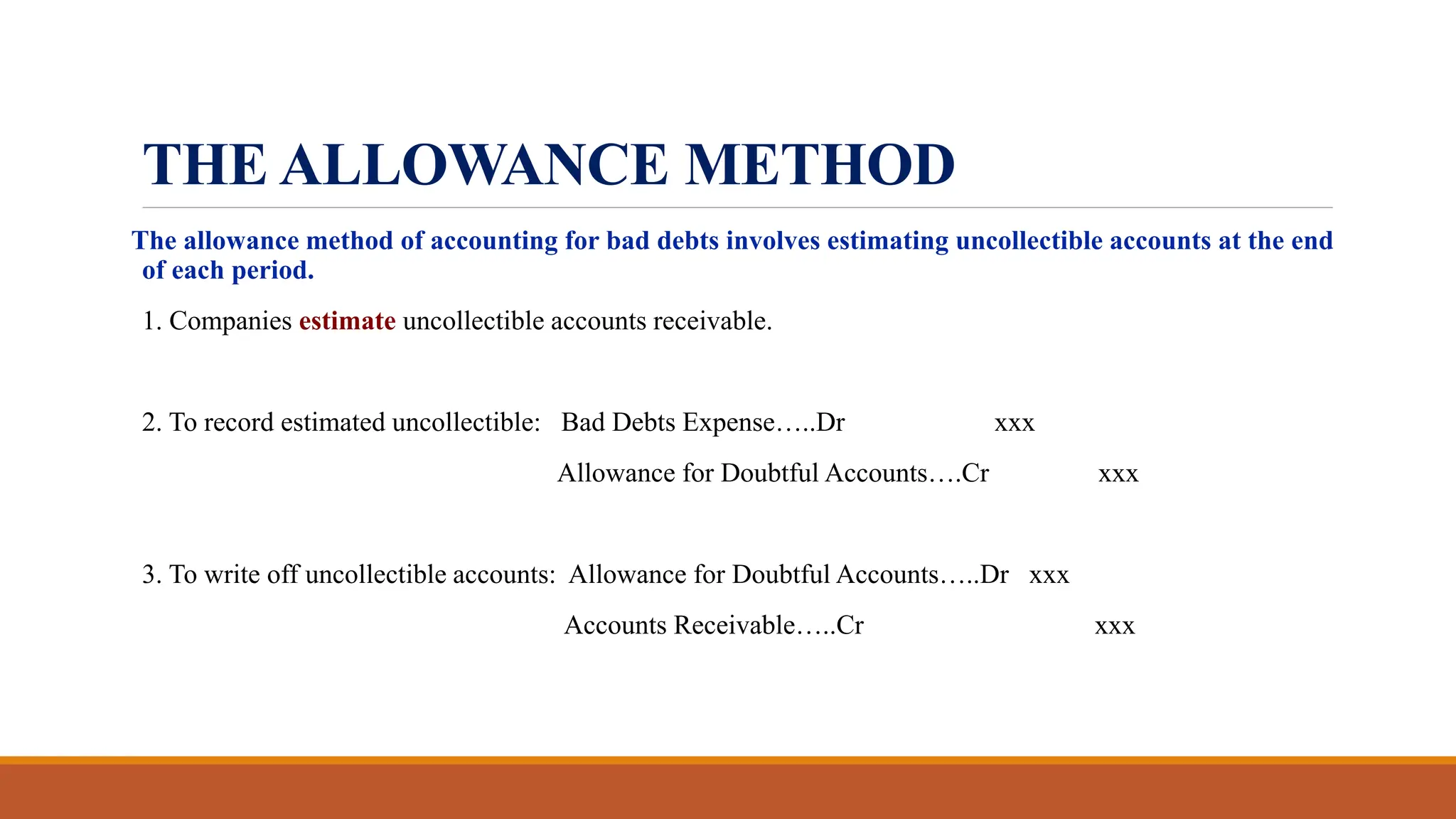

a. Total estimated uncollectible:

March sales (1-30 days) - 2% of 65,000 = 1,300

February sales (31-60 days) - 5% of 17,600 = 880

January sales (61-90 days) - 30% of 8,500 = 2,550

Prior to January (over 90 days) - 50% of 7,000 = 3,500

Total estimated uncollectible = 1,300 + 880 + 2,550 + 3,500 = 8,230

b. Adjusting entry at March 31:

Bad debts expense Dr. 8,230

Allowance for doubtful accounts Cr. 8,230

(To record estimated