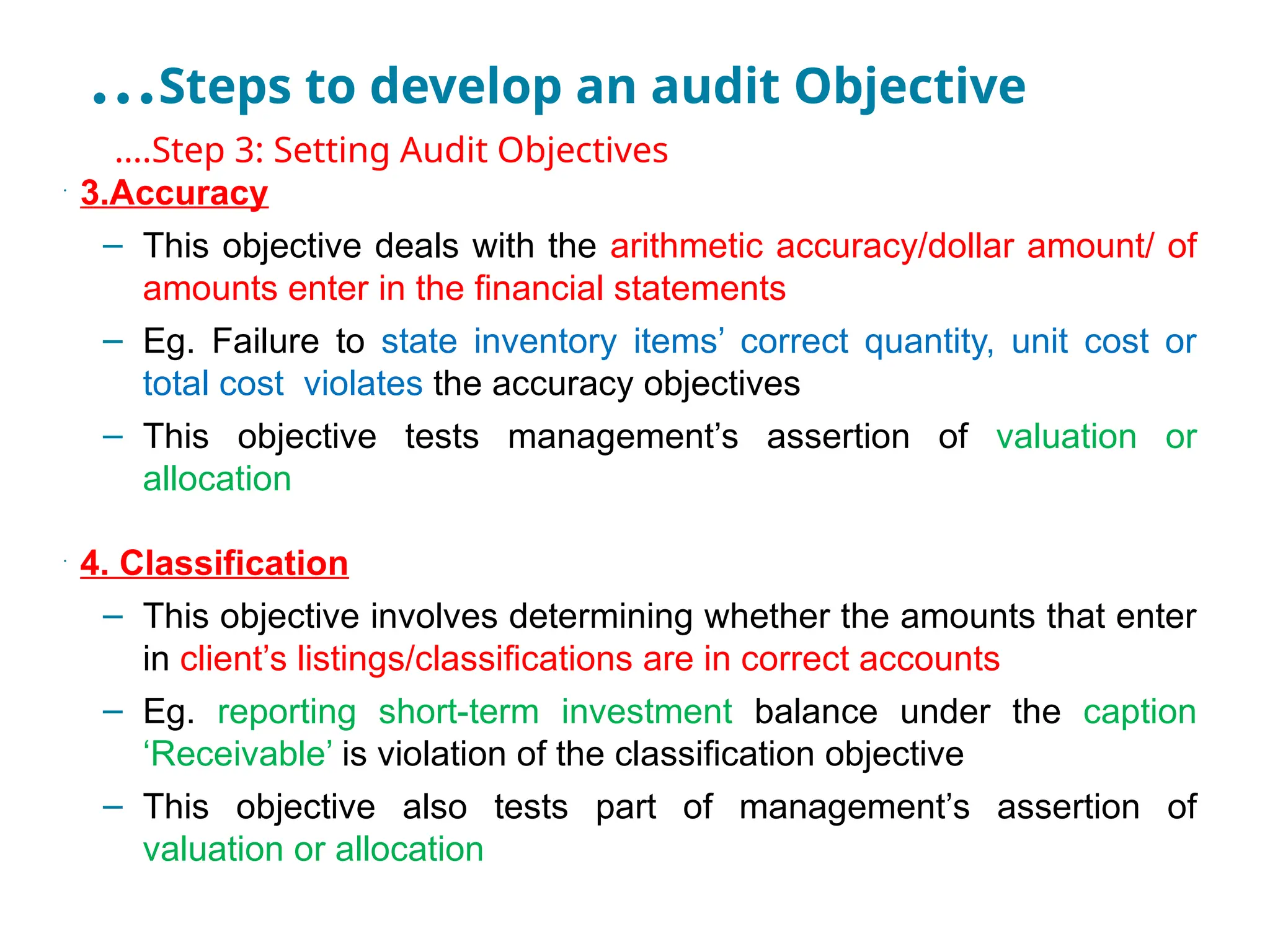

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

3.Accuracy

– This objective deals with the arithmetic accuracy/dollar amount/ of

amounts enter in the financial statements

– Eg. Failure to state inventory items’ correct quantity, unit cost or

total cost violates the accuracy objectives

– This objective tests management’s assertion of valuation or

allocation

•

4. Classification

– This objective involves determining whether the amounts that enter

in client’s listings/classifications are in correct accounts

– Eg. reporting short-term investment balance under the caption

‘Receivable’ is violation of the classification objective

– This objective also tests part of management’s assertion of

valuation or allocation

57.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

…The Eight General Balance Related Audit Objectives

•

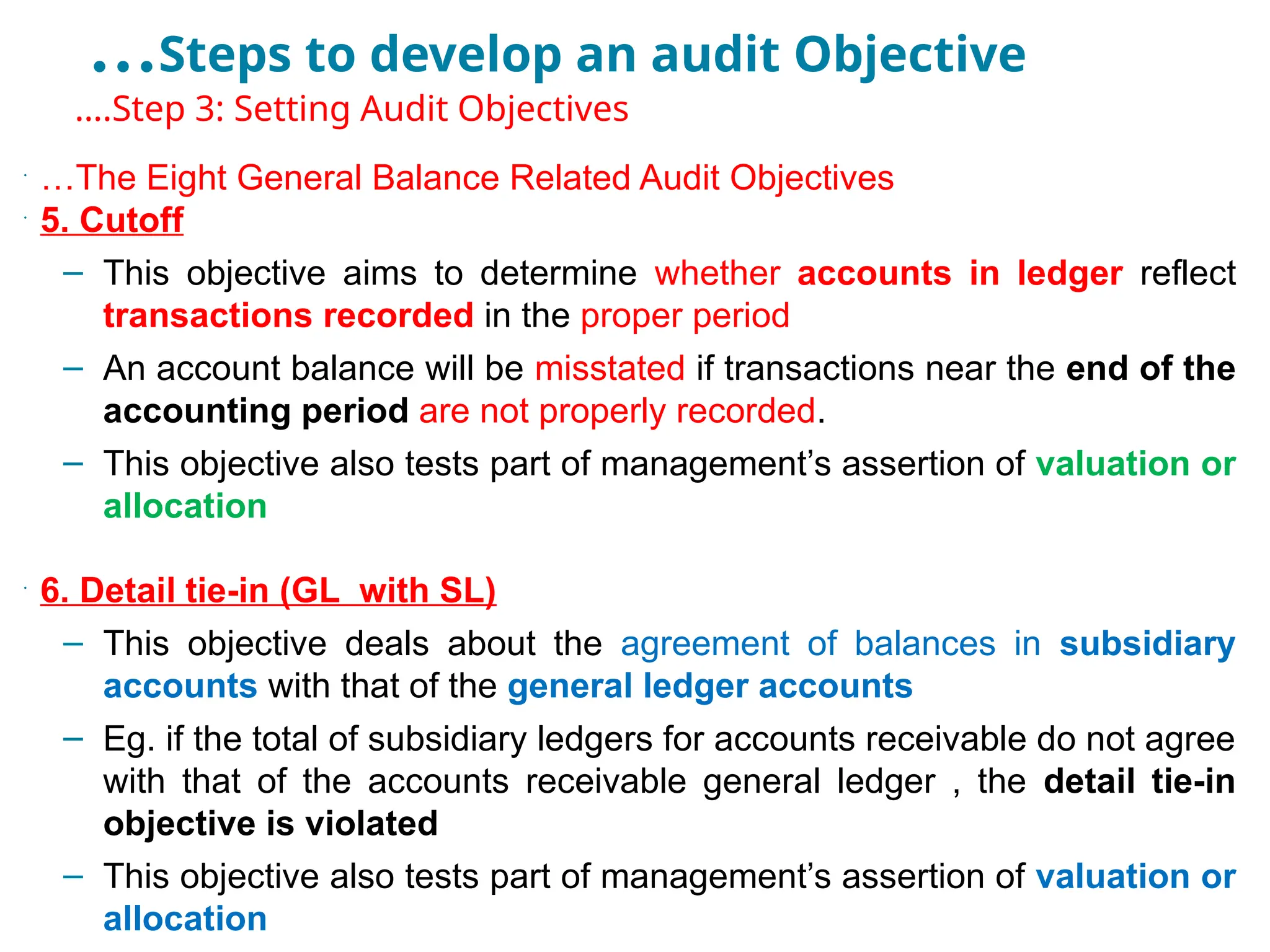

5. Cutoff

– This objective aims to determine whether accounts in ledger reflect

transactions recorded in the proper period

– An account balance will be misstated if transactions near the end of the

accounting period are not properly recorded.

