Download to read offline

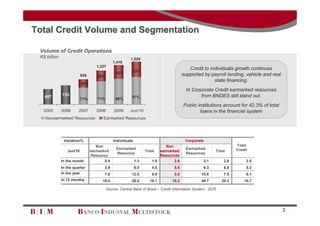

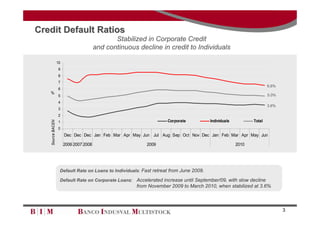

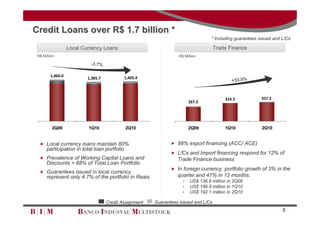

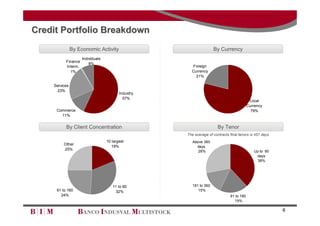

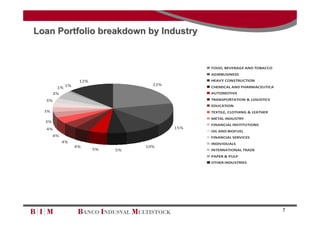

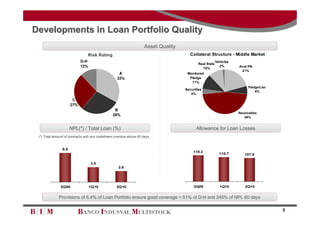

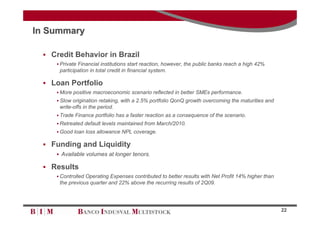

The document summarizes a company's 2Q10 results conference call. It discusses the company's loan portfolio performance, including continued growth in consumer credit from payroll lending and vehicle/real estate financing. Corporate credit saw growth from BNDES earmarked resources. The default rate on consumer loans continued declining while stabilizing for corporate loans. The loan portfolio was diversified across industries with a focus on food/beverage, agribusiness, and heavy construction. Trade finance increased 33.5% year-over-year.