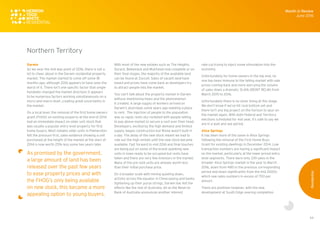

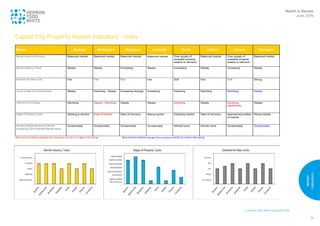

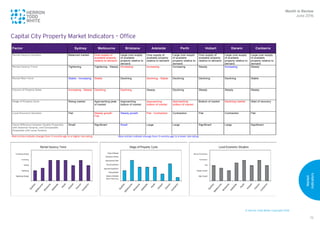

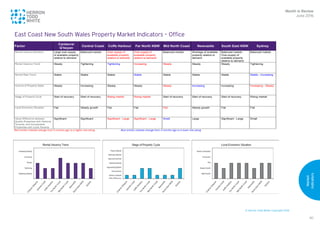

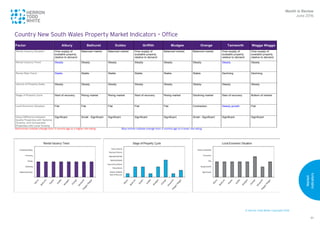

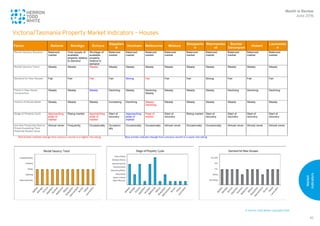

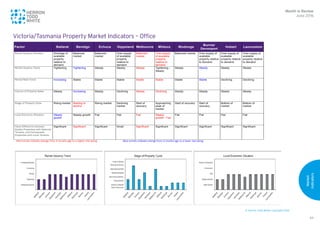

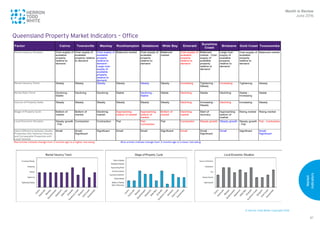

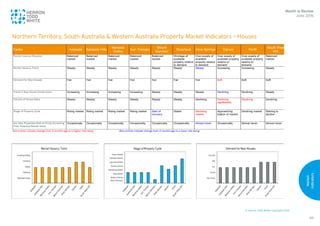

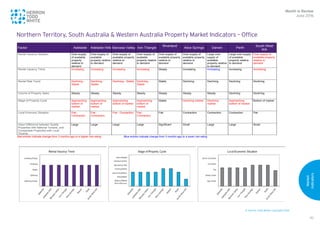

The June 2016 review highlights mixed conditions in Australia's commercial property market at the halfway point of the year, noting a slowdown in activity due to the upcoming federal election and broader economic challenges. Local insights reveal significant variations in rental markets across different sectors and regions, with prime office spaces generally commanding higher rents while secondary spaces face decline in demand and higher vacancy rates. The report emphasizes the need for solid lease agreements and local expertise to navigate the diverse and evolving landscape of commercial property investments.