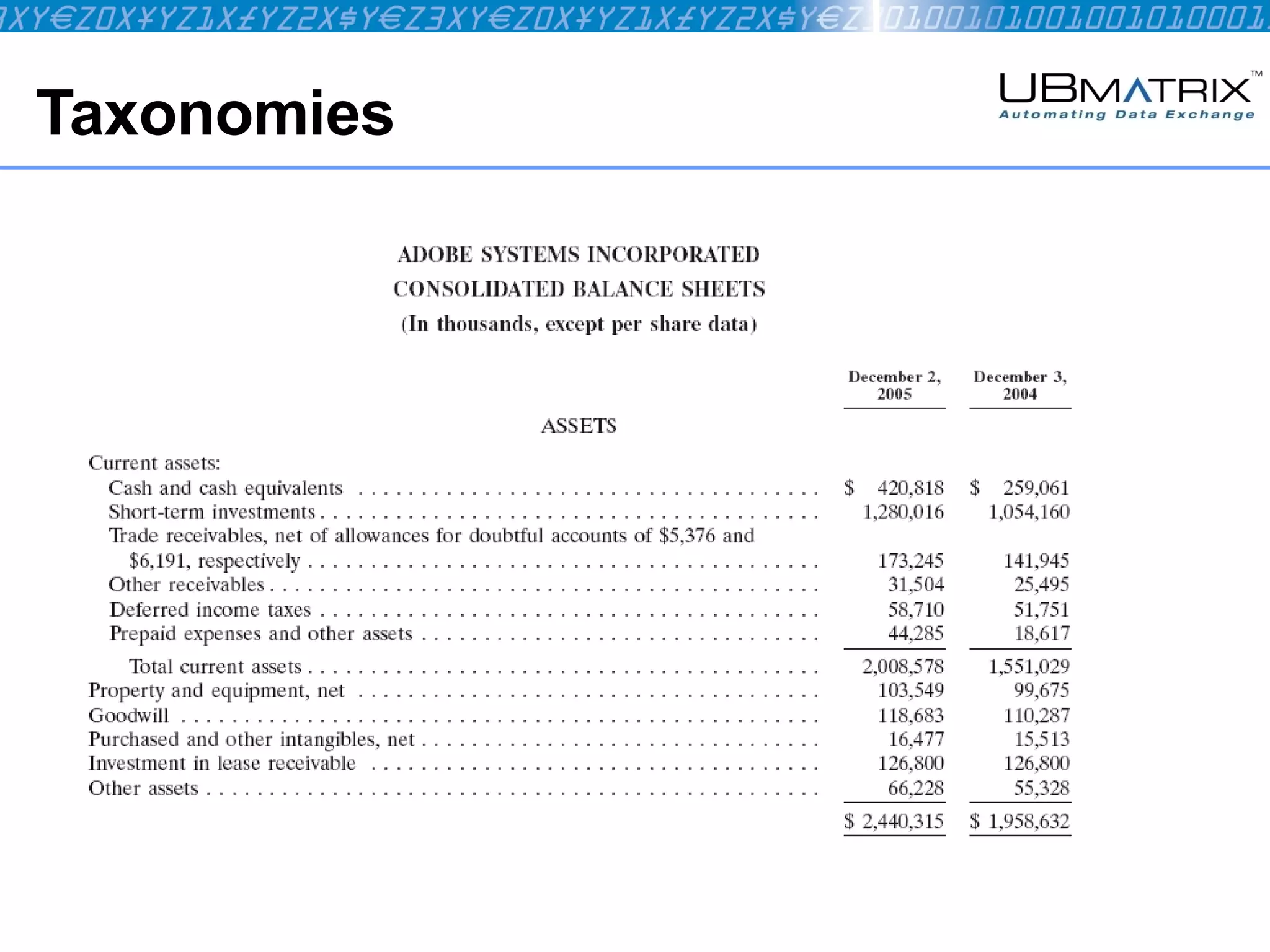

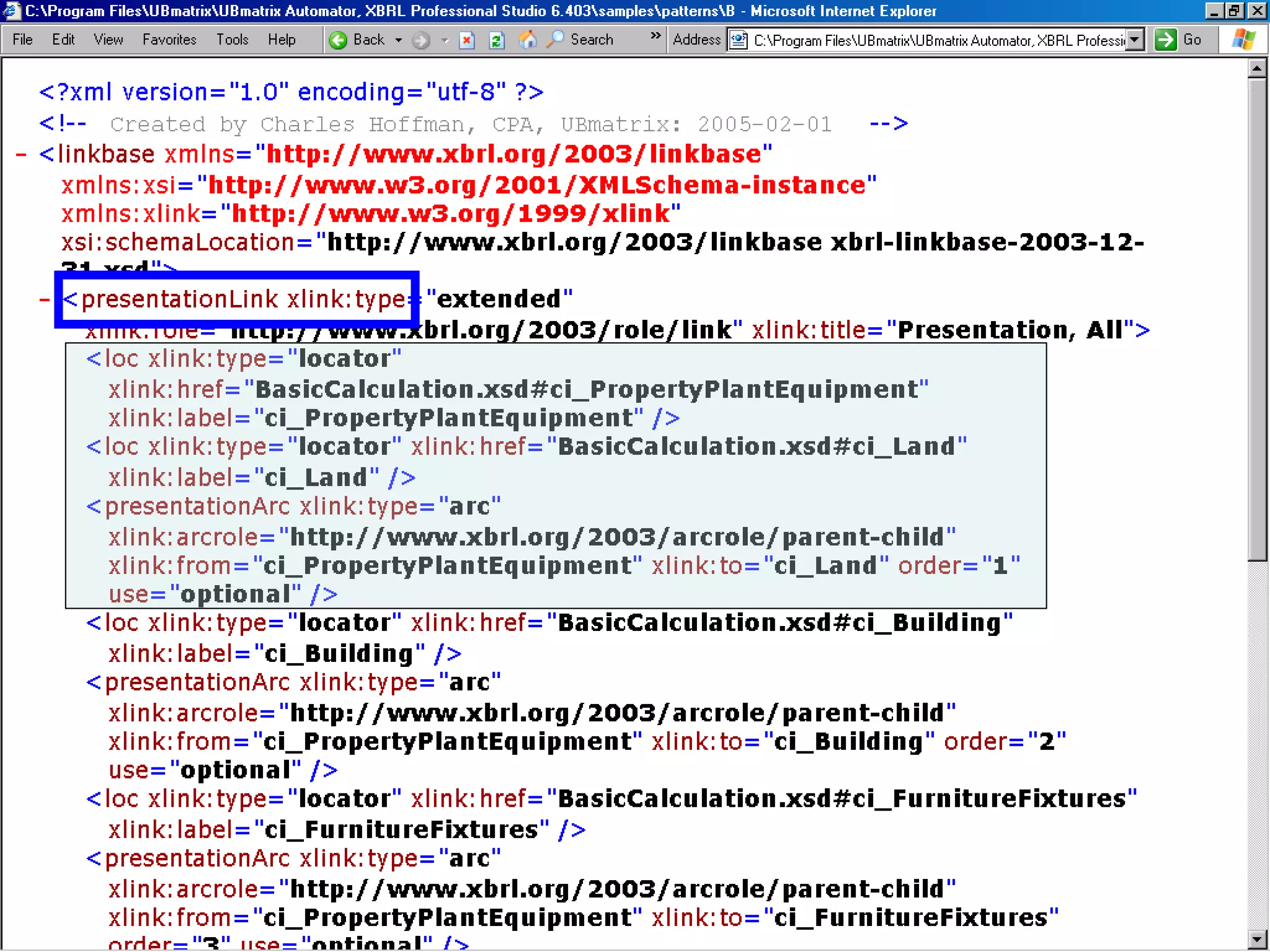

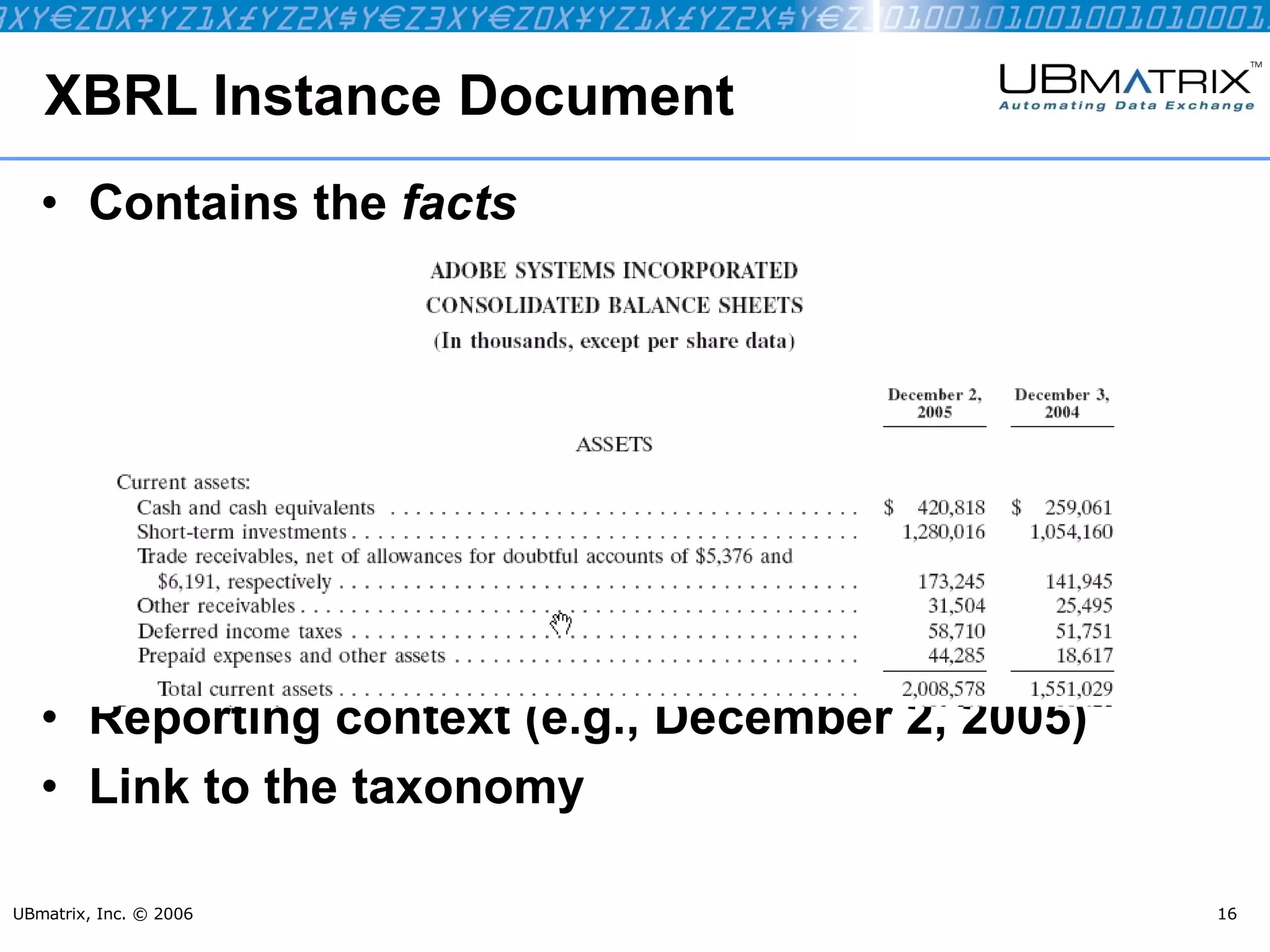

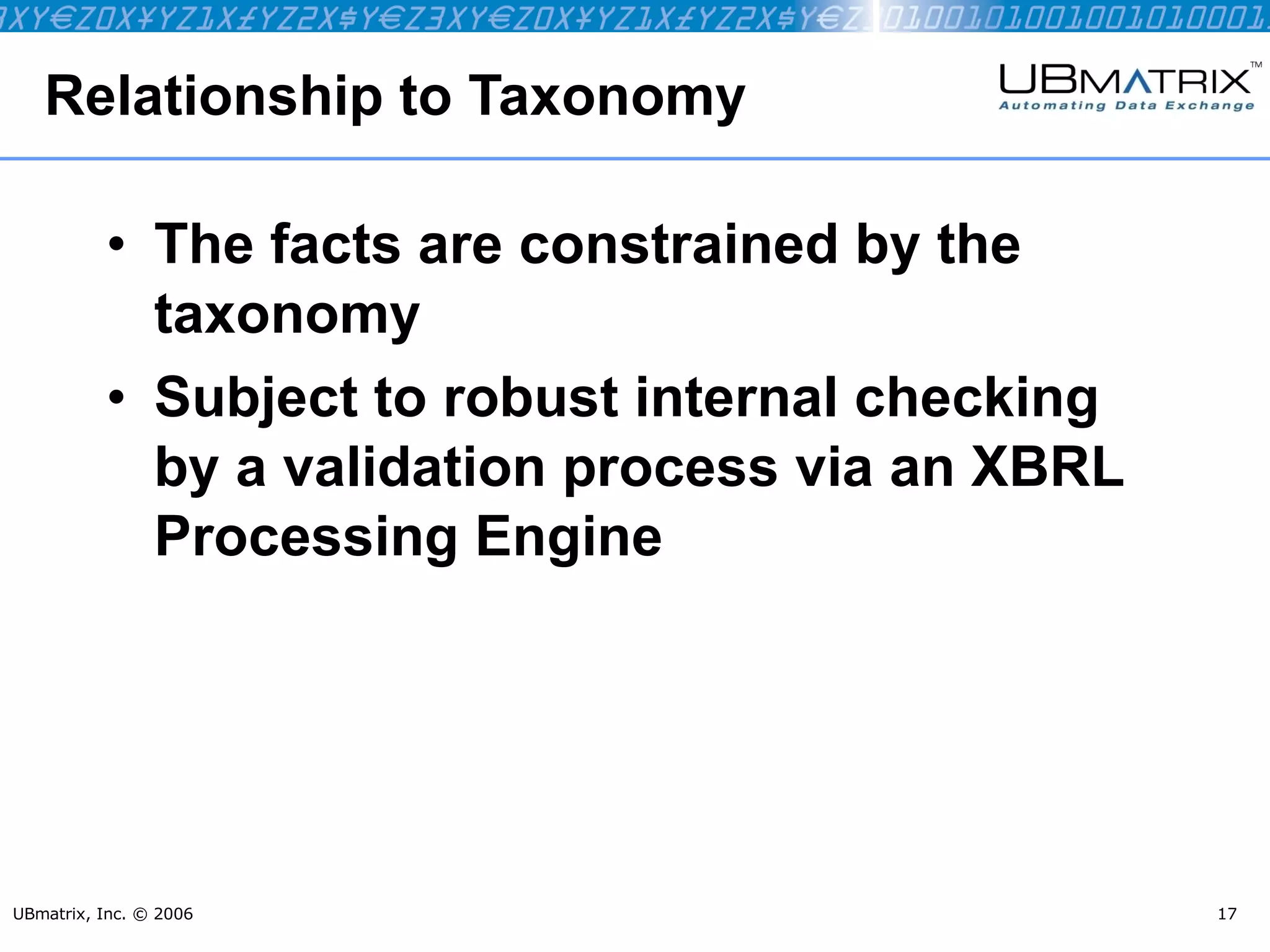

