This document provides an overview of key concepts in XBRL (eXtensible Business Reporting Language), which is a standard for electronic communication of business and financial data. It defines terminology used in XBRL and explains how taxonomies define financial reporting concepts and how instance documents contain fact values that use these concepts. Taxonomies and instance documents are structured using XML.

![FINANCIAL REPORTING USING XBRL – IFRS AND US GAAP EDITION (2006-03-01)

5.6. Key Difference Between Taxonomy and Instance

Information

At this juncture there is a need to point out the difference between what goes

into a taxonomy and what goes into an instance document. The key point to

remember from this discussion is that, in general, the contextual information

expressed in instance documents should not be contained in taxonomies.

There are exceptions to these rules. For example, a taxonomy for a tax return

that requires information for the current period and prior period might contain

concepts only for the current period and both concepts and contextual

information for the prior period.

If taxonomy creators consciously violate these best practices to achieve a desired

result in a specific circumstance, that would be acceptable practice. However, not

being conscious of certain information relating to how instance documents work

can cause problems for users desiring to use information contained in instance

documents.

Putting this contextual information in taxonomies creates comparability problems

and is the equivalent of “hard coding” information within a taxonomy.

5.7. FRTA and FRIS

The XBRL Specification specifies how XBRL taxonomies and instance documents

must be created.

The Financial Reporting Taxonomies Architecture (FRTA) places additional

constraints on XBRL taxonomies which are intended to express information used

in financial reporting. These constraints are intended to enhance comparability of

financial information expressed using XBRL.

The Financial Reporting Instance Standards (FRIS) places additional constraints

on instance documents used for financial reporting. All instance documents and

taxonomies that are valid under the FRTA and FRIS are valid XBRL documents;

however, not all XBRL documents are valid under the FRTA and FRIS. Again,

these constraints are intended to enhance comparability of financial information

expressed using XBRL.

XBRL International provides the FRTA and FRIS to assist those wishing to use XBRL for the

reporting of financial information such as the financial statements of public companies.

This document is intended to comply with:

• The Financial Reporting Taxonomies Architecture [FRTA].

• The Financial Reporting Instance Standards [FRIS].

All information in this document assumes a desire to comply with FRTA and FRIS.

5.8. Separating Presentation and Data

Financial statements (and other business reports) express information. This

information is expressed in certain presentation forms that can helpful in how to

best express that information in an XBRL taxonomy. These forms of presentation

are basically “data patterns”. Identifying these patterns helps understand how to

organize information in taxonomies and how to do so consistently.

There is a fundamental difference between “data” and “presentation”. This

distinction must be understood in order to build taxonomies in the correct

manner. This fundamental distinction between data and presentation is used to

design the taxonomy. Presentation can sometimes provide “clues” as to the data

© 2006 UBmatrix, Inc 87](https://image.slidesharecdn.com/chapter-05-gettingstartedwithxbrl-100426201158-phpapp01/85/Chapter-05-getting-startedwithxbrl-21-320.jpg)

![FINANCIAL REPORTING USING XBRL – IFRS AND US GAAP EDITION (2006-03-01)

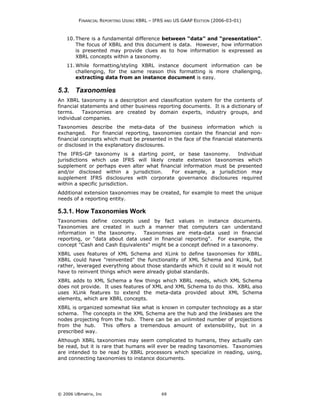

The above screen shot shows how a reviewer of an instance document can view

the tagging of information in XBRL to see if it was done correctly. For example,

this will facilitate the detection of the use of the wrong tag placed on a piece of

data.

In the above report, XBRL is shown without with the angle brackets, and in a

more human readable form. It also show the data with a minimum amount of

formatting so the complex data is readable by humans, but still allows them to

see the detailed tagging so it can be reviewed and verified.

5.9.6. Extracting Data from XBRL Instance

Extracting information from an XBRL instance document is very straight forward

as XBRL makes minimum use of XML Schema content models. The following

XPath expression is an example of how an XSLT document might extract

information from an XBRL instance document:

<xsl:value-of select="format-number(/xbrli:xbrl/ci:Building[@contextRef='I-2003']

div 1000,'#,##0','base')" />

The above XPath expression (the value of the select attribute) extracts the value

for the element "Building" for the context equal to "I-2003". It then divides the

number by 1000 in order to express it for presentation purposes in thousands of

Euros, and then formats the number with a comma to separate each group of

three digits and shows no decimal places.

The following is an Excel spreadsheet VBA macro which extracts data from an

XBRL instance document:

Populating a model with financial data from an XBRL instance document or

formatting information using XSLT (which is discussed below) or rendering it in

some other format such as Word, HTML, PDF, etc uses these relatively simple

XPath expressions to locate XBRL instance data.

Below is simply extracting data from an XBRL instance document and putting it

into Excel, no formatting, just plopping it into a simple table rather than into a

specific models format:

© 2006 UBmatrix, Inc 96](https://image.slidesharecdn.com/chapter-05-gettingstartedwithxbrl-100426201158-phpapp01/85/Chapter-05-getting-startedwithxbrl-30-320.jpg)