– This objective also tests part of management’s assertion of valuation or

allocation

•

6. Detail tie-in (GL with SL)

– This objective deals about the agreement of balances in subsidiary

accounts with that of the general ledger accounts

– Eg. if the total of subsidiary ledgers for accounts receivable do not agree

with that of the accounts receivable general ledger , the detail tie-in

objective is violated

– This objective also tests part of management’s assertion of valuation or

allocation

58.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

…The Eight General Balance Related Audit Objectives

•

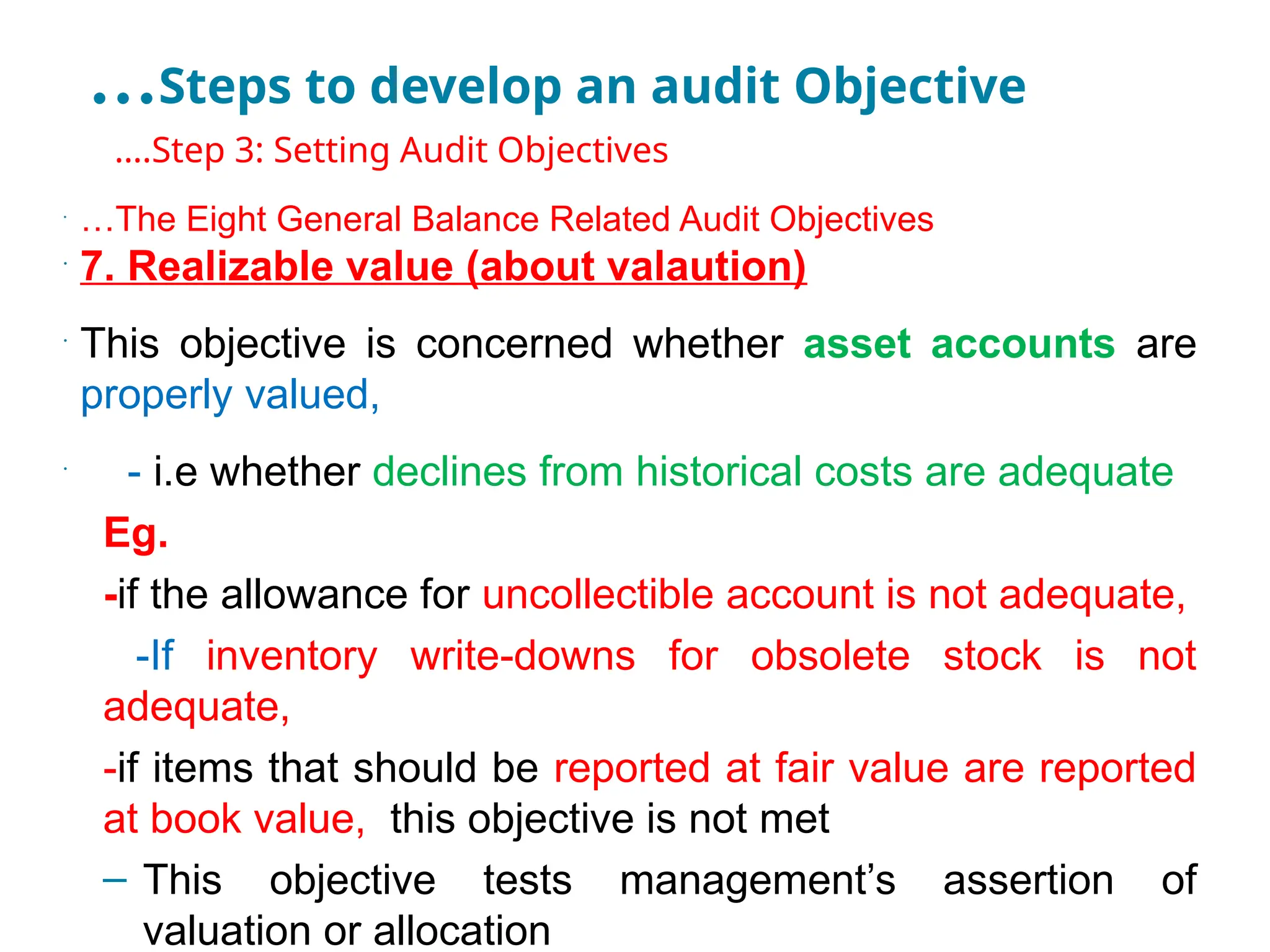

7. Realizable value (about valaution)

•

This objective is concerned whether asset accounts are

properly valued,

•

- i.e whether declines from historical costs are adequate

Eg.