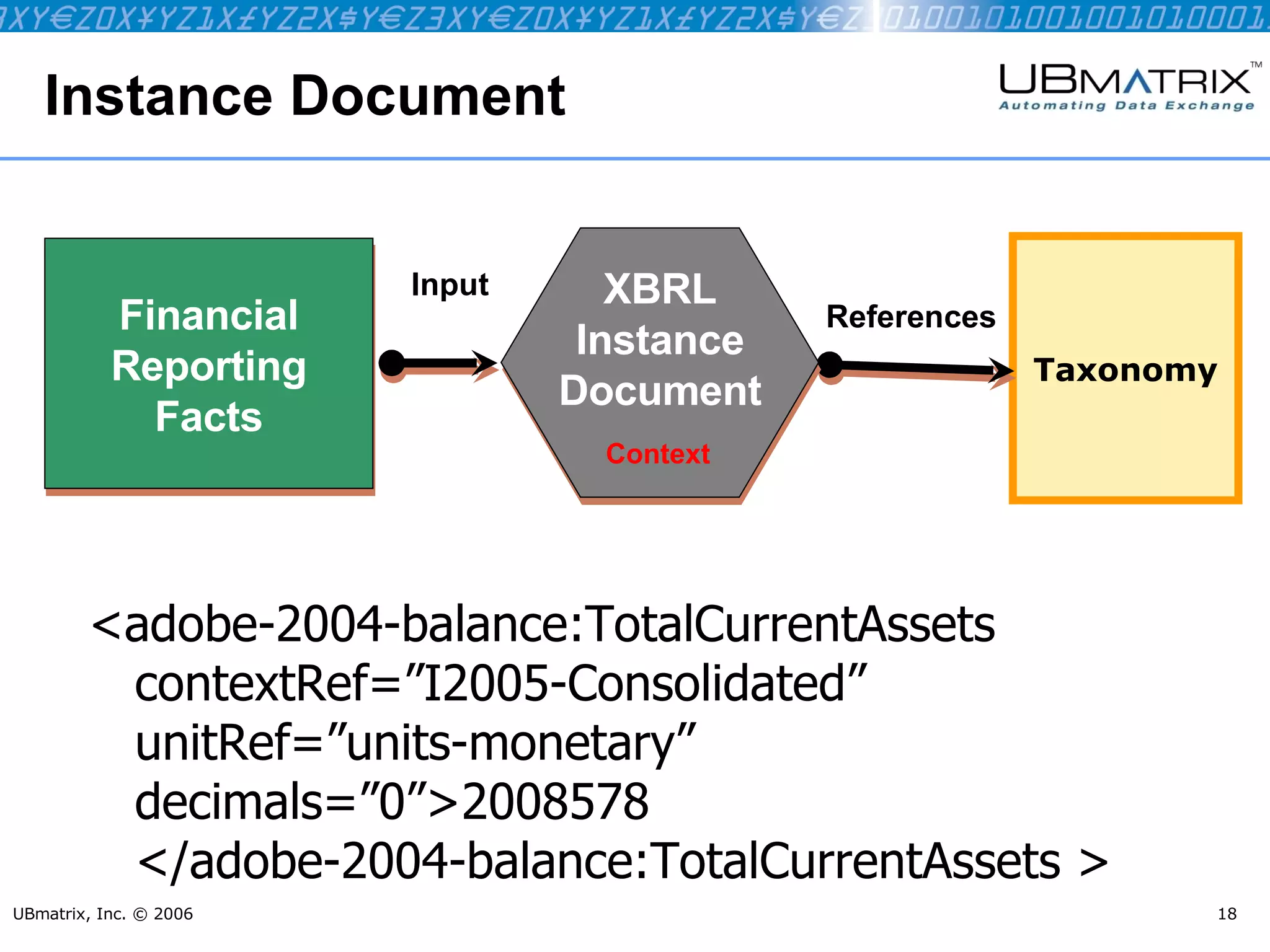

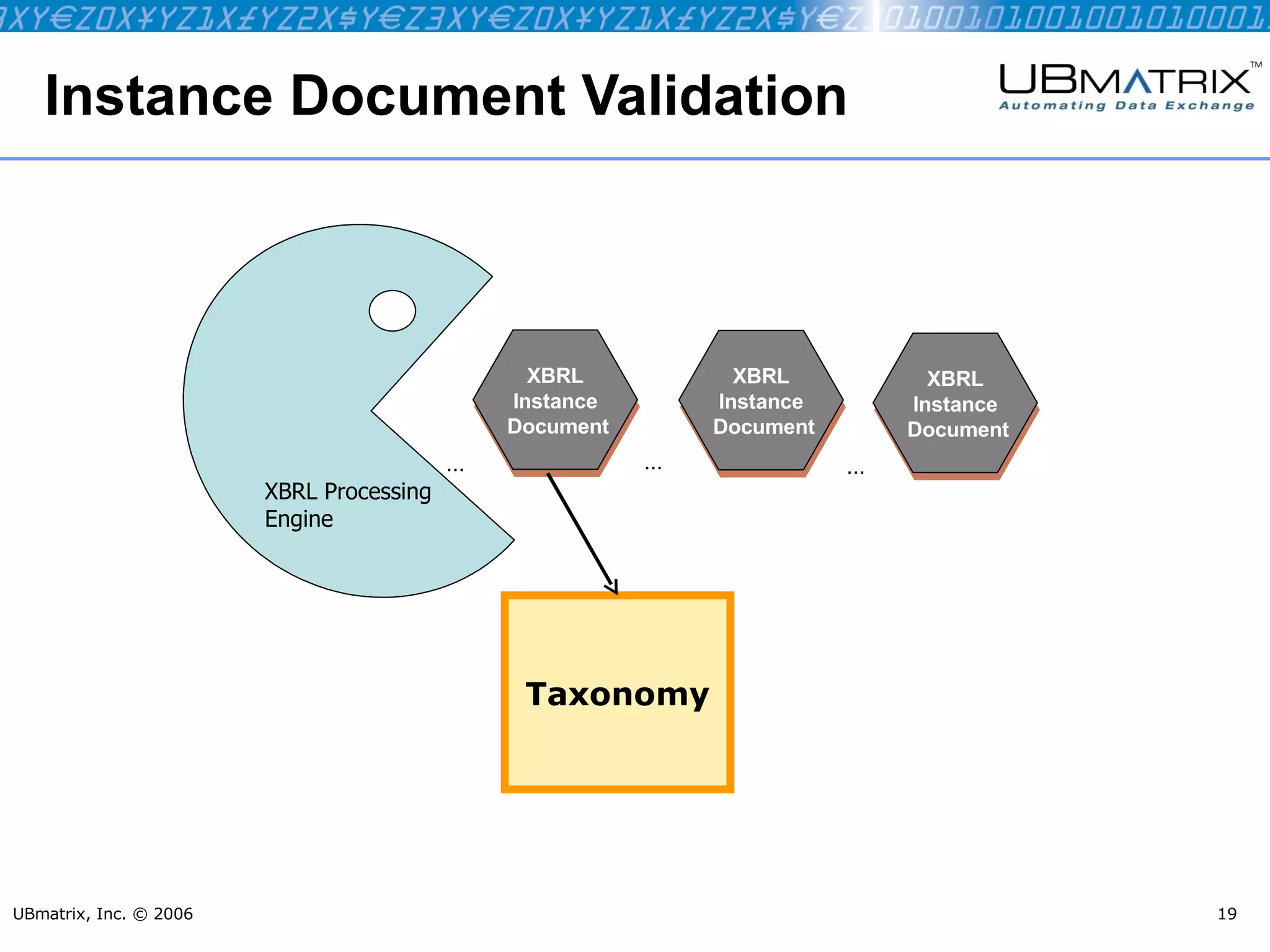

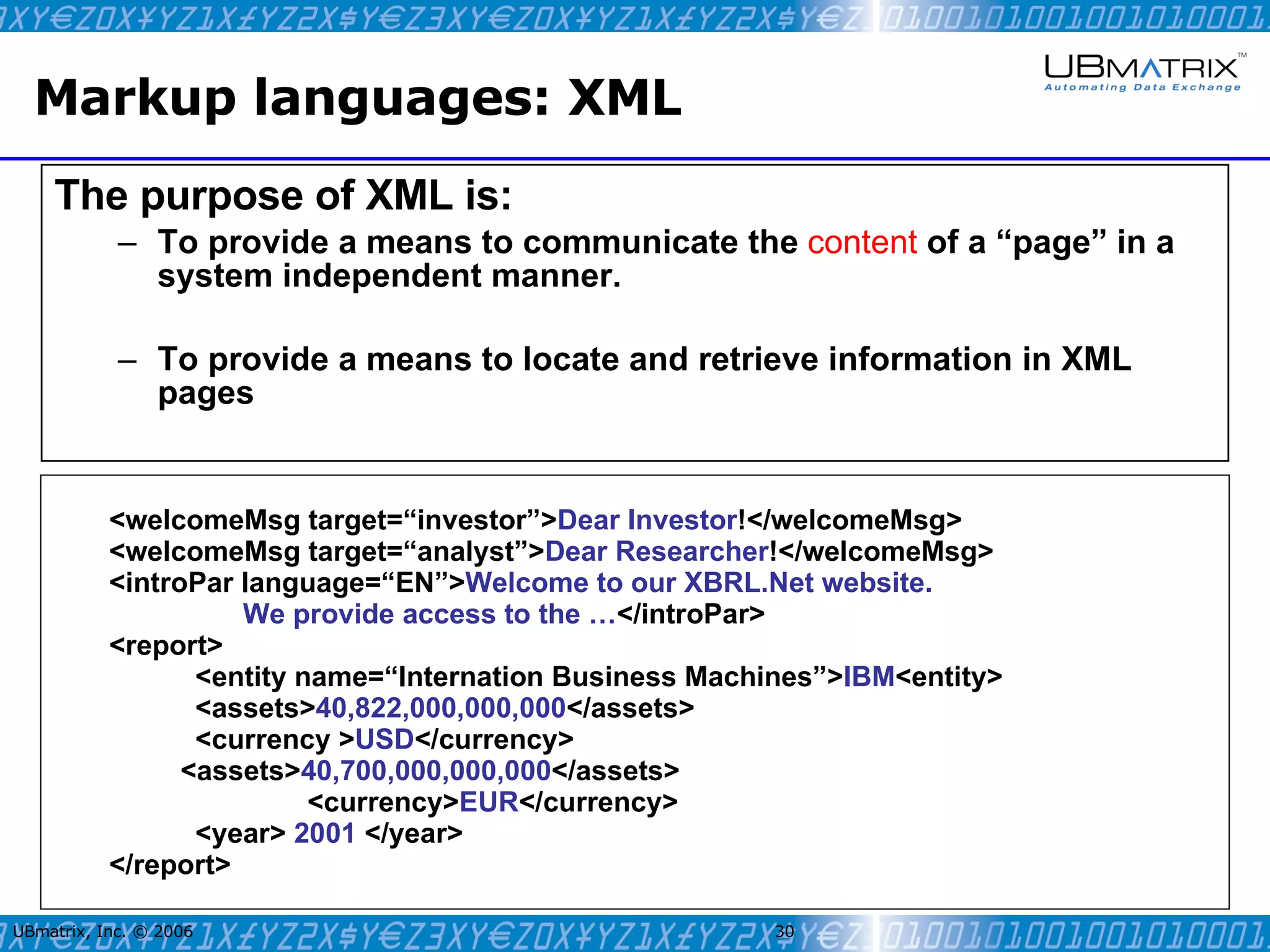

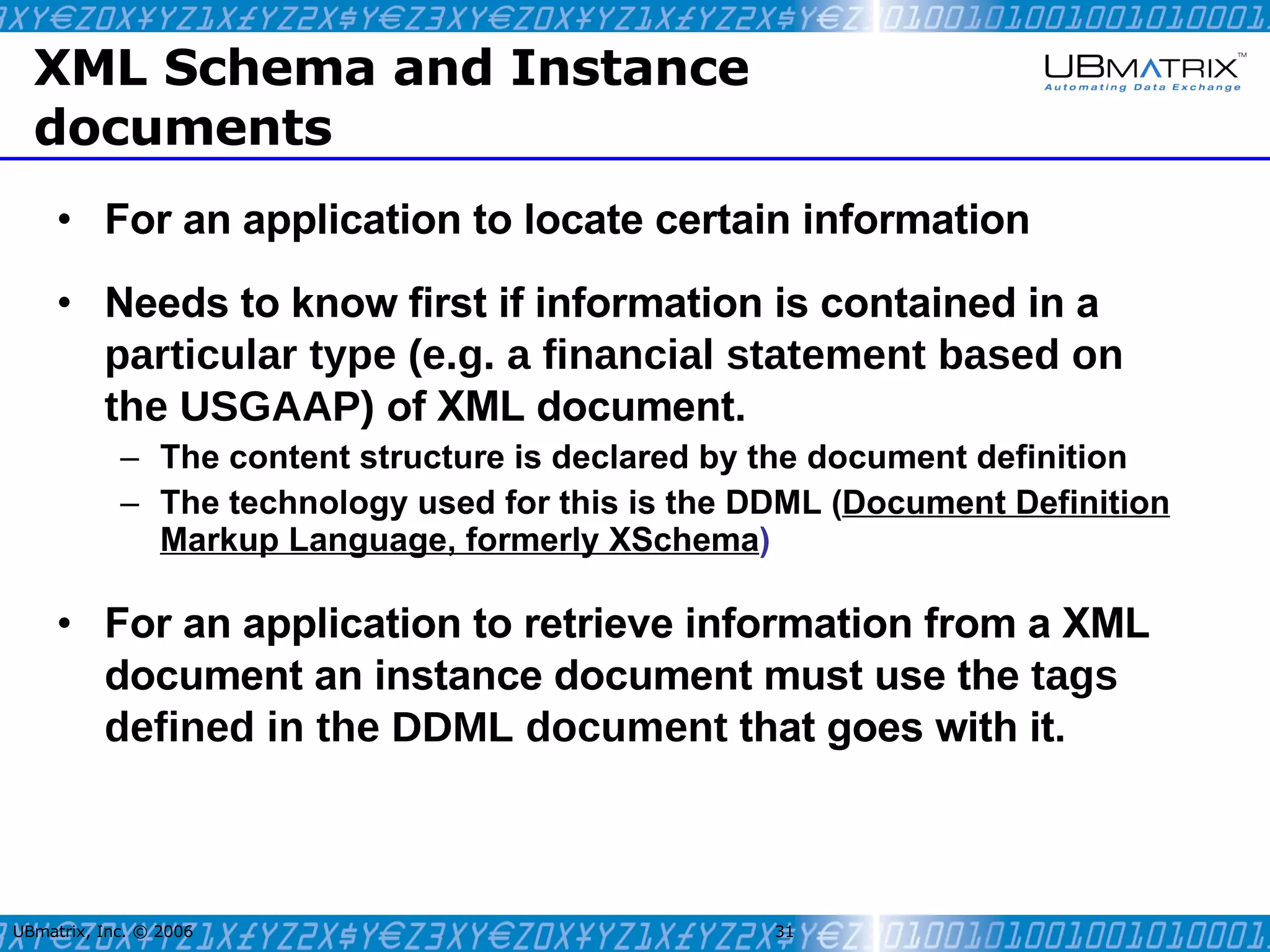

