Download as PPS, PPTX

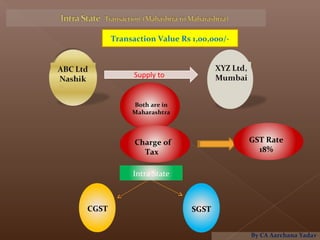

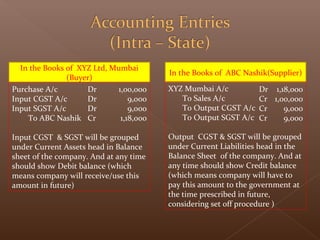

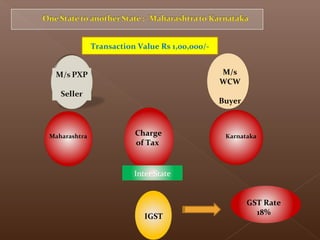

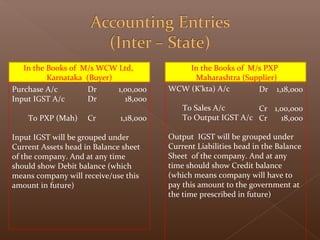

This document contains information about accounting for various GST related transactions including purchases, sales, input tax credit, output tax liability, refunds, and advances received. It provides accounting entries for intra-state and inter-state transactions under CGST, SGST, and IGST and explains concepts like set-off of taxes, separate ledgers for input and output taxes, and accounting for imports. It also covers accounting for tax refunds for exports and output tax on advances received.