-if the allowance for uncollectible account is not adequate,

-If inventory write-downs for obsolete stock is not

adequate,

-if items that should be reported at fair value are reported

at book value, this objective is not met

– This objective tests management’s assertion of

valuation or allocation

59.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

•

…The Eight General Balance Related Audit Objectives

•

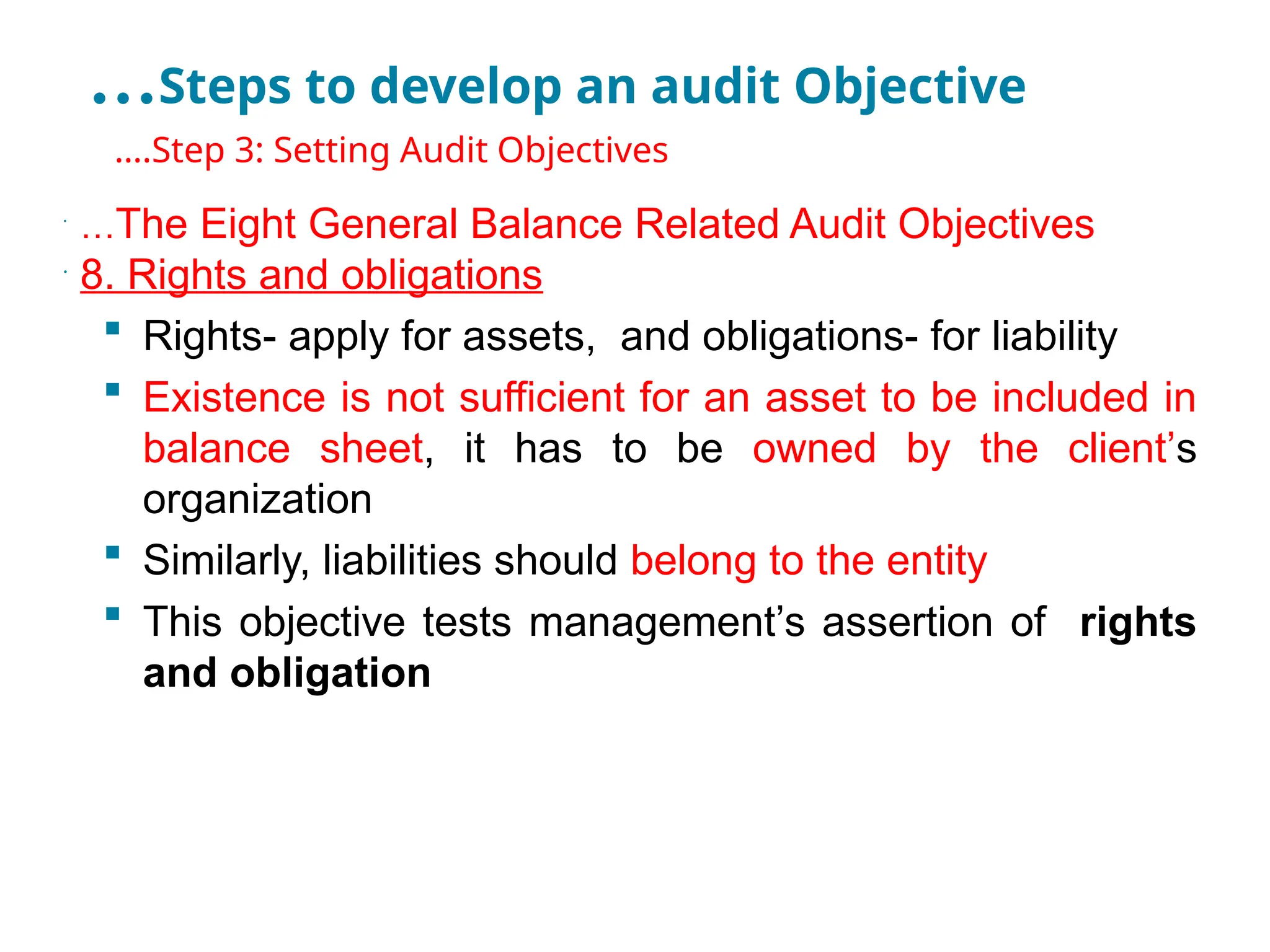

8. Rights and obligations

Rights- apply for assets, and obligations- for liability

Existence is not sufficient for an asset to be included in

balance sheet, it has to be owned by the client’s

organization

Similarly, liabilities should belong to the entity

This objective tests management’s assertion of rights

and obligation

60.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

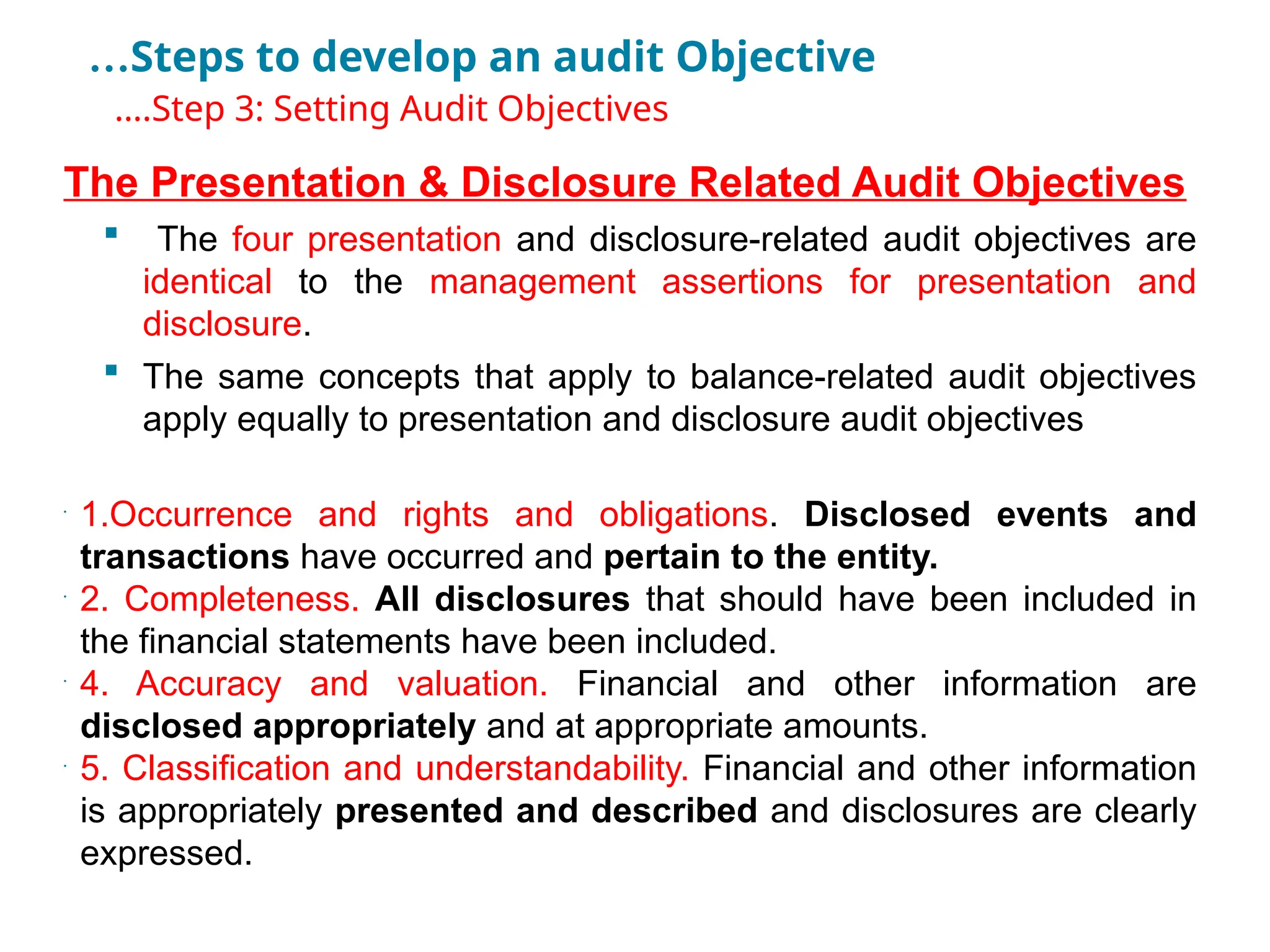

The Presentation & Disclosure Related Audit Objectives

The four presentation and disclosure-related audit objectives are

identical to the management assertions for presentation and

disclosure.

The same concepts that apply to balance-related audit objectives

apply equally to presentation and disclosure audit objectives

•

1.Occurrence and rights and obligations. Disclosed events and

transactions have occurred and pertain to the entity.

•

2. Completeness. All disclosures that should have been included in

the financial statements have been included.

•

4. Accuracy and valuation. Financial and other information are

disclosed appropriately and at appropriate amounts.

•

5. Classification and understandability. Financial and other information

is appropriately presented and described and disclosures are clearly

expressed.

61.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

Relationships between Audit Objectives

There is a significant overlap between the transaction-

related and balance-related audit objectives.

Rights and obligations is the only balance-related

assertion without a similar transaction-related assertion.

Presentation and disclosure-related audit objectives are

closely related to the balance-related audit objectives.

Auditors often consider presentation and disclosure

audit objectives when addressing the balance related

audit objectives.

62.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

How Audit Objectives are Met?

-

The auditor must obtain sufficient appropriate audit

evidence to support all management assertions in the

financial statements.

This is done by accumulating evidence in support of

some appropriate combination of transaction-related

audit objectives and balance-related audit objectives.

The auditor must decide the appropriate audit objectives

and the evidence to accumulate, to meet those

objectives on every audit

63.

…Steps to developan audit Objective

•

….Step 3: Setting Audit Objectives

..How Audit Objectives are Met?

To accumulate evidence that enables to achieve audit

objectives, auditors follow the audit process.

The audit process -= is a well-defined methodology for

organizing an audit to ensure that the evidence

gathered is both sufficient and appropriate and that all

required audit objectives are both specified and met.

- The auditor should know the legal and operating

environment in which the client organization operates, and

also the reporting requirement so that the audit plan can

meet the objectives associated with reporting requirements

in the industry

64.