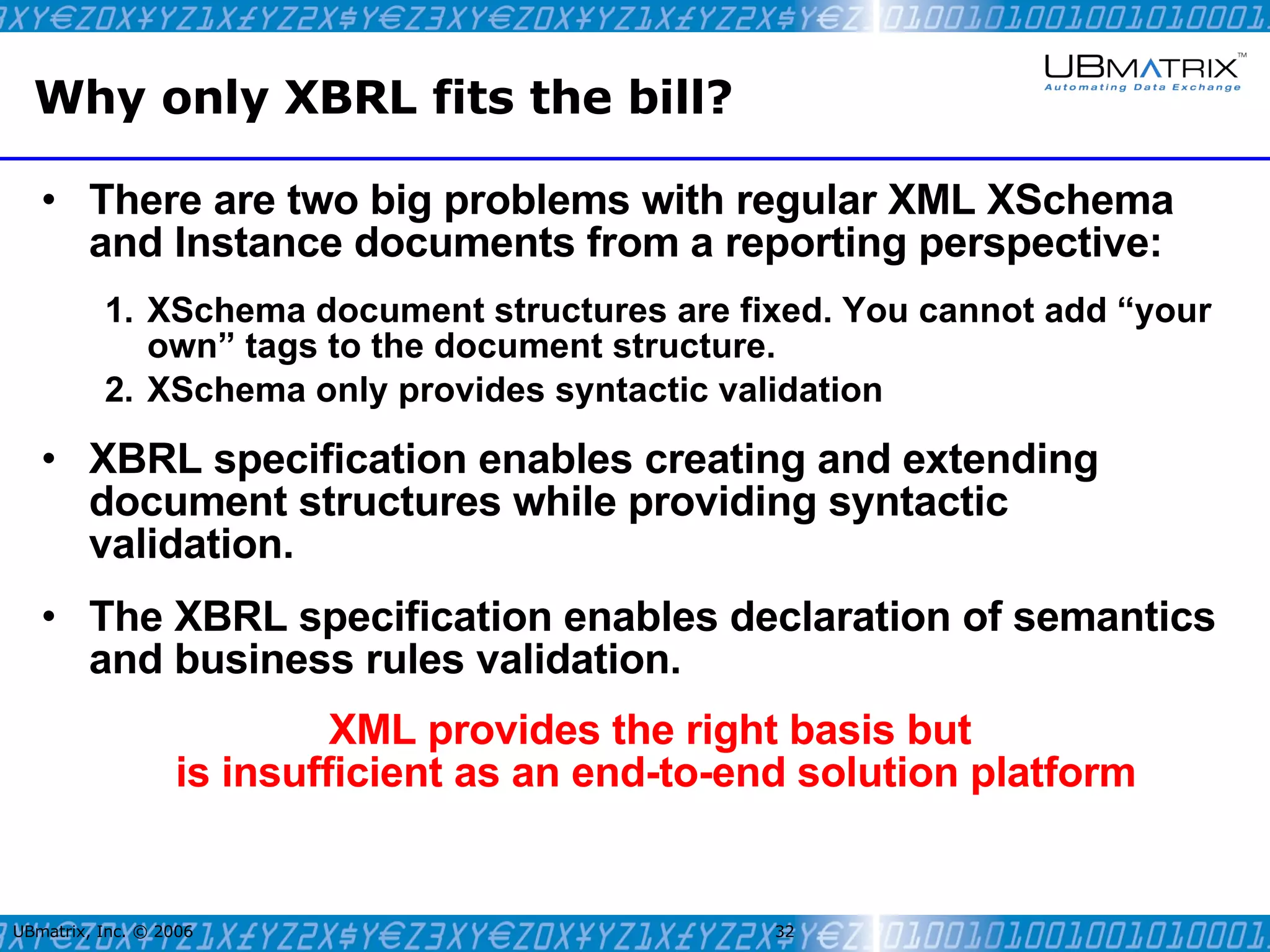

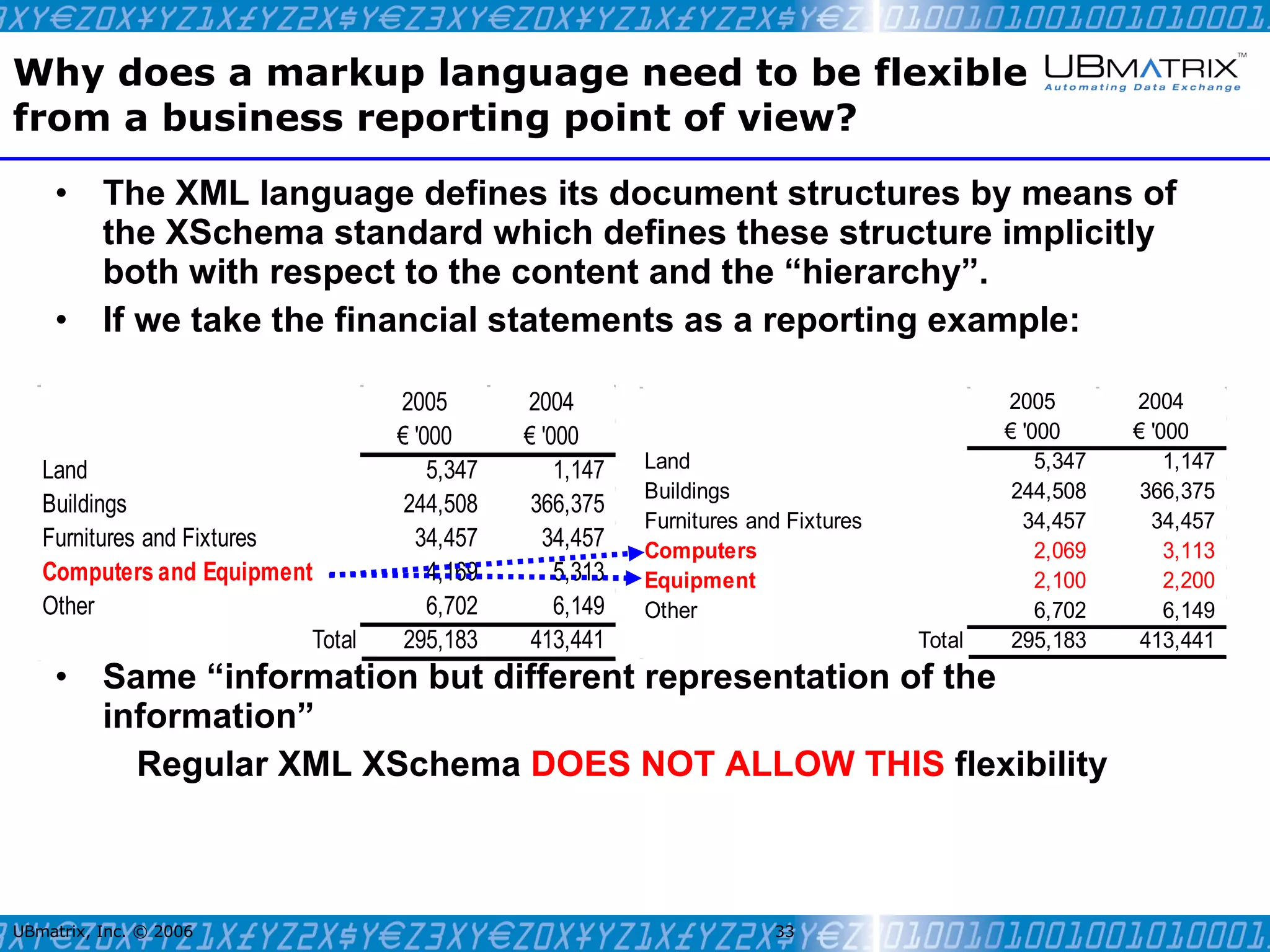

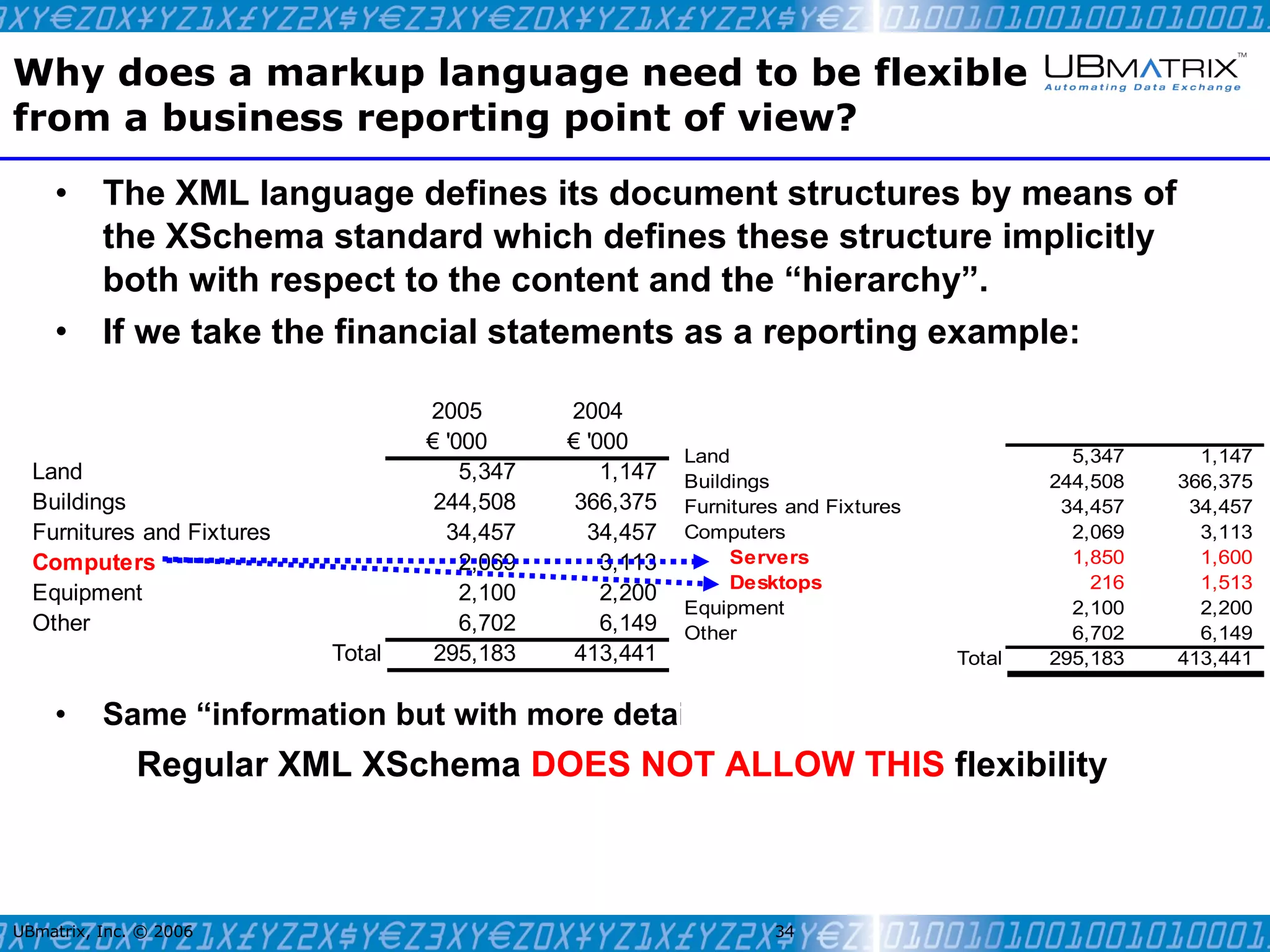

