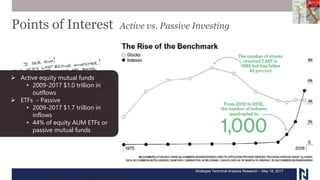

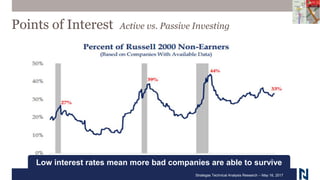

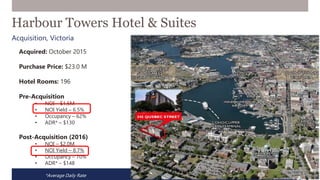

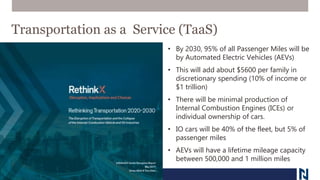

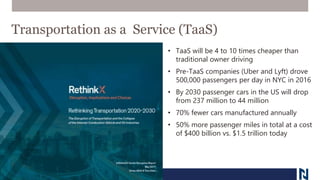

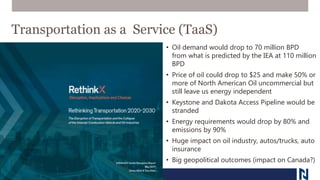

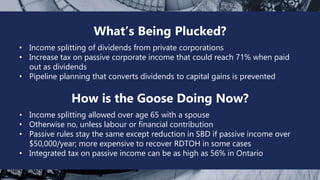

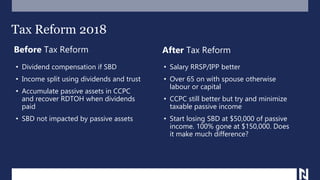

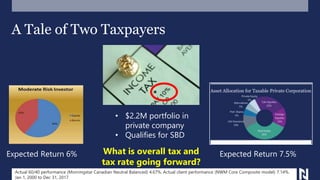

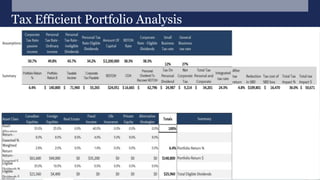

The document provides an extensive overview of the 2018 strategic outlook for wealth management, covering market performance, investment roadmaps, and economic forecasts. It discusses various investment strategies, the impact of U.S. tax reforms, and shifts towards passive investing, while also highlighting the potential transformations in transportation and renewable energy. Additionally, the document emphasizes the necessity of customized planning in response to changing financial landscapes and regulatory environments.