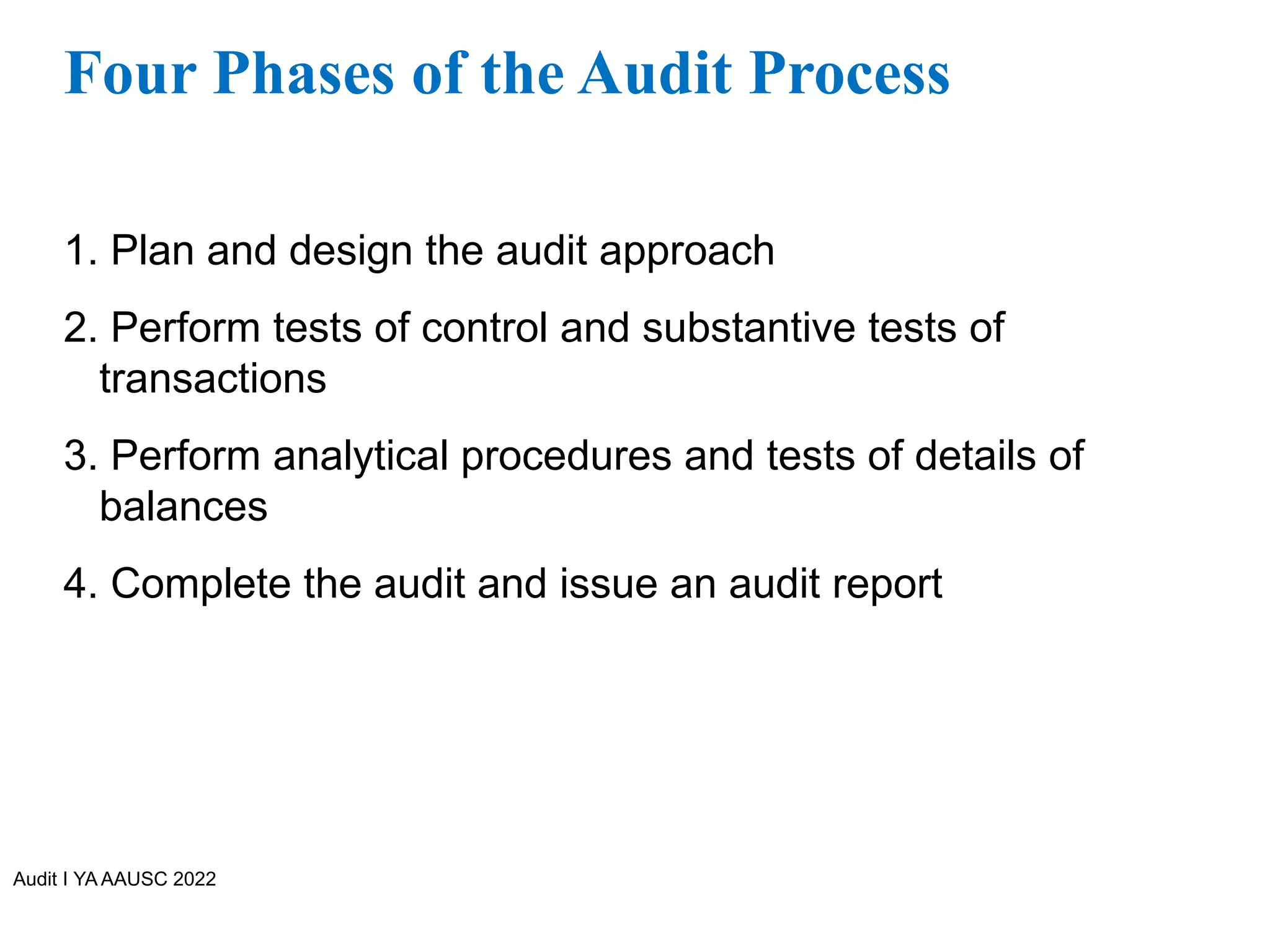

Audit I YAAAUSC 2022

Four Phases of the Audit Process

1. Plan and design the audit approach

2. Perform tests of control and substantive tests of

transactions

3. Perform analytical procedures and tests of details of

balances

4. Complete the audit and issue an audit report

Audit I YAAAUSC 2022

Audit assertions

• Auditors need to use assertions when assessing the risk of

material misstatement and designing audit procedures.

How—by collecting evidence

• Means- auditors need to gather sufficient(how much audit

evidence) and appropriate (tripe of evidence)evidence

about each assertion for each transaction and account

balance or disclosure.

67.

Audit I YAAAUSC 2022

Assertions about classes of transactions and Events

P/L Statement

• Occurrence:- Whether transactions actually occurred

during the accounting period – it happened

• Completeness;- whether all transactions that should be

included are in fact included

• Accuracy:- whether transactions have been recorded in

correct journal account

• Classification- Whether transactions are recorded at

correct amounts ( ledgers Drs and Crs)

• Cutoff:- whether transactions are recorded in the proper

accounting period

68.

Audit I YAAAUSC 2022

Assertions about account balances : Balance

sheet B/S

• Existence: whether A, L, and E interests actually existed at

the balance sheet date (are there any fake assets)

• Completeness: whether all the accounts that should be

presented are included (liabilities concerned)

• Valuation (dollar value ) and allocation (Current and

N/current) : whether A, L and E interests have been

included at appropriate amounts

• Rights (ownership/control ) and obligations; whether the

assets are the rights of the entity, and whether the

liabilities are the obligations of the entity.

69.

