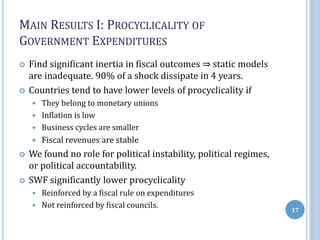

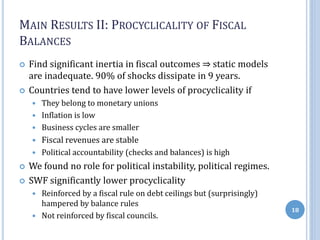

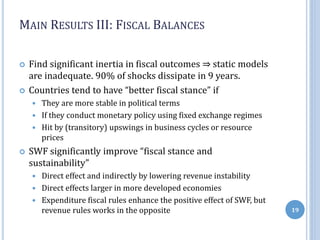

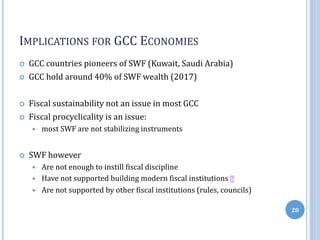

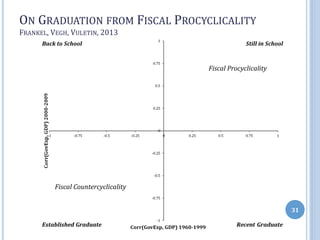

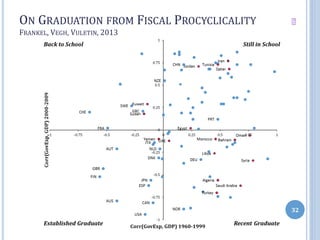

This document discusses sovereign wealth funds (SWFs) and their potential role in macroeconomic stabilization in home economies. It begins by explaining what SWFs are and how they differ from foreign reserves, pension funds, and private wealth funds. The document then discusses several research areas related to SWFs, including their potential impacts on home countries. It finds that SWFs can help facilitate fiscal stabilization and savings. The document outlines some methodological issues in analyzing the impacts of SWFs and describes its analysis of how SWFs may reduce fiscal procyclicality and improve fiscal balances/sustainability in home countries. It finds evidence that SWFs are most effective when complemented by other fiscal institutions like rules and