Download to read offline

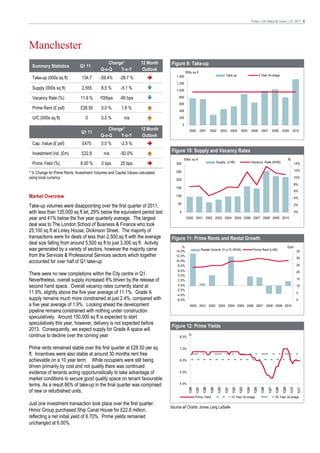

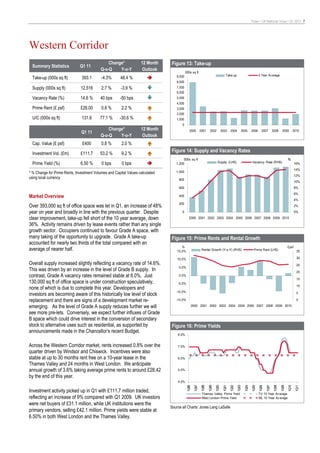

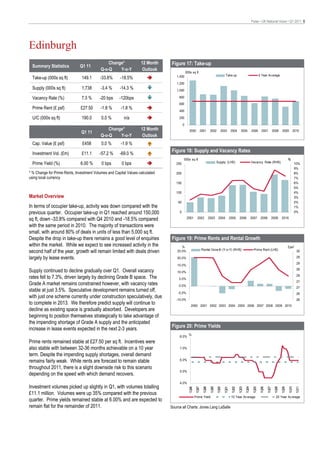

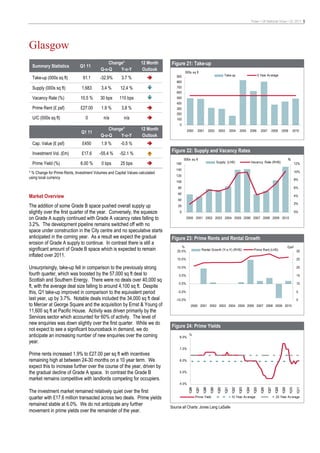

- Office take-up in the UK was down 9% in Q1 2011 compared to the same period in 2010, though performance varied across markets. Supply constraints continued to widen the gap between Grade A and B space. - Rents for prime space continued to be supported by incentives and are expected to see 1.1% growth on average in 2011, while the Grade B market faces more downside risk. - Investment volumes remained relatively weak in Q1 as buyers focused on London and the South East, but strengthening fundamentals may drive more activity outside these areas later in the year.