Audit I YAAAUSC 2022

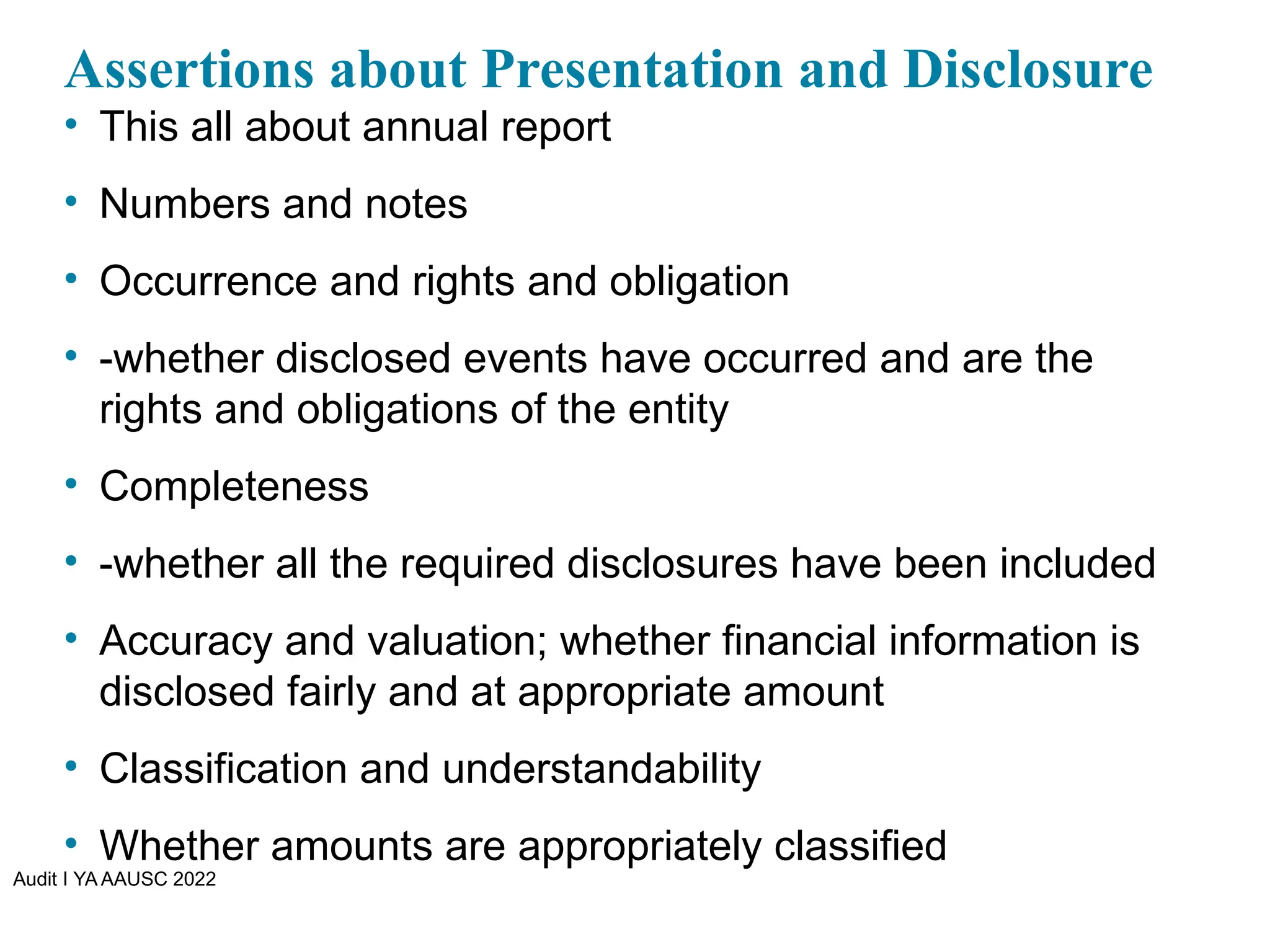

Assertions about Presentation and Disclosure

• This all about annual report

• Numbers and notes

• Occurrence and rights and obligation

• -whether disclosed events have occurred and are the

rights and obligations of the entity

• Completeness

• -whether all the required disclosures have been included

• Accuracy and valuation; whether financial information is

disclosed fairly and at appropriate amount

• Classification and understandability

• Whether amounts are appropriately classified

70.

