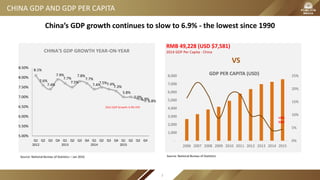

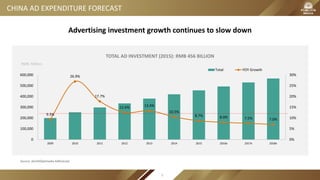

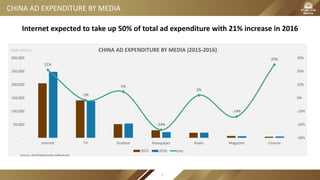

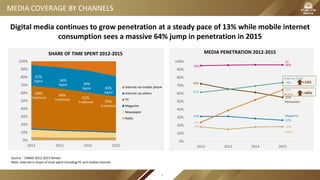

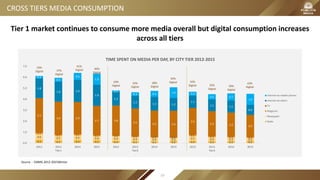

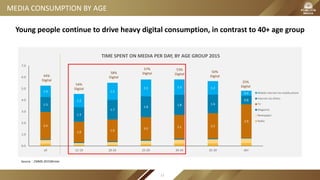

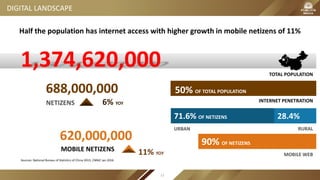

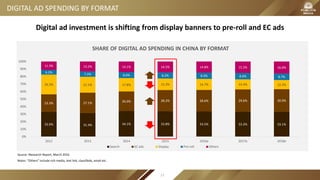

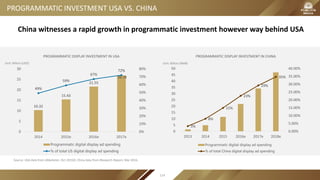

China's GDP growth slowed to 6.9% in 2015, the lowest rate since 1990. Consumer confidence remains stable in China despite the economic slowdown. Total advertising expenditure in China reached RMB 456 billion in 2015 but growth is slowing, with internet advertising expected to account for 50% of total ad spending by 2016 with a 21% increase. Digital media consumption in China continues to rise across all age groups and cities while traditional media declines. Mobile internet penetration reached over 50% of the population in 2015 with mobile internet users growing 11% year-over-year.

![[Report] Internet Trends 2015](https://cdn.slidesharecdn.com/ss_thumbnails/reportinternettrends2015-150717032216-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)