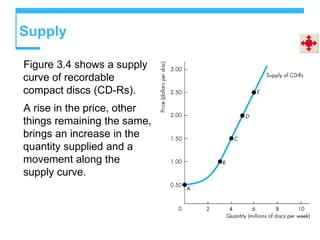

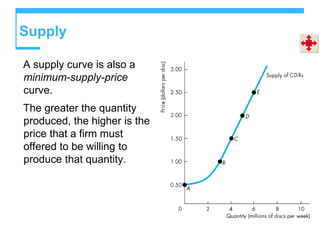

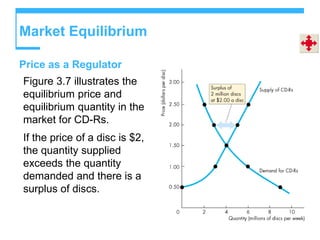

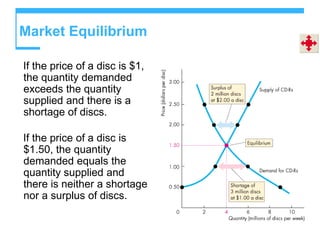

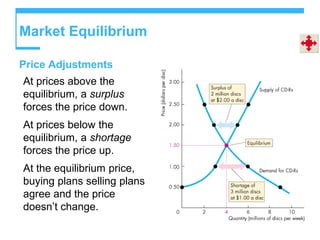

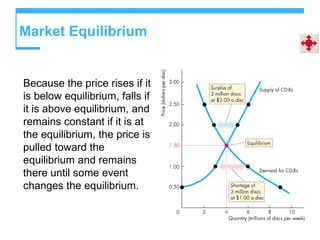

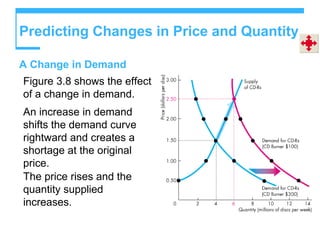

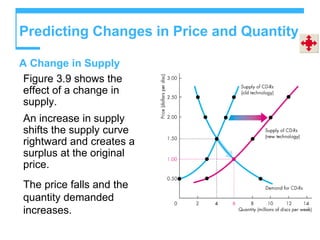

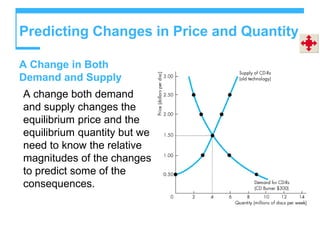

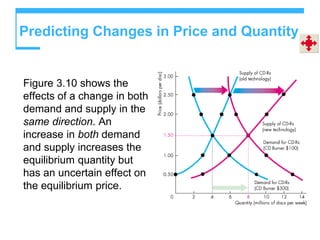

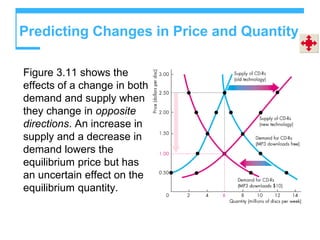

This document defines key economic concepts related to markets, supply and demand. It explains that a market allows buyers and sellers to exchange goods and services. Demand for a product depends on factors like price, income, and preferences of consumers. The law of demand states that as price rises, quantity demanded falls. Supply depends on factors like price of resources and technology. The law of supply says that as price rises, quantity supplied increases. Market equilibrium occurs when quantity supplied equals quantity demanded, and there is no surplus or shortage.