Audit I YAAAUSC 2022

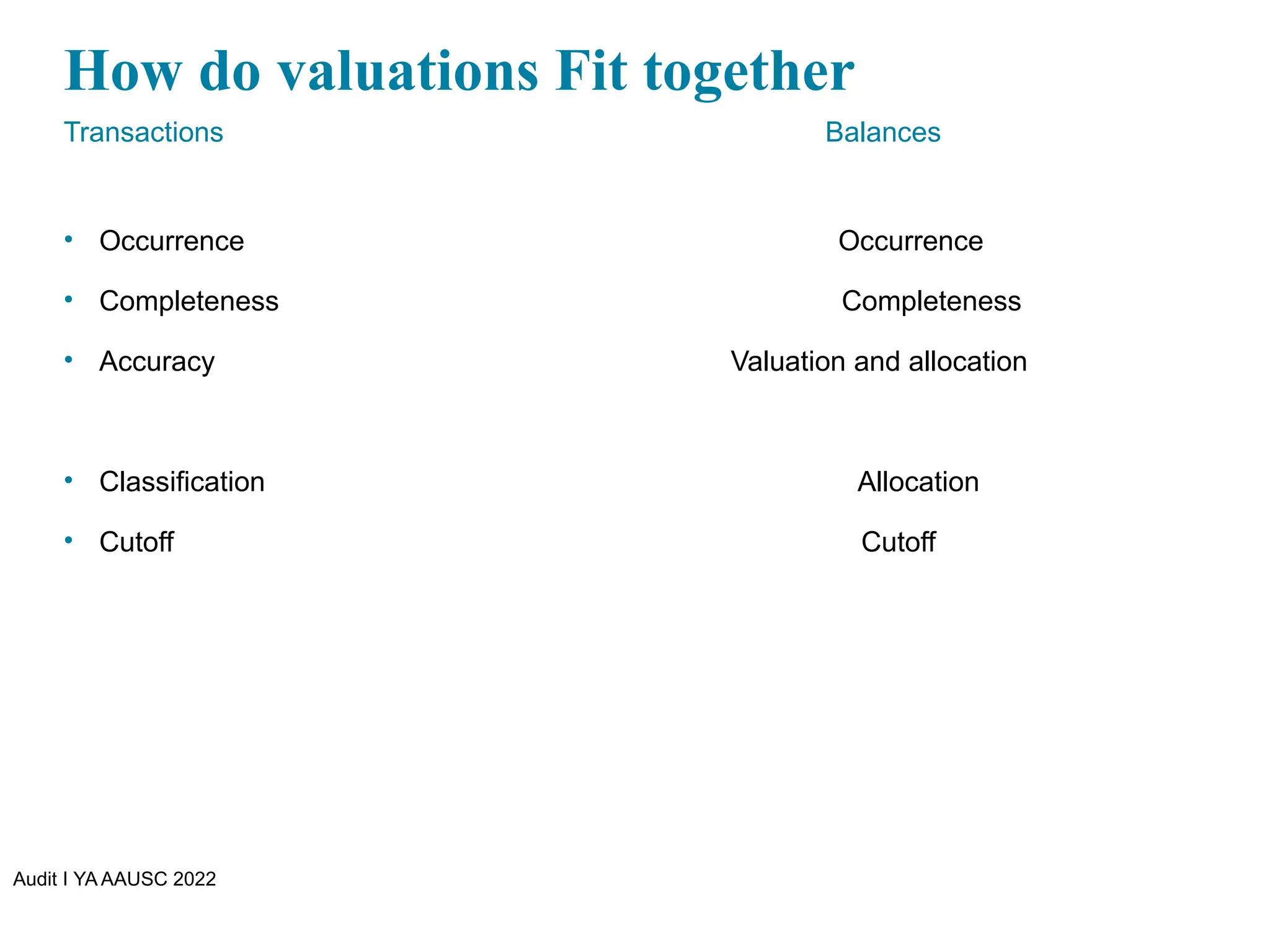

How do valuations Fit together

Transactions Balances

• Occurrence Occurrence

• Completeness Completeness

• Accuracy Valuation and allocation

• Classification Allocation

• Cutoff Cutoff

71.

Audit I YAAAUSC 2022

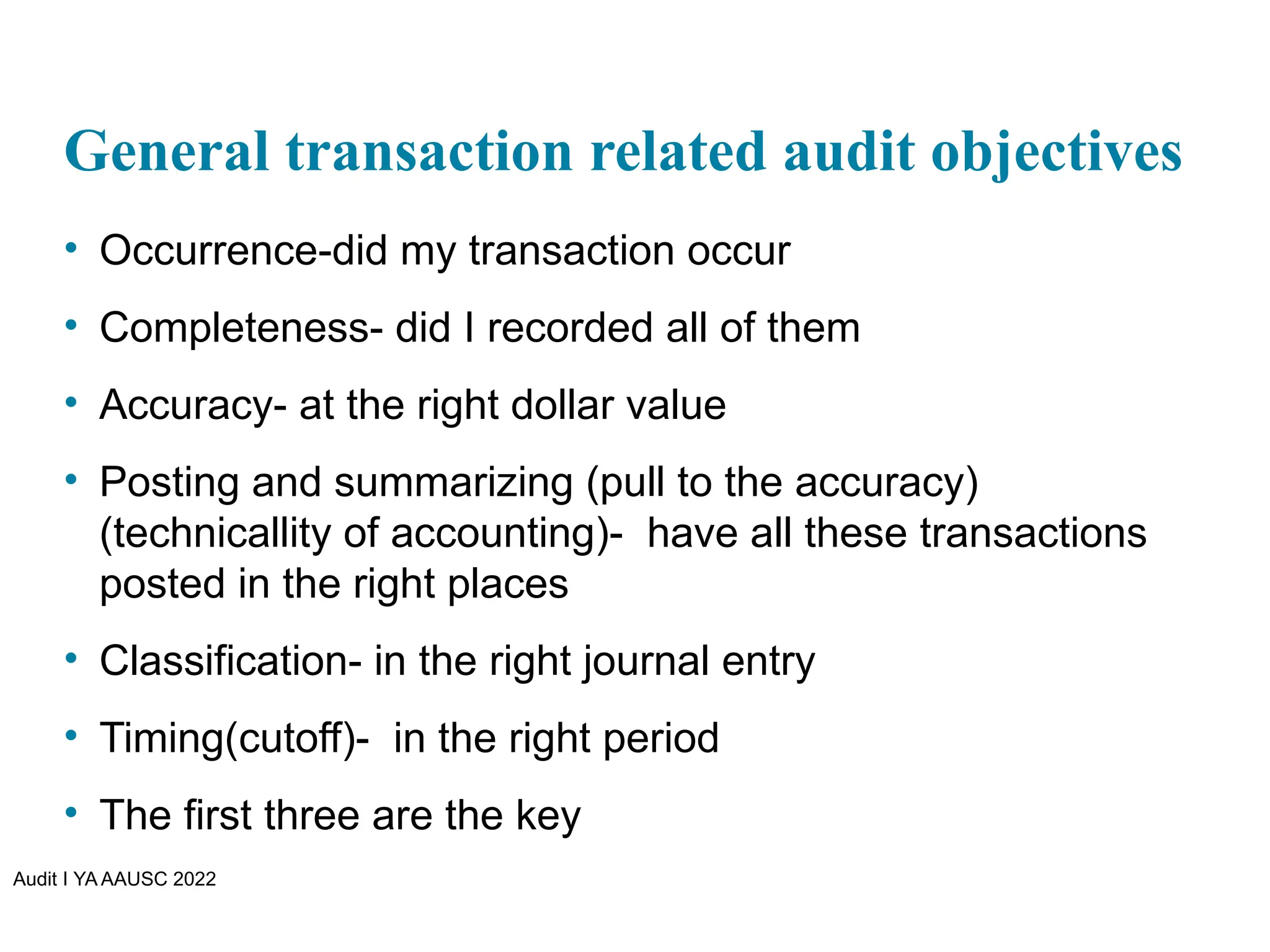

General transaction related audit objectives

• Occurrence-did my transaction occur

• Completeness- did I recorded all of them

• Accuracy- at the right dollar value

• Posting and summarizing (pull to the accuracy)

(technicallity of accounting)- have all these transactions

posted in the right places

• Classification- in the right journal entry

• Timing(cutoff)- in the right period

• The first three are the key

72.

