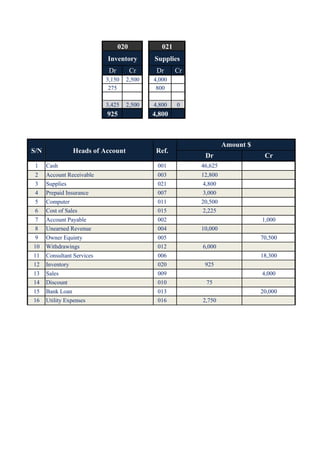

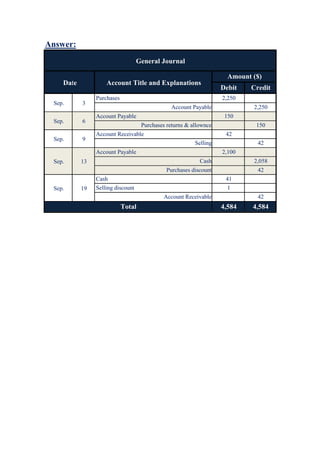

Sherif Consultant Group provides engineering consulting services. The document provides 25 transactions from January 1-25, 2019 to practice journalizing, posting to accounts, and preparing financial statements using the accounting equation and T-accounts. Key aspects covered include unearned and prepaid revenues, depreciation using straight-line method, and allowance method for estimating uncollectible accounts. The income statement shows net income of $12,000 and the balance sheet lists assets of $87,500 equal to liabilities and owner's equity.

![American Industrial Revolution[2]](https://cdn.slidesharecdn.com/ss_thumbnails/americanindustrialrevolution2-1227208285351785-9-thumbnail.jpg?width=640&height=640&fit=bounds)