Downloaded 75 times

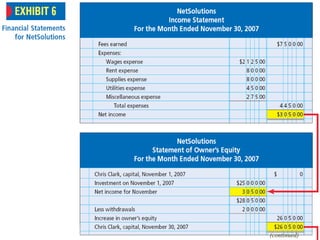

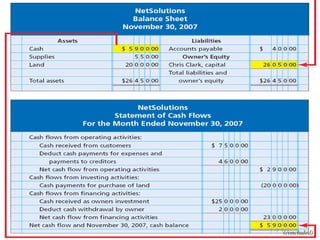

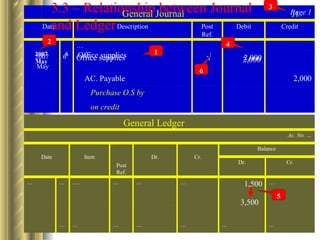

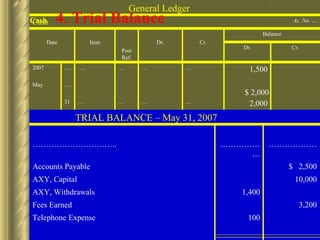

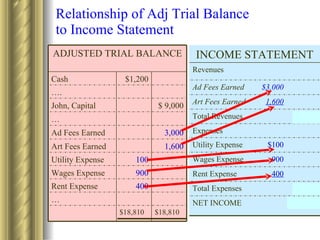

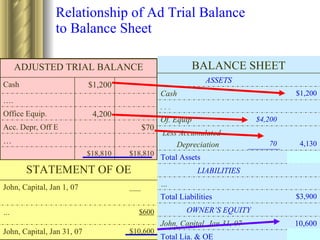

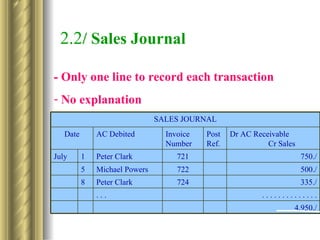

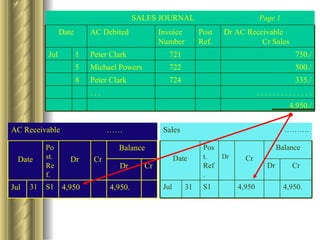

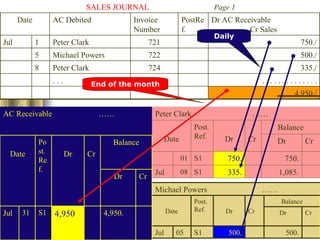

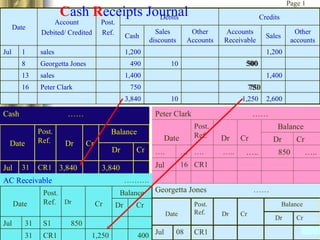

The document provides an overview of accounting concepts and procedures across multiple chapters: - Chapter 1 defines the accounting equation and financial statements such as the income statement, balance sheet, and statement of cash flows. - Chapter 2 covers the double-entry system including T-accounts, the general journal, general ledger, and trial balance. - Chapter 3 discusses adjusting entries, including deferrals and accruals, and how the adjusted trial balance relates to the financial statements.