Audit I YAAAUSC 2022

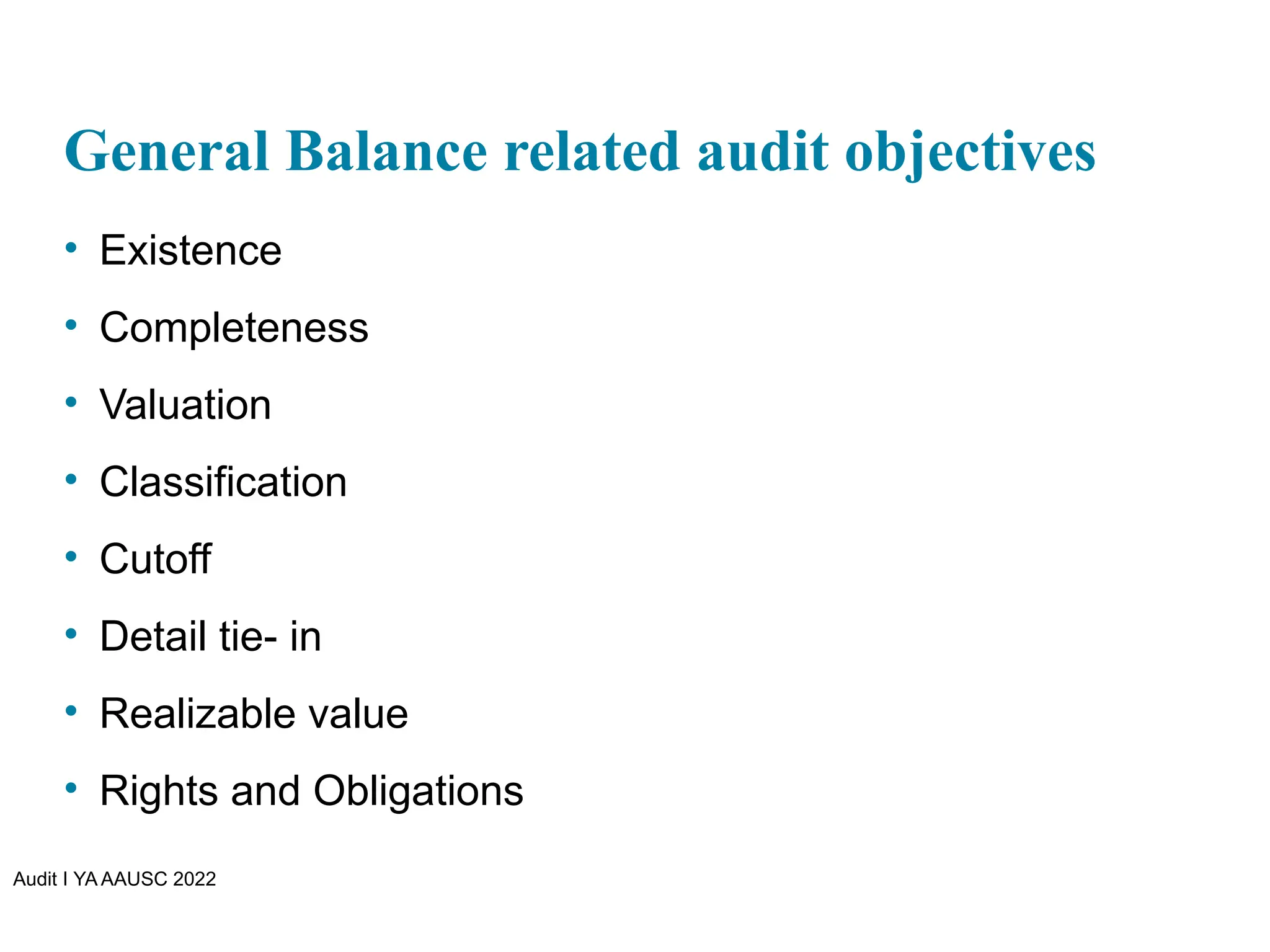

General Balance related audit objectives

• Existence

• Completeness

• Valuation

• Classification

• Cutoff

• Detail tie- in

• Realizable value

• Rights and Obligations

73.

Audit I YAAAUSC 2022

Presentation and dusclosure audit objevtives

• Occurrence and rights and obligations

• Complteness

• Accuracy and valyaution

• Classification and aunderstandability

74.

Audit I YAAAUSC 2022

How audit objectives are met?

The Auditor plans the appropriate combination of:

Audit objectives

The evidence that must be accumulated to meet them

-This plan is called AUDIT PROGRAM (Design)

Audit process is :

A well defined methodology for organizing an audit to

ensure that:

o The evidence gathered is sufficient and appropriate

o All audit objectives are both specified and met.

75.

Audit I YAAAUSC 2022

Four Phases of the Audit Process

1. Plan and design the audit approach

2. Perform tests of control and substantive tests of

transactions

3. Perform analytical procedures and tests of details

of balances

4. Complete the audit and issue an audit report

Editor's Notes

#7 Material= Relevant/important errors in the FS

How do you know is whether material or note+ -Cause and effect, dollar value, impact

#23 Slide 2 is list of textbook LO numbers and statements

#24 Indirect-effect illegal acts do not affect financial statements directly, but result in potential fines. Auditing standards clearly state that auditors provide no assurance that such illegal acts will be detected.

#25 Generally, these laws and regulations relate more to an entity's operating aspects than to its financial and accounting aspects, and their financial statement effect is indirect.

#51 Slide 2 is list of textbook LO numbers and statements

#53 Slide 2 is list of textbook LO numbers and statements

#54 Assertion is a statement one believes is true. How we can prove it is true?

We use a specifoc set of assertions related to the financial statements

Assertions are statements regarding the recognition, measurement, presentation and disclosure of items included in the financial report

#55 Slide 2 is list of textbook LO numbers and statements

#60 Slide 2 is list of textbook LO numbers and statements