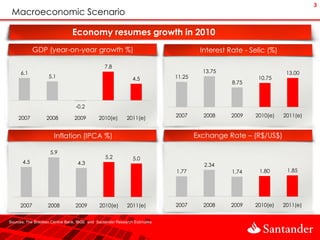

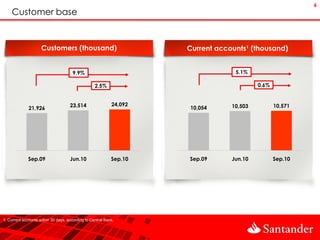

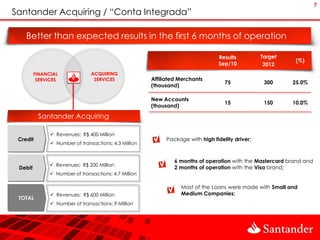

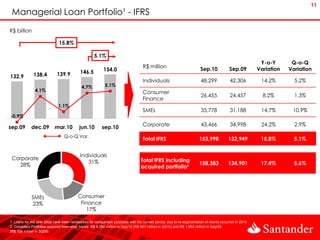

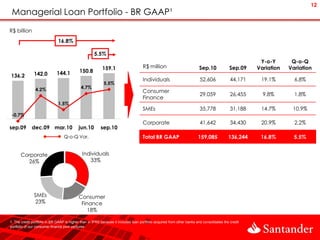

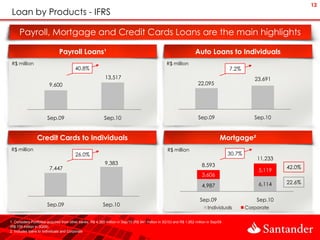

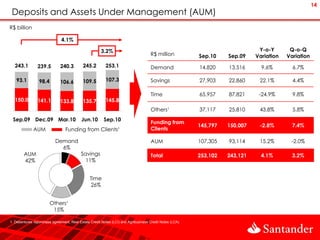

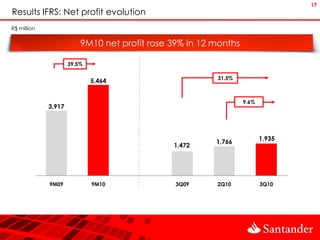

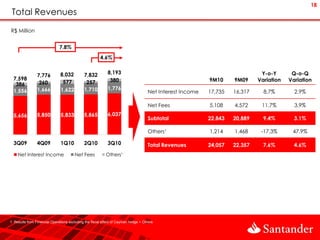

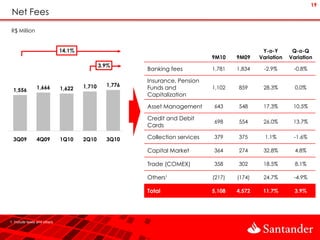

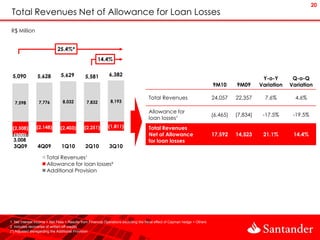

Banco Santander (Brasil) reported results for the first 9 months of 2010. The bank is the 3rd largest private bank in Brazil by total assets, with an 11% market share of loans. Despite the economic crisis, GDP growth resumed in 2010. Santander saw growth in key metrics such as loans, deposits, assets under management, and net profit. The bank has integrated acquisitions successfully and achieved cost synergies above targets. Going forward, Santander aims to continue growing its customer base and expanding its distribution network across Brazil.

![Georgian Banking Sector And Tbc Bank 2011 Q2[1]](https://cdn.slidesharecdn.com/ss_thumbnails/georgianbankingsectorandtbcbank2011q21-13209588990638-phpapp01-111110150353-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)