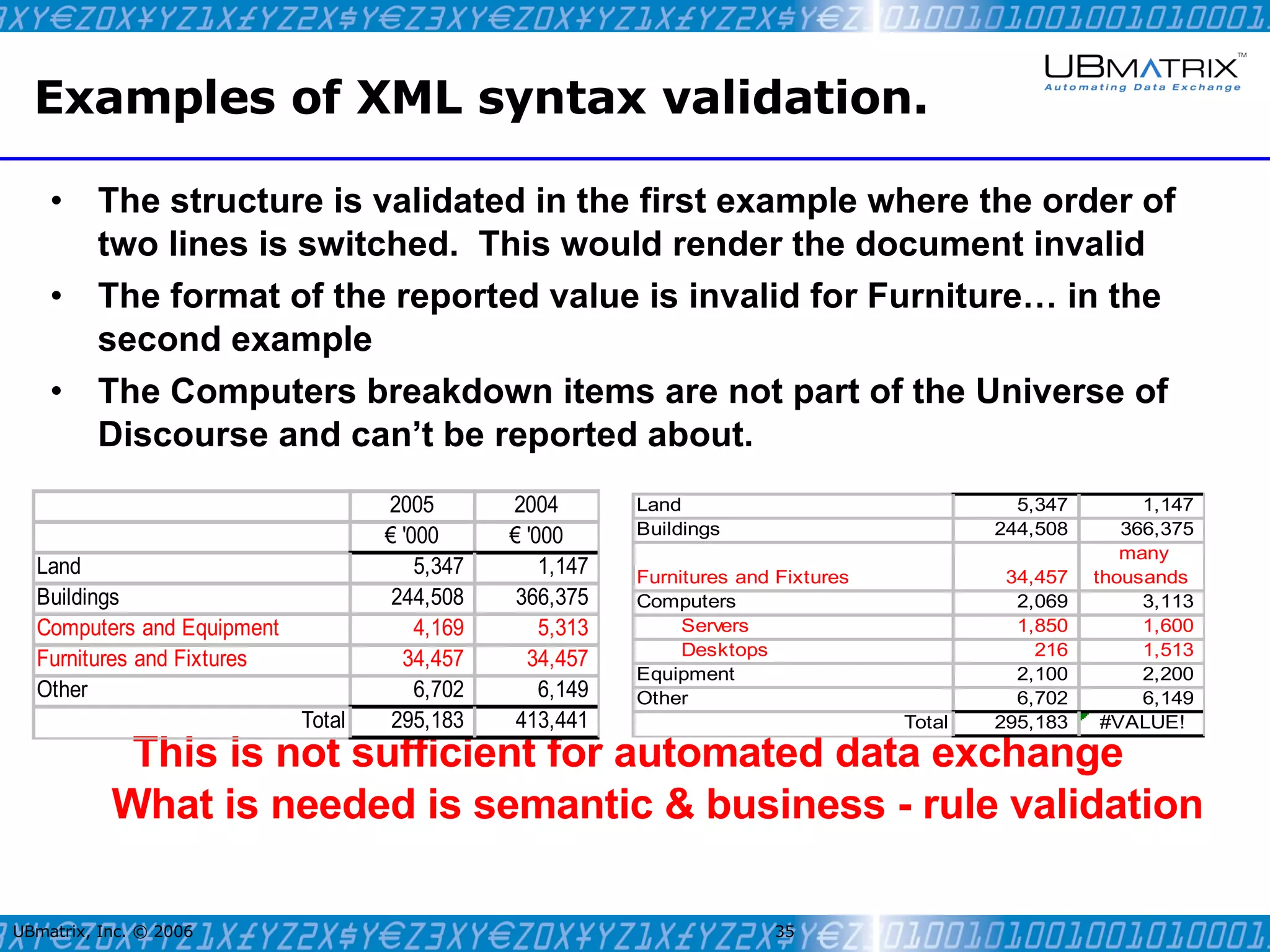

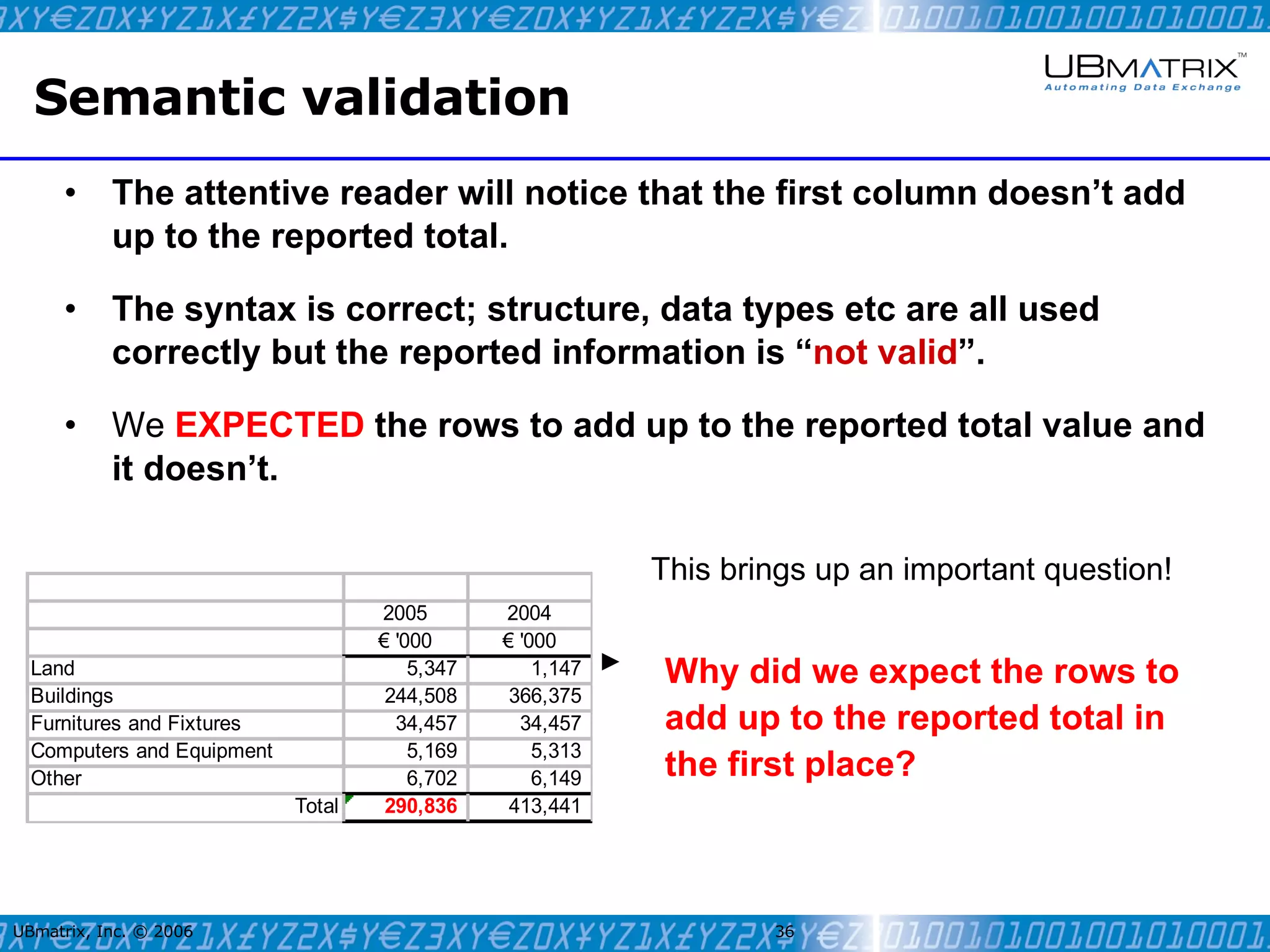

The document provides an overview of XBRL (eXtensible Business Reporting Language) and compares it to XML. It discusses XBRL taxonomies, which define reporting concepts and relationships, and XBRL instance documents, which contain reported facts that are constrained by the taxonomy. While XML provides a basis, XBRL was created to address XML's limitations for business reporting by allowing flexible extension of reporting structures and validating semantics and business rules, not just syntax.

![[DE] DMS: Ist-Analyse und Auswertung von Analysen | Dr. Ulrich Kampffmeyer | ...](https://cdn.slidesharecdn.com/ss_thumbnails/dmsist-analyseulrichkampffmeyer19980112-160819092253-thumbnail.jpg?width=640&height=640&fit=bounds)