Downloaded 31 times

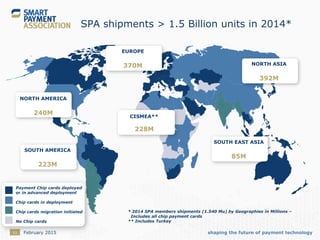

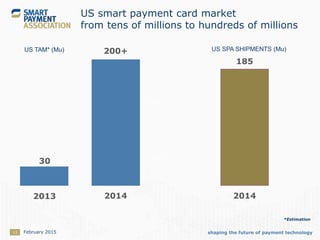

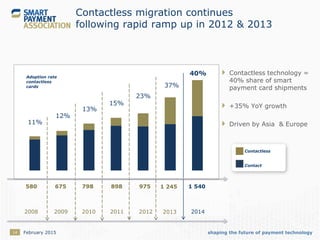

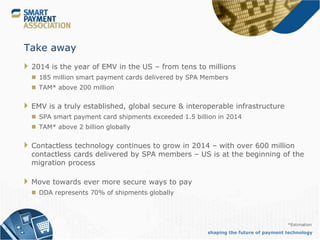

The Smart Payment Association (SPA) highlights significant growth in payment technologies, with 2014 seeing 185 million smart payment cards shipped in the US and over 1.5 billion globally. The report emphasizes the establishment of EMV as a global standard and increasing adoption of contactless payments, which accounted for 40% of smart card shipments in 2014. Additionally, the SPA focuses on supporting members through market monitoring and addressing regulatory standards to adapt to the evolving payment landscape.