2 Right-Sizing theVC Industry

Paul Kedrosky

Kauffman Foundation June 10, 2009

VC産業は1997年以降投資に見合った分

配をしていない。VC産業は2009年末には

10年利回りがマイナスに転じるだろう。

これは病的な状態であり、最終的に競争

力のあるリターンが得られる状態までVC産

業は縮小していくだろう。今がその段階にあ

るかもしれない。

6

The Canarie isDead

Something is Wrong

in Venture Capital

-Q3 2008-

8.

STARTUP 2.0:

A SILICONVALLEY STORY

SOURCING, SELECTING & ENGINEERING BETTER STARTUPS

VIA INCUBATORS, METRICS & ITERATIVE DEVELOPMENT

Dave McClure, Founders Fund

China Mobile Internet Exec Reception

January2010

9.

The New Faceof Venture Capital

Part 2: Rise of Crowdfunding

A road-map for LPs and startups

Kevin Lawton

March 31, 2010

http://www.trendcaller.com/

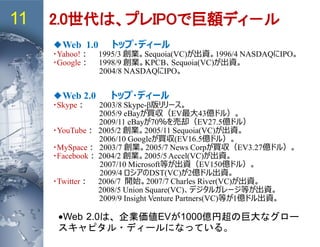

13 発表企業の投資家を見ると・・・

(source) CrunchBase.http://www.crunchbase.com/

Series A 4.1M$ Larry Augustin, Storm Ventures

2.1M$ unattributed

Series B 9M$ Sierra Ventures, eBay, Storm Ventures, Larry Augustin

Series A 600K$

Series B 4.4M$

Amazon, Madrona Venture Group, SoftTech VC, Bruce

Livingstone

unattributed 13.5M$ eBay

Series A 11M$ Benchmark Capital

Seed 20K$ Y Combinator

Seed 600K$ Sequoia Capital, Youniversity Ventures

Series A 7.2M$ Sequoia Capital, Greylock Partners, Youniversity Ventures

Angel 315K$ Spencer Ain, Judson Ain, Sean Meenan

Series A 1M$

Union Square Ventures, Caterina Fake, Stewart Butterfield,

Joshua Schachter, Albert Wenger

Series B NA Union Square Ventures

Series C 3.25M$ Union Square Ventures

Series D 27M$

Accel Partners, Union Square Ventures, Hubert Burda Media,

Acton Capital Partners

Series E 20M$

Index Ventures, Accel Partners, Hubert Burda Media, Acton

Capital Partners

Angel 1.4M$ Chris Michel, Michael Birch, Stan Chudnovsky, James Currier

エンジェルがエンジェルが

目につく目につく

15.

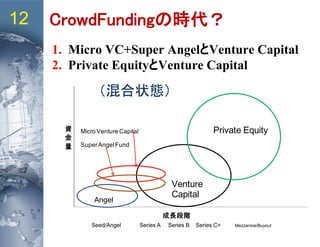

Micro (Lean) VentureCapital14

HQ: Mountain View

Key: Paul Graham

HQ: San Francisco

Key: Robert May, Peter Thiel

HQ: Boulder, CO

Key: Brad Feld

HQ: Washington, DC

Key: Julius Genachowski

(old?) HQ: Pasadena, CA

Key: (Bill Gross)

Tom McGovern

16.

Super Angel (Fund)15

(RonConway, David Lee)

Google, PayPal, Ask Jeeves, Digg,

Mint.com, Twitter

(Ron Conway: Angel)

Ron has served/serves on Boards/Advisory Boards

including: Twitter, Digg, Ask Jeeves,Facebook,

RockYou, ScanScout, Zappos, Trulia, Plaxo, etc.

(David Burwen)

Voicebase, Practice Fusion, GlobalMotion,

Vapore, Ustream

(Reid Hoffman: Angel)

Facebook, Flickr, Digg, Zynga,

Reid previously served as CEO of LinkedIn and

now he is a partner at Greylock Partners.